Market analysts are predicting that some relief for homebuyers may be around the corner, in the form of lower mortgage rates.

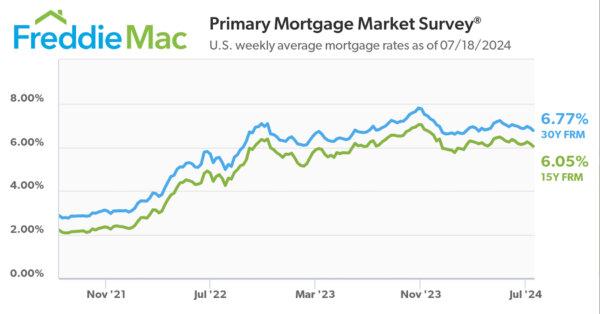

In a report released on July 18, Freddie Mac, a government-sponsored buyer of home loans, struck an optimistic tone, stating that “mortgage rates are headed in the right direction and the economy remains resilient, two positive incremental signs for the housing market.”

The rate for 30-year fixed-rate mortgages fell to 6.77 percent, dropping 12 basis points from the prior week and the lowest level since mid-March. This is down from nearly 7.8 percent last fall, but still significantly above rates that were around 2.7 percent in July 2021, before inflation began to escalate.

Economist and former Federal Reserve vice president Gerald Dwyer says both the market component and the risk component of mortgage rates are currently elevated, and both are likely to come down in the short term.

“There are two parts that are elevated,” Mr. Dwyer said. “One part is that long-term Treasurys are up, and they’re going to come down.

“The other part is prepayment risk on mortgages, and that’s going to come down, partly because rates will fall and so the risk of prepaying new mortgages will decline.”

Mortgage rates are based on the 10-year U.S. Treasury bond, the underlying so-called risk-free rate of return that investors demand at any given time. Treasury bonds are considered risk-free because they are seen as having the lowest default risk, given America’s history of always paying its debts.

Loans also include a risk component, which is the chance the borrower will default, or in the case of mortgages, refinance and pre-pay when rates are lower, forcing lenders to reinvest at a lower rate.

All of these factors appear to be moving in a good direction for home buyers.

Predictions of Lower Rates and Risk Premiums

An aggressive campaign by the Federal Reserve of raising interest rates to tame dollar inflation that peaked above 9 percent in 2022, has brought inflation down into the 3 percent level today.

The Fed has not acted to increase interest rates since July 2023, and market expectations now see rate cuts as more likely than rate increases, though these expectations were recently tapered by the persistence of inflation, albeit at lower rates.

Morningstar, a market analytics firm, predicted substantial rate cuts by the Fed are in store.

“We expect Fed officials to deliver hefty cuts over the next two to three years and bring the federal funds rate to 1.75 percent to 2 percent by year-end 2026,” stated Morningstar economist Preston Caldwell in a July 17 report. Mr. Caldwell also predicted the 10-year Treasury yield will fall to 2.75 percent, from its current yield of 4.2 percent.

The fed funds rate is currently in the range of 5.25 to 5.5 percent. While long-term rates, like the 10-year Treasury bond, don’t map precisely to fed funds, a short-term rate, they have tended to move in a similar direction over time.

And the risk component of mortgages may be coming down, as well.

The risk for mortgage lenders is less that borrowers default, Mr. Dwyer says, because most mortgages are guaranteed by government agencies such as Fannie Mae (Federal National Mortgage Association), Freddie Mac (Federal Home Loan Mortgage Corporation), or Ginnie Mae (Government National Mortgage Association). Rather, it is that mortgages will prepay, reducing lenders’ returns.

The higher the current mortgage rate, the more likely that borrowers will refinance as rates come down. Falling rates create a virtuous cycle in which lower rates reduce prepayment risk, reducing the risk premium and driving rates down further.

Another factor that has affected mortgage rates is the Fed’s purchases of mortgage-backed securities (MBS) in an effort to stimulate markets following COVID-19 lockdowns and the financial crisis of 2008–09. The Federal Reserve’s holdings of mortgage-backed securities (MBS) increased from virtually zero in 2008 to more than $2.7 trillion in 2022, in an effort to keep mortgage rates low and stimulate the housing market.

Since then, however, the Fed has been working to downsize its balance sheet, selling off its holdings of MBS, which worked in reverse and contributed to higher mortgage rates.

While the Fed still holds more than $2.3 trillion in MBS, the sell-off will eventually taper, Mr. Dwyer predicts. Some of the Fed’s holdings will simply be allowed to mature and will come off the Fed’s balance without being sold into markets.

A Better Market for Buyers and Sellers

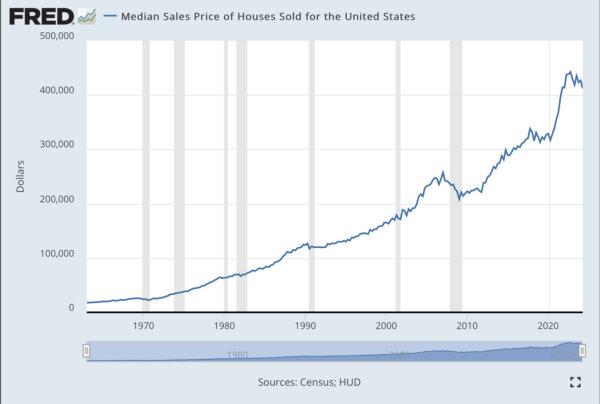

For many homebuyers, watching interest payments more than double over the past three years has put the dream of buying a new home out of reach. And higher loan rates come on top of higher home prices.

According to the Federal Reserve, median home prices in the United States have risen sharply, from well below $400,000 in 2020 to $513,000 as of March.

While things may be moving in a positive direction, real estate markets remain in a slump, with many buyers and sellers still standing on the sidelines. Freddie Mac notes that homebuyers “have yet to respond to lower rates,” and that applications for new mortgages are still about 5 percent below what they were in the spring.

Current home owners who have locked in mortgage rates as low as 3 percent have been reluctant to sell when buying a new home will come with an interest rate more than double that.

“This is not uncommon,” the report noted. “Sometimes as rates decline, demand weakens, and the apparent paradox is driven by buyers making sure rates don’t decline further before they decide to purchase.”

This bodes well for both buyers, who may realize cheaper financing, and sellers, who may see more robust demand when they put their homes on the market. But there is still a lingering gap between buyers and sellers.

“If I have a $400,000 house and I have a 3 percent mortgage, that probably is worth about $50 grand to me, relative to if I had to go out and get a new [loan],” Mr. Dwyer said. “So it means that houses are worth more to the people who own them, who have low-interest mortgages, than they are to other people.”