Respondents to the survey, conducted in May, were divided equally between male and female and had an average age of 39. In addition to savings, many of those surveyed are also planning to use money from a second job or family support to make their home purchase a reality.

More than 78 percent reported that they are also cutting their monthly spending, and 34 percent are leveraging other investments.

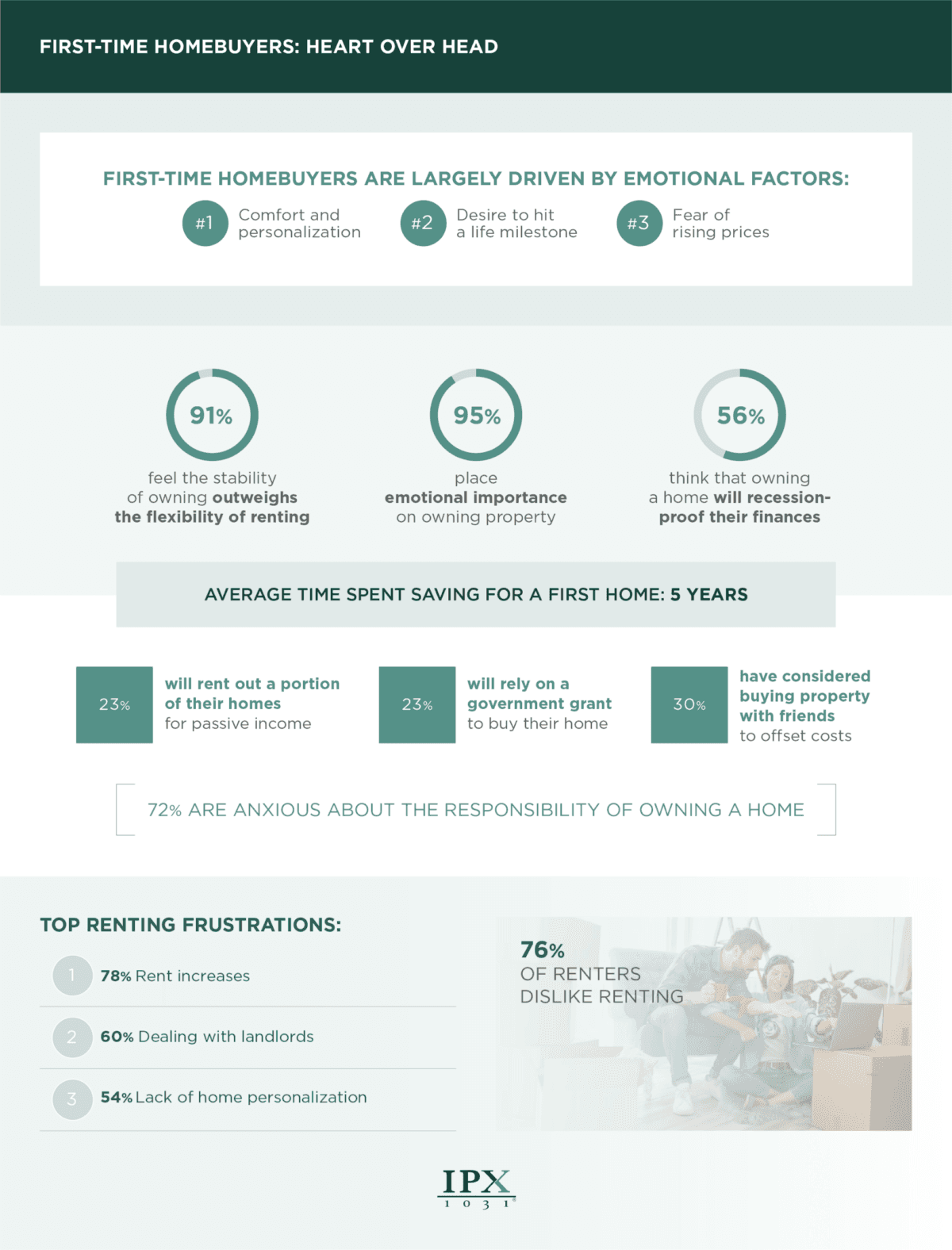

The fear of rising rent costs, coupled with the desire for comfort and personalization, and hitting a milestone, were the top three motivators driving first-time buyers to purchase property. Building wealth came in fourth place.

Emily Fanous, spokesperson for IPX 1031, told The Epoch Times that this is the first time that they have conducted this survey and that some of the results were surprising.

“The average amount of saving time to buy a home is a lot, but we need to think about how the world has changed,” she said.

“Younger people are getting married later than they used to and are delaying home purchases. Rising rents are also making it harder to save money.”

Many younger people are not prioritizing home buying right away, according to Fanous.

“Some of them are using their money to pay off college loans or credit card debt, while others are using their funds for vacations or trips,” she said.

“With the average survey age of 39, people are definitely waiting longer to make a major decision like buying a home.”

The report also found that only a little more than half of those surveyed were interested in home purchasing right now, Fanous said.

“You hear so much about the housing market today, and the average American may be confused or cautious about making such a huge investment,” she said.

Almost 72 percent admitted to having anxiety about the possibility of purchasing a property. Some 23 percent even considered renting out part of their new home to ensure passive income, while 30 percent debated co-buying with friends.

While 42 percent said they would move somewhere else—perhaps out of state—for more affordable options, almost all were concerned about having enough money for a down payment.

But Kimber White, president-elect of the National Association of Mortgage Brokers, told The Epoch Times that most borrowers are not putting down 20 percent.

“The median is probably about 17 percent, and for first-time buyers, it’s more like 8 [percent] to 9 percent,” he said. “There are a lot of programs out there that can help first-time buyers.”

Federal Housing Administration loans can require as little as a 3.5 percent down payment for those who qualify. There are also Veterans Affairs loans, as well as other types of alternative financing.

“The average homebuyer may not know about all of the options available to them, so the first thing they should do before home shopping is meet with a local lender to find out how much they can afford, as well as their financing options,” White said.

“Searching for a home without knowing how much you can spend is like going car shopping without a budget.”

He recommended asking real estate agents and friends for referrals, as well as meeting with more than one potential lender.

In addition, White noted, many banks and mortgage lenders often hold free educational workshops for first-time buyers.

“I think first-time buyers also have to realize that in most cases, that property will not be their ‘forever’ home,” he said.

“They might want to set their sights a little lower just to get in the door and then gradually build toward that ‘forever’ home.”

Some conventional loan programs may require private mortgage insurance with anything less than a 20 percent down payment, but others may not.

White said he believes that the market is starting to settle, and first-time buyers are realizing that rates are probably going to remain in the upper 6 percent range.

“Houses are sitting a little longer on the market, and sellers are more willing to negotiate,” he said. “Some areas, like parts of Florida, are also becoming a buyer’s market—especially with the amount of new construction there.”