Not much has changed in the past month to convince the markets that the Fed is completely done raising rates. Last week’s inflation and retail sales data, chip-sector theatrics, and a host of industry conferences did little to change that. All it did was raise the level of hand wringing before the Fed meeting this week.

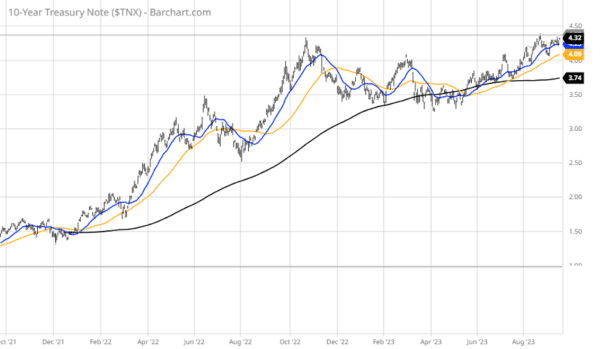

About now, it would be nice to focus on end-of-quarter window dressing, fourth-quarter seasonality, a near-certain Fed pause on a rate hike, and what should be a pretty bullish third-quarter earnings season, but the market landscape bears some elements of caution for the very near term. Namely, bond yields are grinding higher, as Treasury auctions are seeing lower demand, oil prices are trading above $90 per barrel, the United Auto Workers strike reveals wide divisions among union leaders and management, the former and current U.S. Presidents are snarled in political investigations, the ECB is raising rates, and Congress appears to be on track to trigger a government shutdown on October 1, 2023, since it is not expected to pass the 12 appropriations bills that fund government operations before the start of the new fiscal year.

So, should anyone be surprised that traders and investors hit the revolving doors in last Friday’s session? There’s also a lack of trust in American leadership. To say that America has large numbers of unqualified people in high places is a major understatement. For starters, the high-profile diplomatic trip to China by Secretary of Commerce Gina Riamondo and Treasury Secretary Janet Yellen, resulted in nothing of value.

On the home front, Congress faces yet another budget deadline by October 1, and once again there seems to be no regard for fiscal responsibility in Washington. The federal debt is spiraling higher, with the latest Treasury auctions being met with softer demand, implying that real rates will need to be high enough to attract buyers of U.S. debt, which currently stands at $32.6 trillion, the equivalent of almost $100,000 per U.S. citizen. Politicians have turned a blind eye, as if to ignore any bond market revolution, and that doesn’t even get into the oil markets, where the U.S. has little, if any, leverage in bringing prices down.

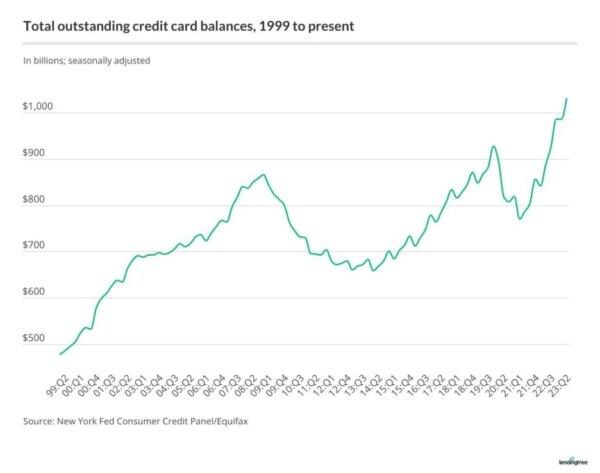

To be frank, I’m surprised that much of the time the market trades as well as it does, considering the incredible vacuum of integrity and leadership that exists on both sides of the U.S. aisle, as well as at the leadership pinnacle of the world’s most important foreign powers. Additionally, there is little mention of how Americans are piling on personal debt at a meteoric pace. While bankers and the financial media claim that U.S. household balance sheets are healthy, the hard data would argue otherwise.

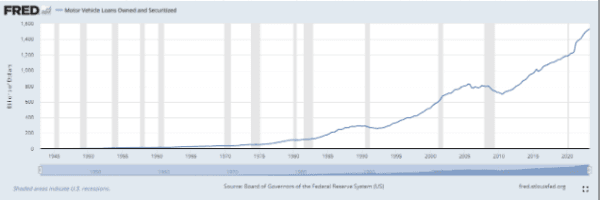

Outstanding auto loans in the U.S. are nearing $1.6 trillion, up 14-fold from 1980 and reaching an obscene number, considering that we’re talking about a rapidly depreciating asset. I suppose this number can be visualized by a costly new car. For example, the base price of some 2023 pickups is over $70,000. Car loans now extend out to 96 months (eight years). A 96-month loan with a 5% interest rate and 10% down ($7,000) commands a monthly payment over $1000 and so, buy my calculations, this will end up costing over $100,000. I think this borders on insanity, but I don’t make the rules, and it’s a free country. It also helps explain this red-flag type of chart.

Still, the largest form of consumer debt in the U.S. is mortgage debt at $12.04 trillion in the first quarter of 2023. Student debt is the second largest form of consumer debt at $1.77 trillion, followed by auto debt and credit card debt, noted above. The student loan repayment pause was stopped on June 30, 2023.

No wonder there’s a labor movement arising in multiple industries. Americans have some big bills to pay.