")

Bernanke led the Fed during one of its most tumultuous periods in history, and expanded the central bank’s powers to alleviate the worst financial crisis this country has seen since the Great Depression.

Whether or not you agree with what he and the Obama Administration have done so far, he’s the only suitable candidate for the job today.

It’s far too late in the game to consider any other candidates for the post.

Wall Street pretty much expected the news, and the stock markets have already factored in Bernanke’s reappointment. He only needs Senate approval, which will be a no-contest as Banking Committee Chair Christopher Dodd is a major supporter of Bernanke and his policies.

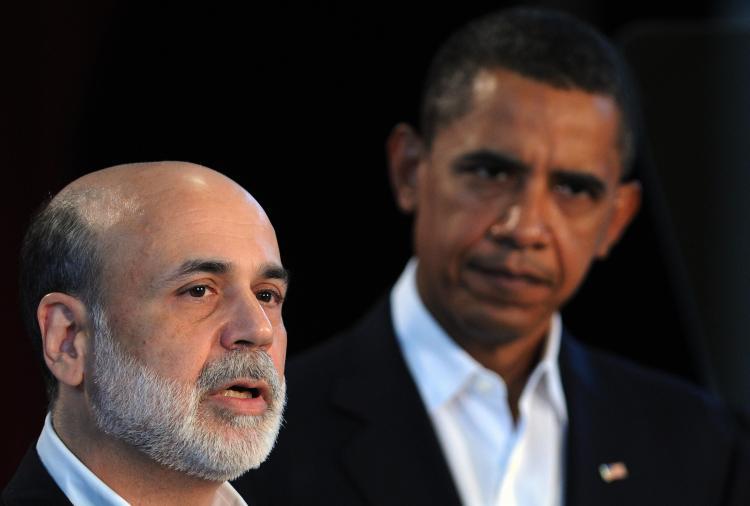

“Ben approached a financial system on the verge of collapse with calm and wisdom, with bold action and out-of-the-box thinking that has helped put the brakes on our economic freefall,” Obama told reporters while on vacation in Martha’s Vineyard, Mass.

Walking a Tightrope

Whether you agree or disagree with Bernanke’s efforts, it’s apparent—at least on the surface—that the U.S. economy is witnessing some stabilization. Housing prices, the quarterly U.S. GDP readings, and job losses—to some degree—have all stabilized.

Bernanke’s next task is tackling what will surely be runaway inflation once the U.S. economic engine starts churning again—and Bernanke himself has acknowledged as much.

Once there are visible signs of economic recovery, the Fed will likely raise interest rates and rein in aggressive lending. It’s been a tightrope to walk for the Fed chairman.

People from across the political spectrum demanded quick action to battle a spiraling U.S. economy late last year. The result: The Federal Reserve created its Troubled Asset Relief Program to pump federal money into the U.S. banking system.

Many didn’t agree with sinking so much of taxpayers’ funds into the private sector, especially a Wall Street industry known for its unbridled excess.

But it wasn’t a decision entirely up to Bernanke. President Obama and his inner circle held much of the power. It was up to Bernanke to implement the program and sell it to the public, and in the end, take most of the blame if it doesn’t work to the public’s liking. Bernanke despises the previous excesses at American International Group (AIG)—he used the term “disgusted” during a Congressional hearing earlier in the year while discussing bonus payments to AIG executives.

Gutsy Moves

I want to point out two instances where Bernanke made controversial decisions that eventually paid off. On Sept. 14, 2008, Bernanke along with Secretary of the Treasury Tim Geithner made the call to let investment bank Lehman Brothers fail after several deals to broker a merger had collapsed.

At the time, AIG’s near-collapse was a wakeup call for the industry, and many analysts feared that Lehman’s failure could trigger a shutdown of the entire U.S. financial system. Many industry insiders at the time criticized Bernanke for his failure to pour more taxpayer funds to prop up the bank.

In hindsight, many overestimated the consequences of Lehman’s fall on the financial markets. On the very day the Fed’s decision was made, the Fed ushered many of Lehman’s trade counterparties to net their trades against each other—a brilliant move that served to stabilize the “over the counter” market. Even had Lehman survived the crisis last fall, the impending commercial real estate market downturn would have put the bank on life support anyway—Lehman held more than $60 billion in commercial mortgage-backed securities on its balance sheet.

On that same day that Lehman’s fate was sealed, Merrill Lynch & Co. sold itself it to Bank of America Corp. (BofA) in what was a shocker to many analysts.

BofA eventually attempted to pull out of the deal in December 2008, but at Bernanke’s behest, Bank of America agreed to complete the merger. To incentivize BofA, the Fed promised more than $100 billion in asset guarantees should the value of Merrill’s assets freefall.

But so far, BofA has declined to accept the cash in fear of greater Fed control. On the other hand, the merger has paid off for both sides. BofA gained Merrill’s strong market experience and client base, while Merrill received a lifeline.

In Bernanke’s eyes, a Merrill collapse would have bigger consequences on the U.S. economy than Lehman’s fall. Merrill’s wealth management division manages the life savings of thousands of Americans, whereas most of Lehman’s activities are in the capital markets.

Expert Reactions

Today, Bernanke’s Federal Reserve, along with the Treasury Department and the FDIC, are tasked with keeping a more watchful eye over the financial industry to make sure the same mistakes made in overleveraging, excessive risk taking, and exotic financial instruments fueled by increasing real estate prices will be kept in check in the future.

Many economists fault Bernanke for failing to detect the asset bubbles created by his predecessor, Alan Greenspan. But once he recognized the problem, most agreed that he took reasonable actions given the time restraints.

“The financial system faced both a liquidity and a solvency crisis, and it is the Fed’s role to provide appropriate liquidity,” said Bill McBride at CalculatedRisk.com.

“Bernanke met that challenge, and I think he is a solid choice for a second term (not my first choice, but solid).”

The critics of Obama’s policies understand that it’s already too late to alter the course of restoring the U.S. economy.

Too much monetary and political capital has been spent, and the next task is to collectively figure out a way to keep inflation and commodity prices in check during the next phase.

Indeed, the Fed has placed all of its chips on Obama’s federal programs. The jury is still out on Bernanke, but a new appointment at this juncture makes little sense, and could be debilitating for the fragile U.S. economy.