At age 25, Jacob Weber left the U.S. Army to pursue his American Dream: raising a family and owning a home.

Years later, half of that dream—home ownership—remains elusive. Instead, Weber, his wife, and their infant daughter are renting a relative’s property while they continue their search for a house within their budget in their hometown of Ocean Shores, Washington.

Like Weber, many young would-be homebuyers are facing what they say is the growing impossibility of achieving homeownership. While housing analysts and real estate agents argue that the dream is very much alive, they concede that for many, it may feel unreachable.

Gen Zers and young millennials who spoke to The Epoch Times highlighted a range of barriers on the path to owning a home, including sky-high prices and interest rates, rising cost of living, and simply not wanting to leave their hometown or family for somewhere cheaper.

Similar stories are common in online groups for first-time homebuyers.

Add to that the perennial issues for this age group: bad or no credit, college debt, and low wages, as observed in online forums and groups.

Housing market analysts, economists, and real estate agents who spoke to The Epoch Times confirmed the sentiment but predicted brighter days ahead.

The increased cost of living and high rental prices make the idea of saving money to put toward his American Dream increasingly difficult, Weber told The Epoch Times.

The 30-year-old veteran finished his military service in 2022 and now works as an automotive technician. He began renting a family member’s vacation home, thinking that it would be a temporary move.

At the time, Weber said, his mindset was: “I don’t know what I’m doing. I just got out of the Army. How about I just crash here for a year or so until I figure it out?”

Years later, he feels stuck, he said.

He and his wife had always dreamed of owning their own house with land. The goal seems unachievable now, because of what Weber said are astronomical prices and a scarce supply of homes in his area.

Even when both Weber and his wife were working, prices around their town seemed out of reach.

The median sale price of a home in Ocean Shores—population 8,200—hovers in the low- to mid-$300,000s. That’s below the U.S. median sale price of a home, listed at nearly $430,000 on Redfin.

Now, with his wife staying home to raise their young daughter, the feeling of unattainability is amplified.

“The American Dream has always been the husband works while the wife is there to take care of [their child],” Weber said.

If the Weber family still had a dual income, buying a home might be possible over time, he said. A couple thousand dollars of debt that they have to pay off prolongs that timeline.

An automotive technician in Washington state earns on average about $71,000 a year, according to Indeed.com. ZipRecruiter.com lists the average at about $59,000.

Americans have not always needed two income streams to afford a home, Weber noted.

According to the U.S. Census Bureau, the median household income in 1960 was $5,620. The median home price was $11,900.

That’s a home price-to-income ratio of roughly two to one, at a time when husbands were primary breadwinners in 70 percent of households, according to a Pew Research report.

In contrast, today’s homebuyers are often advised to look at houses that are about three to five times their annual income.

“I don’t know how they expect to have a family dynamic in America if the family can’t stay home with the kids,” Weber said.

A 28-year-old Marine Corps veteran who lives in King County, Washington, a few hours inland from Ocean Shores, told The Epoch Times that he feels his hope of owning a house is shrinking. He asked to remain anonymous to avoid drawing negative attention to the family business he works for.

“There’s a stubborn part of me that’s holding out hope that maybe, just maybe, someday I’ll have a house and wife and kids with a backyard for them to play in,” he said.

He said that without those things, he wonders how he could give a child the childhood “they not only deserve but need to make it in the world.”

Economic Factors

The U.S. inflation rate spiked to 9.1 percent in June 2022—a 40-year high largely because of the COVID-19 pandemic—but has since stabilized.For 2025, the consumer price index—which measures inflation as experienced in daily living expenses—rose by 2.7 percent, according to the Bureau of Labor Statistics.

Slower inflation growth doesn’t mean that prices are going down—only that they are rising more slowly. Wage increases fell behind during the inflation surge and have struggled to keep up. However, wage growth did outpace inflation for the past two years, according to Bureau of Labor Statistics data.

These gains aren’t felt among many Americans, though.

However, overall, inflation-adjusted wage growth since 2020 has been close to zero. The median household income in 2024 wasn’t statistically different from that in 2019, according to U.S. Census Bureau data.

Blake Bryan, founder and mortgage loan officer at Gridstone Home Financing, told The Epoch Times that he frequently meets with young families trying to buy their first home. Most often, his clients bring up steep home prices and unfeasible down payments as their largest barriers.

The Trump administration has heard the complaints of would-be homebuyers, and the president signed an executive order preventing Wall Street firms from buying single-family homes.

His administration is exploring other mortgage options to help homebuyers.

Homebuying by Generation

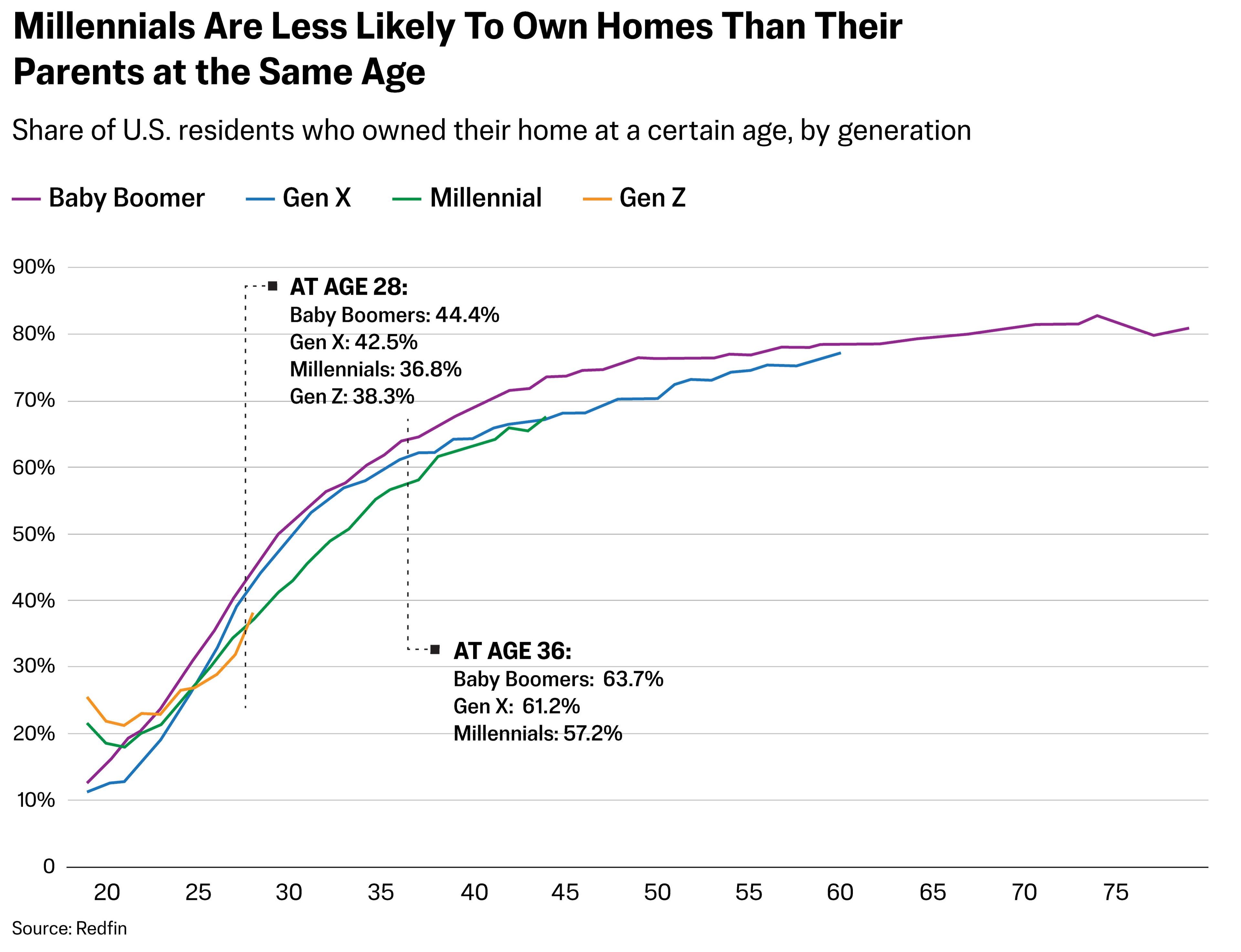

Statistics show that older generations of Americans had more success when they were young homebuyers.Baby boomers, born between 1946 and 1964, came of age during a thriving economy and years of healthy housing construction and continue to dominate the U.S. housing market.

Roughly 51 percent of baby boomers owned a home by the age of 30, according to a Realtor.com analysis of National Association of Realtors and Census Bureau data.

Not far behind are Gen Xers, born between 1965 and 1980. Among this generation, 48 percent owned a home by age 30.

Millennials, born between 1981 and 1996, have surpassed baby boomers as the nation’s largest living generation. They have lived through a vastly different economy and housing market than their predecessors. Still, 42 percent of millennials owned a home by age 30.

However, among millennials approaching age 40, homeownership still lags behind that of previous generations. In 2025, 57.2 percent of 36-year-olds owned their homes. The rates were 61.2 percent for Gen Xers at age 36, and 63.7 percent for baby boomers at that age, according to a January report from Redfin.

Meanwhile, the oldest of Gen Z, born from 1997 to 2012, is only 29 years old now. In 2025, 38.3 percent of that oldest cohort owned a home. That compares with 42.5 percent of Gen Xers, 44.4 percent of baby boomers, and 36.8 percent of millennials at that age, according to the Redfin report.

Moving Home

The Marine veteran served four years before moving back in with his parents in 2021.He said he believed that working for his family’s business, paired with a Department of Veterans Affairs home loan would be his ticket to homeownership. But even with a preapproved loan of $400,000, homes were out of his budget.

Single-family homes were neither within that amount nor within a reasonable commute to his family’s business.

His only options appeared to be a mobile home, which didn’t qualify for a Veterans Affairs loan because of its location in a mobile home park, or a condominium, which he compared to the barracks he lived in while serving in the military.

By the Numbers

A December 2025 Bankrate analysis showed that anyone earning the median U.S. income is priced out of 75 percent of homes on the market.

The median household income for 2024 was $105,800, according to the most recent Federal Reserve Bank of St. Louis data, while Redfin reported the national median sale price of a home for 2024 to be $428,200.

The U.S. housing market finished 2025 with a slight uptick in home prices, according to Redfin. However, price growth on homes had slowed gradually since the beginning of 2025. The year-over-year increase in November 2025 was the smallest in Redfin’s records dating back to 2012.

At the same time, the number of U.S. homebuyers in November 2025 had dipped to 1.43 million, its lowest level on record, with the exception of April 2020, when COVID-19 put a choke hold on the market.

Another Redfin report from January shows home sellers outnumbered buyers by a record margin. It’s a buyers’ market for those who can afford it.

Meanwhile, homebuyers are canceling deals at the highest rate on record, Redfin reported.

Location, Location, Location

Family is often both a motivating and limiting factor for first-time homebuyers. Many are looking to stay close to their relatives, while at the same time needing homes that will accommodate their own growing families.Gen Zers or young millennials having trouble buying a home are often advised to move to a more affordable area. But they say it’s not that simple, especially for a family with young children.

“We have a lot of family here, so we are bound to Washington in that context,” Weber said.

“We want our kids to grow up the same way we [did], where they know all of their family. They don’t see them just once or twice a year on holiday.”

The Marine veteran reaffirmed this view. He wants to remain near family. That may not be possible for him, however, as most developments in his area are condos, apartments, and company-owned homes to rent.

Although he has been told that the housing market “isn’t bad on paper,” he said, in practice, he’s finding it less than hospitable.

Thinking Cheap

David Moore, 27, grew up in Bowling Green, Kentucky. He said he was fortunate enough to have a stay-at-home mom to raise him and his three brothers. All four were homeschooled.His father, whom Moore described as having a well-paying job selling timber, purchased a one-story ranch home on roughly an acre of land in 1999, for about $160,000.

Today, Zillow lists the median sale price of a home in Bowling Green at more than $289,000. According to Redfin, that measurement is slightly higher at about $292,000.

Moore attended Middle Tennessee State University but ultimately quit college to pursue bigger dreams as an aspiring artist and musician.

For the past several years, he has continued pursuing music while traveling for work and living mostly out of his car, in his parents’ home, and at friends’ houses.

But eventually, Moore said, he wants to put down his own roots, preferably close to his family around Bowling Green.

“I want to attract a wife. I want to have children. I don’t want to put them in a position where it’s like, ‘I live in abject poverty, and now you do, too,’” Moore said.

For now, he said, he is content with his lifestyle and making ends meet on roughly $20,000 a year.

Moore said he has accepted the fact that achieving his goal of building a home may stretch a decade or more.

“I’m in a situation now where I’m like, ‘OK, I need to upgrade. I need to grow,’” Moore said. “I don’t really know what I’m going to do.”

Getting Creative

Young homebuyers can turn to several nontraditional options when looking to purchase their first home.The platform is powered by artificial intelligence (AI), automating 95 percent of the home-purchasing process and allowing a purchaser to buy a home without a real estate agent and keep the commission, according to Homa’s website.

While working at Zillow, Javaherian witnessed countless instances of homebuyers’ obstacles, frustrations, or outright aversion to real estate agents, he told The Epoch Times.

He said he designed Homa to eliminate those obstacles and help homebuyers avoid pricey commissions for real estate agents.

The service is currently available only in Florida, but the company has said it plans to expand to Texas and California soon.

For those with an aversion to AI, other nontraditional options exist to help would-be homeowners.

Co-ownership, in which friends, family, or partners jointly purchase a home, is becoming increasingly common.

In the United States, 63 percent of Gen Z and 49 percent of millennials have thought about buying a home with family, according to Coldwell Banker’s 2025 American Dream Report.

Pooling resources with someone who isn’t a spouse doesn’t come without its difficulties, but it does allow young homebuyers a chance at homeownership.

Outside of co-ownership, relatives can provide additional pathways to homebuying.

Family financing involves using resources from relatives and can result in better terms such as lower—or even zero—interest rates.

One common option for family financing is an intra-family loan, in which a relative lends money to the homebuyer for the purchase, typically with lower rates than would a bank. Family members can also co-sign to help a buyer qualify for a bank loan.

Another method used in family financing is gifted funds, in which a relative provides a formal cash gift to assist with a down payment.

Federal Solutions

In December 2025, Trump pledged to introduce “some of the most aggressive housing reform plans in American history.”The next month, in an executive order titled “Stopping Wall Street From Competing With Main Street Homebuyers,” Trump vowed to “stop Wall Street from treating America’s neighborhoods like a trading floor.”

His administration would “empower American families to own their homes,” he said, with a goal of preserving the supply of single-family homes and increasing pathways to homeownership.

Other possible federal government solutions being evaluated in Trump’s second term include portable and assumable mortgages.

A portable mortgage would allow a homeowner to transfer an existing mortgage, with interest rate and terms, to a new property instead of being locked into the same house for 15 years or 30 years. With an assumable mortgage, a buyer would inherit the seller’s existing mortgage terms, subject to lender approval.

The government has also floated the possibility of using federal lands to improve the national housing supply.

For months, Trump and other administration officials have urged the Federal Reserve to lower interest rates, arguing that the elevated rates make life more expensive. The president has accused current Fed Chair Jerome Powell of not dropping interest rates fast enough.

Looking Ahead

Recent housing market data suggest that the American Dream still has life. The young homebuyers whom The Epoch Times spoke to also discussed their optimism for the future.“I have no money. I don’t feel disadvantaged at all. I was born on third base, and I’m running home. I live in the United States of America,” Moore said.

“If all it takes is I gotta save some money, and then I’m gonna scoot over and live in Ecuador—that would be a shame to leave, but I can do that.”

Although homeownership rates flatlined in 2024 for Gen Zers and millennials, a January analysis showed that homeownership rates for both groups increased from 2024 to 2025. Gen Z’s rate ticked up from 26.1 percent to 27.1 percent, and millennials’ rate rose from 54.9 percent to 55.4 percent. Redfin calls the increases “meaningful.”

It’s a trickle, not a flood, the real estate brokerage said.

“Gen Zers and Millennials are making small gains in homeownership because they’re eager to buy, they’re making sacrifices, ... not because homes suddenly became affordable,” the report reads.

Redfin predicts that homeownership among Gen Zers and millennials will continue to slowly grow this year, “with housing costs dipping slightly while wages rise.”