Financial markets are always adjusting to the new reality. Sometimes they get ahead of themselves and then they retrace. Case in point: reacting to the election of Donald Trump.

The U.S. 10-year bond yield surged, along with stock markets, after Trump’s win and reached a peak of about 2.60 percent in mid-December. It hung in a range of roughly 30 basis points (0.3 percent) before starting to fall sharply in mid-March.

Now many market observers are calling for the 10-year yield to hit 2.00 percent, a level not seen since around the U.S. election last November.

The so-called “reflation trade”—higher economic growth and inflation as a consequence of Trump’s victory—is certainly unwinding given the diminishing hopes and/or increasing delays of growth-supporting fiscal measures.

Rally Built on Hope

“Soft” economic data like surveys and sentiment indicators shot up after Trump’s election victory. “Animal spirits” were back.

However, “hard” economic data has started to weaken. While the headline figure for the March jobs report was just 98K, April 14th’s weaker than expected inflation and retail data are more worrisome for the Trump reflation trade.

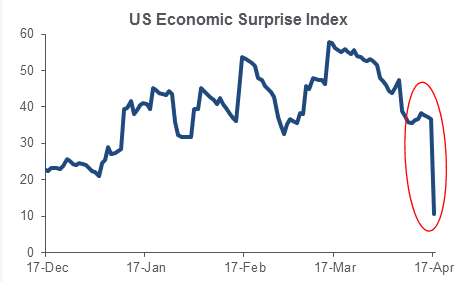

Citi’s economic surprise index (ESI) dropped sharply after the data was released. The ESI, which had been pushing higher in positive territory, indicates that U.S. economic data—driven by soft data—had been coming in stronger than expected. The ESI move is the sharpest since November.

Market-based measures of U.S. inflation dropped to their lowest levels of 2017 on April 17 in reaction to the April 14 data.

The Obamacare repeal and replace didn’t get done. Gridlock in Washington is a reality now. It is threatening to pour cold water on consumer confidence that is at post-financial crisis highs.

David Rosenberg, chief economist and strategist with Gluskin Sheff, said in an interview with Bloomberg, that he expects the soft data to follow the hard data lower. He said there’s still room to run in this bond market rally—or “de-risking phase”—as only a portion of the run-up in yields since the election has been reversed.

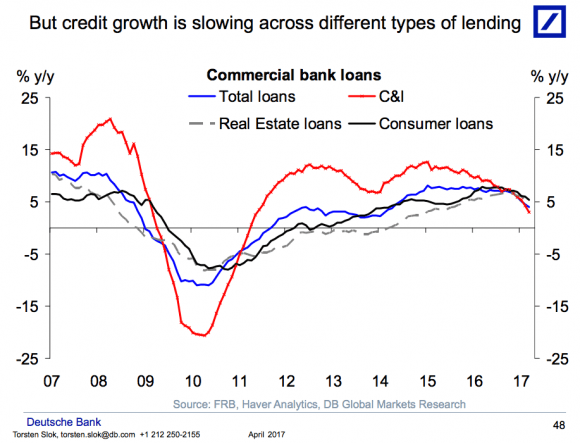

Banks are even tightening their lending standards, according to analysis from Deutsche Bank’s chief international economist Torsten Sløk. If the banks’ spigots aren’t open, then businesses won’t be making investments to grow their operations and economic growth will stall.

“The risks are rising that companies and banks hold back credit as they wait to see more details about what policies are actually coming from the new administration,” said Sløk in an email.

The 10-year yield is not moving lower just because of doubts about the Trump administration’s ability to achieve its pro-growth policies and when. It is also a time of heightened geopolitical concerns. Tensions with North Korea are growing and the first round of the French presidential election takes place on April 23.

The uncertainty around these events is causing flight-to-safety buying of U.S. government bonds—lower yields—not unlike the immediate aftermath of the Brexit vote last June. Gold has acted in a similar way.

Gold has been appreciating since mid-March when the cracks started to appear in the Trump agenda. Gold’s appreciation basically coincided with the 10-year yield beginning its nosedive.

The stock market generally brushes off geopolitical concerns, unlike U.S. Treasury bonds and gold. Since mid-March, the S&P 500 is down less than 2 percent. But since the financial crisis, the Fed and other major central banks have been very accommodative to ensure things don’t go too far south.

The stock market generally brushes off geopolitical concerns, unlike U.S. Treasury bonds and gold. Since mid-March, the S&P 500 is down less than 2 percent. But since the financial crisis, the Fed and other major central banks have been very accommodative to ensure things don’t go too far south.

Important market variables are reaching levels not seen since the U.S. election. The market’s fear gauge—the VIX, implied volatility of S&P 500 index options—is an important one, reached its highest level since the U.S. election, though it is still very low historically.

For now, the threat of something worse, like a recession, remains low. Yields on longer-term bonds remain higher than those on shorter-term ones. With the U.S. Federal Reserve potentially raising rates two or three more times this year, the difference between the benchmark 10-year yield and 2-year yield could narrow. This differential reducing—a flattening or even inversion of the yield curve—has been a harbinger of an economic recession.

Market exuberance post the U.S. election was excessively hopeful and now the reality is setting in. Some pullback was probably healthy, but now meaningful progress needs to take place on tax reform, deregulation, and infrastructure spending to justify the levels in the stock market. Otherwise the entire “Trump bump” risks getting unwound.

Follow Rahul on Twitter @RV_ETBiz