As artificial intelligence investment ramps up, some analysts are now drawing comparisons to the early “dot-com” days of the internet and the market crash that followed.

It is a déjà vu moment for Wall Street: A revolutionary technology captures the imagination while capital floods in and valuations begin to put a high price on promises of a future that has not arrived.

Now, as AI spending accelerates and a handful of mega companies dominate returns, financial industry insiders are asking whether the AI boom has crossed the line into market bubble territory, when the price of an asset exceeds its actual value.

Investment experts say this is a potential problem: How much of these reported returns belong to AI, and how much is bundled in with other earnings?

“Right now, stories about the future promise of AI are pushing stock prices higher,” Paul Walker, author and owner of Fil Financial Corp., told The Epoch Times. “When those stories turn into earnings disappointments, prices will fall.”

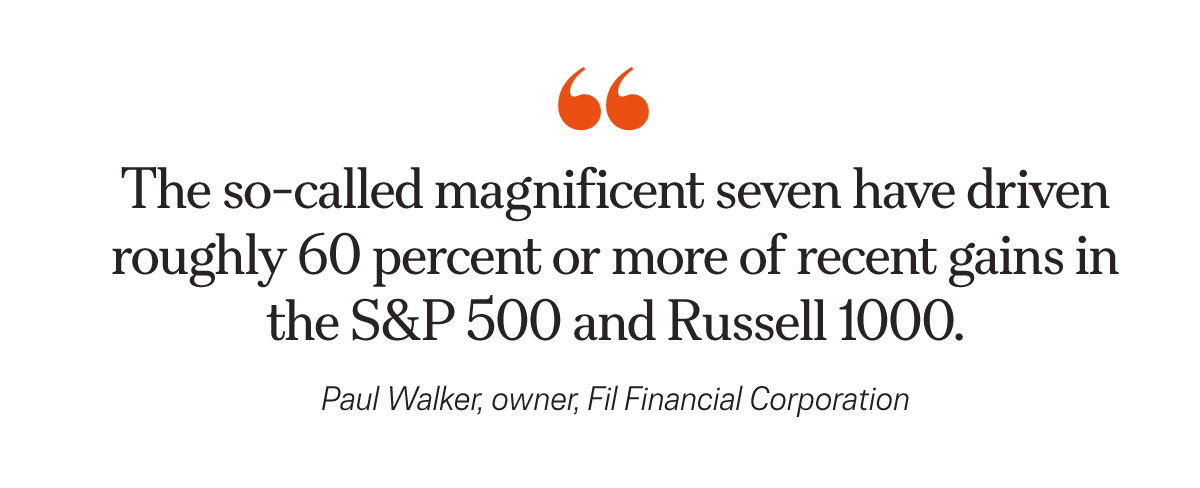

“What most investors don’t realize is just how concentrated the market has become,” he said. “The so-called magnificent seven have driven roughly 60 percent or more of recent gains in the S&P 500 and Russell 1000.

“In other words, people are far less diversified than they think. When those stocks stumble, panic spreads quickly, as investors dump index funds that are loaded with the same tech giants.”

The “magnificent seven” companies include Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla.

“Believers build capacity to meet future demand,” the analysis states. “The bubble begins to form in part because credit is widely available. Decaying underwriting standards and increasing leverage cause a disconnect between economic fundamentals and market valuations.

“More and more investors join the crowd—until fundamentals finally prevail and the bubble bursts.”

Living in a Bubble

Comparisons have been made between the current level of AI investment and the conditions leading up to the dot-com bust of 2000.

In the late 1990s, speculation and heavy funding of internet startup companies or dot-coms pushed the Nasdaq composite index from 751 in January 1995 to more than 5,048 by March 2000. However, with many companies failing to deliver on their promised returns, the market plummeted by more than 75 percent between March 2000 and October 2002. More than $5 trillion in market value was lost during that time.

Dan Buckley, chief analyst for DayTrading.com, said the current situation “doesn’t quite feel like 1999 yet, but it’s similar to 1998.”

“The real bubble typically forms after the technology proves that it matters, not before, as that’s what gets most investors off the sidelines,” he told The Epoch Times.

Buckley said he believes that AI has “crossed that line,” making the current market phase more dangerous.

“Pricing can become even more stretched, and monetary and fiscal policy can become even more supportive of AI buildout,“ he said. ”Governments are also getting involved, as they’re less sensitive to financial returns and see AI as a source of geopolitical power.”

Goldman Sachs observed that investors are becoming more cautious about where they are putting their money.

“The past few months have seen the stock prices of AI hyperscalers diverge: Investors have rotated away from AI infrastructure companies where operating earnings growth is under pressure and where [capital expenditure] is being funded via debt,” the analysis reads.

Goldman Sachs also said investors are opting for companies that demonstrate clear evidentiary links between their AI expenditures and revenues.

“There are some key similarities between AI and [the] dot-com craze, both on the side of investors and corporations,” Pedro Silva, principal partner at Apex Investment Group, told The Epoch Times.

“From the investor side, people want to get in on AI just because they hear it on the news daily,” Silva said. “There is no real scrutiny of the valuations or possible future headwinds; if it says AI and it’s grown substantially, investors want to participate.”

He said it is similar from the corporate perspective.

“Companies have to spend on AI, regardless of whether they see an immediate or obvious return on investment,” Silva said.

Thinking Ahead

Buckley said he believes that most of the reported return on investment with AI is based on vision versus cash flow.“The productivity gains are genuine, even exceptional, in areas like coding, but the investment is ahead of the evidence,” he said. “There has generally been little hard disclosure on how much AI is monetized directly versus bundled into existing products or simply a matter of future promises.”

He noted that any market devaluations related to AI and how they affect individuals largely depend on how their income and savings are linked to technology.

“This [AI] buildout is based on the belief that ‘scale equals control,'“ Buckley said. ”A break in that narrative is what’s likely to bust spending rather than traditional cyclical pressures like declining margins, falling stock prices, or rising interest rates.

“While a pullback in the AI space would reflect on [and] be felt on client statements, the bigger concern would be if it is perceived as a broader economic downturn.”

Silva warned that investors could misread a shrinkage of AI investment as something bigger and make hasty decisions.

Silva emphasized that the top five tech giants are not synonymous with the U.S. economy but that their oversized representation in S&P returns could give that impression, triggering a broader equity sell-off.

Walker pointed out that, over longer periods, the stock market has still shown steady growth, even amid big changes. He stressed the importance of the bigger picture, because today’s market leaders can become “tomorrow’s case studies.”

“Instead of trying to predict crashes or pick the next AI winner, investors should build a risk-based portfolio and rebalance it,” Walker said. “If your plan calls for 40 percent stocks, market drops mean you buy more, not panic. When markets boom, you buy less. Discipline beats prediction every time.”