Medicare Advantage is a super-popular alternative to traditional Medicare, but some experts say it has a hidden flaw that could break the system.

People love the program because many of its plans have zero-dollar premiums (after the standard Medicare Part B premium), benefits that traditional Medicare doesn’t offer, and lower out-of-pocket spending. About 36 million Americans are enrolled.

But there’s a catch.

A series of lawsuits by the Department of Justice has exposed a problem that cost taxpayers billions of dollars, according to the Department of Health and Human Services inspector general.

Simply put, health insurance companies get paid more for enrolling sicker people into Medicare Advantage. That gives them a perverse incentive to identify diseases without treating them.

By adding diagnoses to a patient’s record that no doctor has ever found, an insurance company can increase its revenue even though the patient may never have sought treatment.

Four large insurers have settled lawsuits with the Department of Justice over this issue. Two cases remain open.

Here’s how Medicare Advantage works and why some experts say it’s susceptible to manipulation.

The System

In traditional Medicare, a person goes to the doctor, and the doctor submits a bill to Medicare. Medicare pays the doctor for the service provided.

That’s called fee-for-service.

Medicare Advantage is different.

In Medicare Advantage, Medicare pays an insurance company a monthly fee to cover the patient’s care. So it’s a payment per person, not a payment for a particular service.

When that person goes to the doctor or the emergency room, the insurance company pays for those services using the money it received from the government.

That’s pretty much how commercial health insurance works. The enrollee pays a premium, then the insurance company pays the bills, except for deductibles and copays. The insurer collects a fee for taking on part of the risk.

But there’s a crucial difference with Medicare Advantage.

Risk Adjustment

In Medicare Advantage plans, the risk can be adjusted during the year based on changes in a beneficiary’s health.

Take the case of a 65-year-old with average health living in the Midwest. Medicare might pay an insurer $1,000 a month to provide for that person’s care.

But if that person was diagnosed with diabetes in April, the payment could be increased by perhaps $200 a month.

That’s called a risk adjustment.

If the patient is diagnosed with a new ailment during the year, the insurance company can get paid more based on that diagnosis.

That’s different from regular Medicare, and from commercial health insurance.

Commercial rates for individual and small-group plans are based on a narrow set of factors, like the area in which you live and your age. Large-group plans can consider the experience of insuring the group as a whole.

But insurance companies can’t increase the premium midyear if one of the plan members gets sick. Under federal law, they can’t change it at all based on one person’s diagnosis.

This is the loophole some experts say left Medicare Advantage vulnerable to abuse.

Disease Inflation

At some point, according to the Department of Justice, insurance companies began to inflate patients’ risk scores by sifting through patient data to add diagnoses that, in many cases, no doctor had ever indicated.

The companies were paid more as a result, regardless of whether the beneficiaries ever sought treatment for the condition or even knew they had it.

To the extent those people really were sicker than they or their doctors thought, that presented a legitimate added risk for the insurance companies.

Yet even when those added diagnoses were found to be inaccurate, some of the companies never removed them from the patients’ charts—and never returned the money they had been overpaid for providing care.

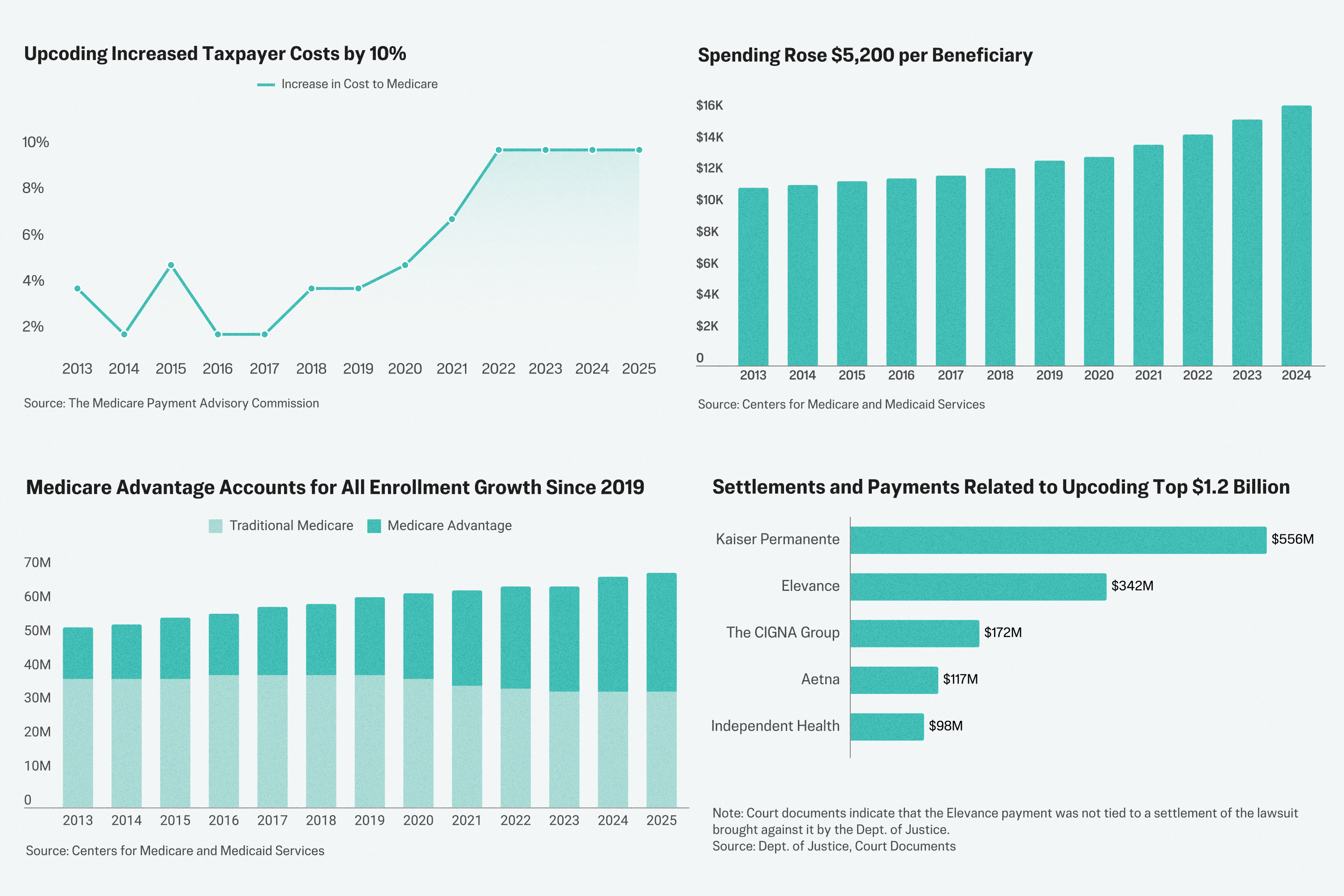

Data-determined diagnoses—diagnoses that appear only in company risk assessments and not in patient charts—cost taxpayers $7.5 billion in a single year, according to the Office of Inspector General. Certain chronic health conditions such as diabetes and congestive heart failure led to increased risk-adjusted payments.

An audit of 97 beneficiaries who were rated as high risk of stroke found that none of the diagnosis codes submitted were supported by physician medical records. That cost taxpayers an estimated $462 million in overpayments, a May report from the Inspector General stated.

Eventually, whistleblowers within six insurance companies caught on to what was happening and filed lawsuits against the insurers, which the Justice Department later joined. The lawsuits alleged that major insurers UnitedHealth Group, Cigna, Independent Health, Elevance (formerly known as Anthem), Aetna, and Kaiser, all engaged in upcoding.

The first whistleblower lawsuit began in 2011. While four of those cases have been resolved, two are still pending, including the initial case against United Health Group.

How It Worked

Here are some examples of alleged upcoding by insurers. None of the companies involved have admitted wrongdoing.

Kaiser Permanente, a large healthcare corporation that includes a health insurer, hospitals, and physician practices, allegedly pushed doctors to add diagnoses to patient charts.

Over a 10-year period, the company mined personal medical data to identify potential conditions for which the patients hadn’t yet been diagnosed, the Department of Justice alleged.

The company allegedly linked physician and facility bonuses to risk adjustment goals.

Aetna, the insurance arm of healthcare giant CVS Health, is alleged to have paid medical diagnosis coders to review patient histories and identify all diagnoses that those histories might support. Aetna used the review to submit additional diagnosis codes to Centers for Medicare and Medicaid Services.

The Department of Justice said Aetna also identified some diagnoses that were not supported by the data, but did not remove those diagnoses and refund money to Medicare as required.

That went on for six years, according to the department, and particularly involved diagnoses of morbid obesity.

Benefit or Flaw

Despite the problems, some industry analysts say the risk-adjustment system is an overall win.

Supporters argue that the risk reviews conducted by insurers provide early warning of chronic diseases and keep them from getting worse.

And the Centers for Medicare and Medicaid Services fact sheet says, “Risk adjustment strengthens the [Medicare Advantage] program by ensuring that accurate payments are made to [insurers] based on the health status ... of their enrolled beneficiaries.”

Others view it as a way for large, data-savvy corporations to pad the bottom line at taxpayer expense.

“My investigation has shown UnitedHealth Group appears to be gaming the system and abusing the risk adjustment process to turn a steep profit. Taxpayers and patients deserve accurate, clear-cut and fair risk adjustment processes,” Sen. Charles Grassley (R-Iowa) wrote in January.

“We stand firmly behind the integrity of our Medicare Advantage business and the positive impact it delivers to millions of seniors across the country,” UnitedHealth Group said in a 2025 statement.

The real problem, according to some experts, is that the Medicare Advantage system itself is deeply flawed.

“It continues to allow financial incentives for providers participating in Medicare Advantage plans to record all possible diagnoses for their enrollees,” according to the Bipartisan Policy Center.

“Risk adjustment was a well-intentioned concept that has grown out of control and overrun with abuse,” Ceci Connolly, CEO of Alliance of Community Health Plans, wrote in 2025. “This is a failing system.”

With 36 million people enrolled in Medicare Advantage as of March, at an average per-capita payment of about more than $14,000, that’s more than half a trillion dollars in annual payments.

Federal administrators are considering reforms that would discourage the inflation of risk assessment, according to The Commonwealth Fund. Those include basing risk on two years’ data rather than one and inferring diagnoses based on claims for services actually provided.

Settlements

Kaiser Permanente settled with the Department of Justice in January. The company did not admit wrongdoing but agreed to make a $556 million payment to the government.

Kaiser Permanente said in a statement the case was a disagreement about how to interpret Medicare’s risk adjustment requirements.

Aetna settled with the government in March and released a statement saying it “continues to disagree with the [Department of Justice’s] industry-wide allegations, and this settlement should not be seen as an acknowledgment of liability,” Reuters reported.

The company agreed to pay the government $117 million.

The Cigna Group settled a similar suit in 2023 as did Independent Health in 2024. The companies agreed to payments of $172 million and $98 million respectively, to resolve allegations of inflating diagnosis codes.

Neither company admitted wrongdoing. Both entered five-year agreements with the government to implement accountability and auditing measures.

The government’s lawsuit against Elevance, alleging that the insurer unlawfully obtained and retains millions in payments under the risk adjustment payment system, remains open.

The government alleges that UnitedHealth Group engaged in similar conduct, increasing risk-based payments some $3 billion over six years and failing to return at least $1 billion in wrongful payments.

A court appointed special master—an attorney or specialized expert delegated to handle specific duties in a case—recommended a summary judgment in favor of UnitedHealth Group in March 2025, saying that the government had not proven its case.

The case remains pending.