Congress responded to the COVID-19 pandemic by passing the American Rescue Plan Act in early 2021. This $1.9 trillion spending bill was intended to provide relief and spark an economic recovery.

Among other provisions, the law expanded the availability of government-subsidized health care through the Affordable Care Act Marketplace to help low- to middle-income people maintain health coverage until the economy normalized. The Affordable Care Act is former President Barack Obama’s health care law, known as Obamacare.

The measure brought millions of middle-class Americans into Obamacare but had the unintended consequence of making many of them dependent on government aid.

The law also introduced temporary, enhanced subsidies, which raised Obamacare premiums, some observers said.

Expanded Enrollment

Obamacare was created for people caught in the gap between Medicaid coverage and employer-sponsored health insurance.The program provides income-based premium tax credits, which are subsidies paid directly to insurance companies, for people whose incomes are on the poverty line and up to four times above the poverty line (between 100 percent and 400 percent of the federal poverty level).

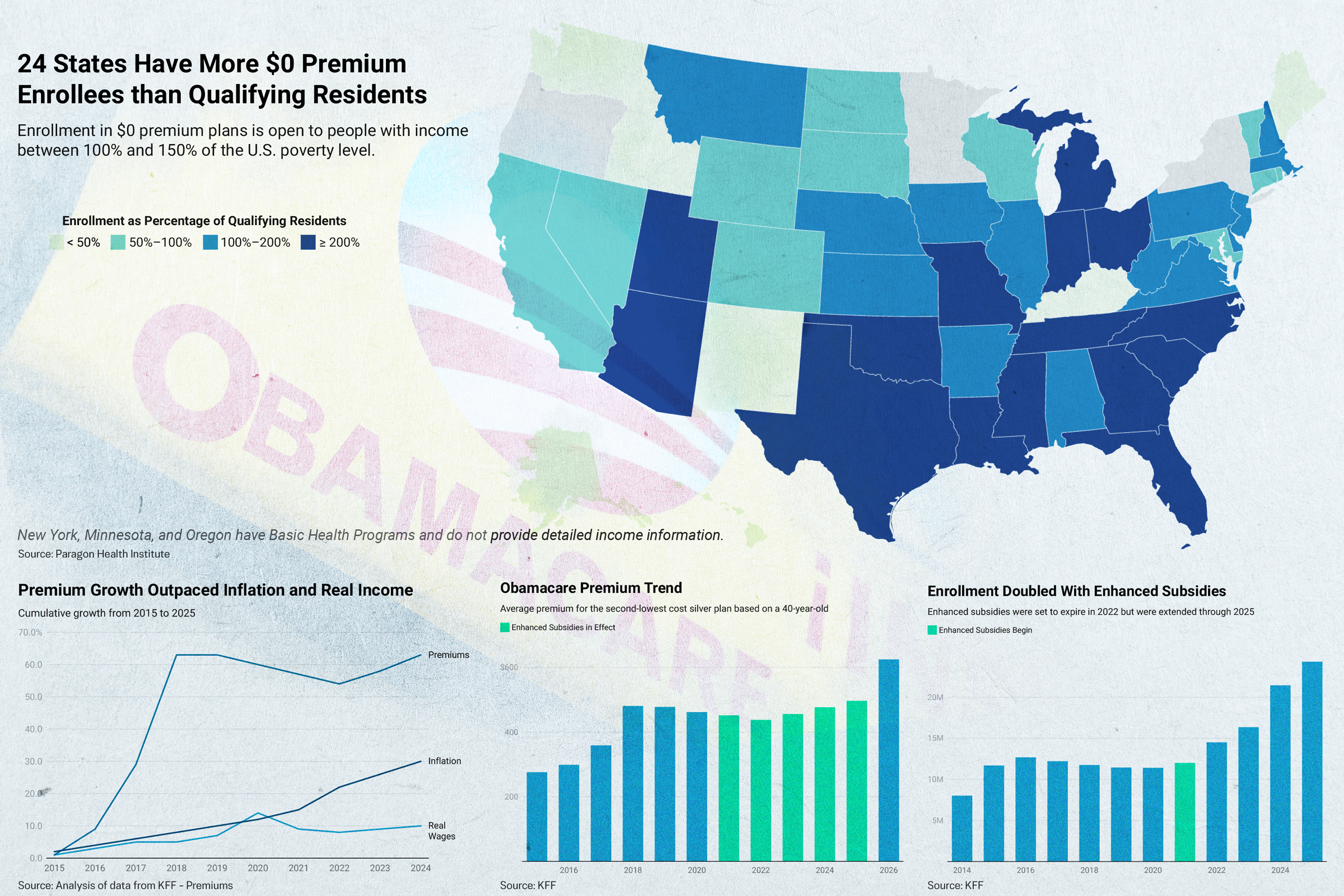

During the COVID-19 pandemic, Congress created subsidies that had no income cap. These enhanced subsidies also lowered enrollees’ affordability cap—the maximum amount a customer would pay out of pocket for a monthly premium.

Under the enhanced subsidies, introduced in 2021, no enrollee would spend more than 8.5 percent of his or her monthly income on premiums. Some would pay no more than 6 percent, others 4 percent or 2 percent, and some would pay nothing.

The enhanced subsidies were set to expire in 2022, allowing just enough time to get people back to work.

But when the COVID-19 pandemic ended, the enhanced subsidies remained.

Premiums Increased, Wages Did Not

Health insurance premiums increased dramatically during Obamacare’s first five years. The average individual premium for a 40-year-old went up by at least 75 percent, according to data reported by KFF.Obamacare prices leveled out before the COVID-19 pandemic hit. During the time from 2020 to 2022, which includes the first two years of enhanced subsidies, prices dropped by 5 percent, according to data reported by KFF.

Economists broadly agree that this was an unintended consequence of American Rescue Plan spending.

Obamacare premiums shot back up, according to data reported by KFF, rising by more than 13 percent in three years.

Many observers also cite the enhanced subsidies themselves as a driver of the problem they were created to address.

“As Congress considers the future of the COVID Credits ... it must confront the reality that the [Affordable Care Act] made coverage far less affordable.”

That reality was largely hidden from many who received the enhanced subsidies because their out-of-pocket premium payments were capped based on income. Price hikes above that cap were paid by taxpayers, which meant that the enhanced subsidies became even more important for people with modest incomes.

Meanwhile, the real wages of American workers were not keeping pace with the price of consumer goods, let alone the skyrocketing cost of health insurance.

At about that time, Rep. Jim McGovern (D-Mass.) commented on the value of the enhanced subsidies to members of his congressional district.

Insurers responded with premium increases ranging from 10 percent to 59 percent, Peterson-KFF found, with the median being 18 percent.

Congressional Democrats argued that the enhanced subsidies had become essential and moved to make them permanent. Some Republicans agreed that a second extension of one to three years was needed.

After five years of premium increases largely paid for by federal taxpayers, both the insurers and the insured appear to have become dependent on the enhanced subsidies.

Increased Fraud

Most Republicans opposed extending the enhanced subsidies. Before spending more money on rising premiums, they said, another problem hidden in the system needs to be fixed: fraud.There has been no dispute among lawmakers that the enhanced subsidies have been a boon to consumers.

The average Obamacare premium for 2025 was $619 per month, of which subsidies covered more than $500. More than 10 million enrollees, 46 percent of those receiving aid, paid $10 or less per month out of pocket for premiums.

That is exactly the problem, according to some analysts, because the possibility of enrolling large numbers of people who would never receive a bill created a ripe opportunity for fraud.

These phantom enrollees are detected in part by their lack of activity once enrolled, Blase said.

“In 2024, nearly 12 million enrollees did not use their plan a single time—up from fewer than 4 million in 2021,” Blase told the House Judiciary Committee on Dec. 10.

Overall, 35 percent of all exchange enrollees never used their plan, and 40 percent of fully subsidized enrollees did not have a single claim, which Blase said is double the rate in both the commercial market and pre-COVID-19 pandemic Obamacare.

“A ‘no-claims’ year is evidence that a consumer stayed healthy or only had a few months of coverage—not that taxpayer money was misdirected or that their policy was illegitimate,” the group said in an Aug. 18 statement.

Investigators were able to enroll 20 nonexistent identities in Obamacare in 2024 by using Social Security numbers that had never been issued to any person and other easily created counterfeit documents.

Of the 20 false enrollments, 18 were still active in September 2025, costing taxpayers more than $10,000 per month.

Investigators also found 26,000 accounts that received subsidies in 2023 based on Social Security numbers that matched records in the Social Security Administration’s death file.

More than 7,000 Social Security numbers belonged to people who were reported dead before enrolling in Obamacare and 19,000 Social Security numbers matched death data by number but not name and address, indicating that false identities may have been created for enrollment.

Taxpayers paid more than $94 million in subsidies for one year based on those numbers.

Another indication of fraud is the number of states where the number of enrollees in Obamacare plans with a zero-dollar premium is unreasonably high compared with the number of people with a qualifying income.

Twenty-four states have more Obamacare enrollees claiming incomes between 100 percent and 150 percent of the federal poverty level than there are people living in the state with that income, according to data from the Census Bureau.

The problem appears worse in states that have not adopted expanded Medicaid, which would have increased Medicaid eligibility to 138 percent of the federal poverty level.

Obamacare customers are automatically reenrolled each year, so a fictitious account would continue to generate fraudulent commissions and wasteful insurance payments until detected.

Making Health Care Affordable

The enhanced subsidies expired on Dec. 31, 2025.Congressional Republicans and Democrats continue to agree that the U.S. health care system has become unaffordable and want to address the problem. They differ in approach.

Democrats generally favor government intervention in the system, as in the case of Obamacare, in which taxpayers pitch in to cover rising costs.

House Minority Leader Hakeem Jeffries (D-N.Y.) said at a news conference on Jan. 5 that his party continues to seek an extension of the subsidies “to protect the health care of tens of millions of ... everyday Americans, middle-class Americans and working-class Americans.”

Without the subsidies, Jeffries said, some consumers would face cost increases of up to $2,000 or more per month.

Republicans generally favor using the power of government to create marketplace competition. Senate Republicans recently presented a plan to provide dedicated funds directly to consumers, which they could use to shop for health care. That plan, too, was rejected by the Senate.

Senate Majority Leader John Thune (R-S.D.) addressed the differing philosophies in a news conference on Dec. 16, 2025.

“If [Democrats are] willing to accept changes that actually would put more power and control and resources in the hands of the American people, and less of that in the pockets of the insurance companies, I think there’s a path forward,” he said.

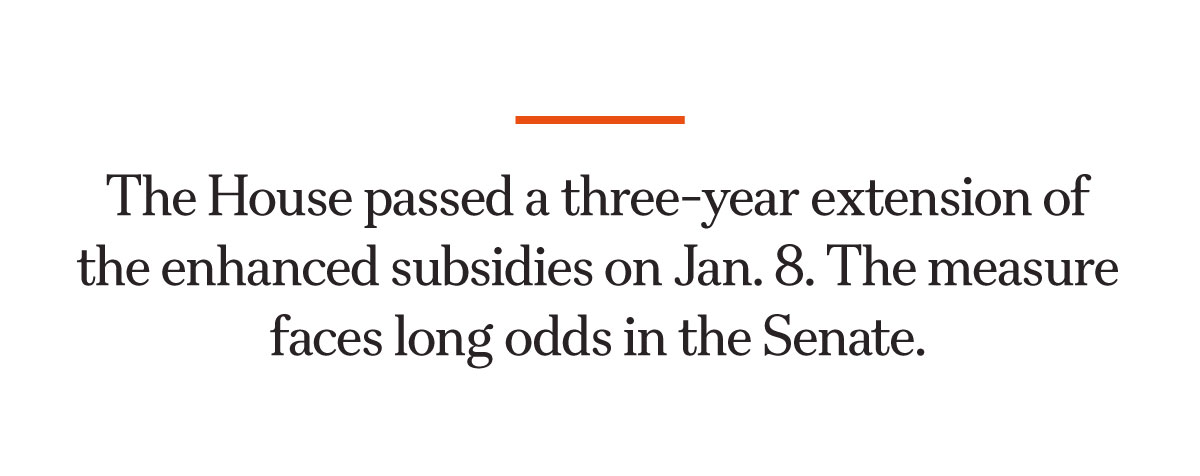

The House passed a three-year extension of the enhanced subsidies on Jan. 8. A bid by Senate Minority Leader Chuck Schumer (D-N.Y) to pass the bill via unanimous consent in the upper chamber failed on Jan. 14.

President Donald Trump has said he would veto any extension of Obamacare subsidies that came to his desk.