This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

This was undoubtedly the week that was. Silicon Valley Bank’s (SVB) failure sent the markets into the worst turmoil since the 2008 financial crisis. And, as I write this Friday morning, St. Patrick’s Day, there are “little fires everywhere” in regional banks that have unsettled markets. Most of them could have been avoided.

What Happened

SVB, the sixteenth largest bank in the United States, catered primarily to an elite cadre of venture capitalists and wealthy individuals. As of December 31, 2022, it held over $26 billion in assets held for sale (AFS) and another $91.3 billion in assets held to maturity (HTM). Some 94 percent of SVB’s deposits were largely venture capital (VC) funds, and their portfolio companies were largely uninsured.

A bank’s whole reason for being is to manage risks: liquidity risk, interest rate risk, and credit risks. Liquidity risk includes duration risk on bonds, which increases as interest rates rise. The longer the bond term, the greater the duration risk. In a rising rate environment, duration risk is particularly hazardous to liquidity risk because a bond with, say, a $1,000 face value may only be worth $750 when a bank goes to sell it to meet liabilities. This is why banks will charge a penalty fee for early termination of a certificate of deposit; it compensates them for the duration risk they have assumed when a customer buys a bank CD but then breaks its terms.

SVB was flush with excess cash—deposits had tripled during the pandemic—and it could not deploy the money in the form of loans to businesses. Instead, SVB took the enormous risk of putting its assets—cash from depositors—into long-term bonds, which have high duration risk, against their related liabilities—those same demand deposits that had provided the money—that had to be paid immediately upon the request of the depositors. When interest rates rose, the bonds SVB had purchased declined, threatening SVB’s liquidity risk. Management moved to issue additional shares to raise cash, telling the markets there was a risk depositors would not be paid. Word soon spread in the venture capital space that was SVBs principal depositors. Soon enough, fund managers and their portfolio of venture entities were moving tens of millions of dollars out of the bank as quickly as they could. A bank run soon ensued, and SVB became insolvent—unable to meet depositors’ demands for their funds.

SVB Failure Affects the Wider Economy

A first-year MBA student could have told SVB to hedge their interest rate risk, but SVB was without a risk manager for some eight months while the Federal Reserve was raising rates. It deserved to fail. And the failure of the FDIC to act earlier against the bank is unforgivable.

Worse has been the Biden Administration’s ham-fisted and inept management of the SVB failure. It should have let the bank fail outright and guaranteed the deposits per FDIC insurance terms, that is, $250,000 per account. Then, the FDIC, the Federal Reserve, and the White House should have waged a public relations jihad against SVBs management and the government regulators responsible for SVB’s oversight. That would include sanctioning the executive management of the San Francisco Federal Reserve Bank, whose job, along with the FDIC regional managers, was oversight of SVB and its risk profile. The president should have fired Treasury Secretary Janet Yellen and Fed Chairman Jerome Powell over the weekend of March 10 and 11 as the two government officials ultimately responsible, and replaced them with an interim panel of “wise men,” retired financial figures whose reputations were beyond reproach and who could stabilize the markets and assure the public, like Ken Langone, the founder of Home Depot.

Such seemingly harsh accountability should not be to lay blame, per se, but to highlight SVBs extreme outlier status; to make clear to the public that SVB was not a “typical” bank; that it was poorly managed, and that it was allowed to continue operations because banking regulators in San Francisco and Washington were asleep at the switch.

As part of the resolution, and to ensure bank depositors, the president should have asked Congress to pass an emergency appropriation to guarantee the uninsured deposits of SVB’s clients of a shorter “haircut” of, perhaps, 10 percent of the uninsured accounts. The funding could be repaid against the total maturity value of the long-duration bonds SVB held on its balance sheet. The SVB depositors’ haircut would be, in effect, a financing fee. Depositors would get 90 cents on the dollar, but the government would get 100 percent of SVB’s bonds when they matured. It would have been uncertain because of the whims of Congress. It would have taken longer, and, yes, payrolls would have been missed, and some businesses—particularly VC-backed businesses—might have folded while awaiting Congress to act, too. But many VC-backed companies could have received lines of credit from their investors or other banks.

Instead, after the fact, the Biden Administration elected to treat SVB as a systemically important financial institution (SIFI) and treat SVB as “too big to fail,” like large money center banks such as JP Morgan Chase or CitiBank. That allowed the Administration to engage in duration risk hocus-pocus, magically transforming the bonds devalued because of interest rate hikes as if they were still at their original par value. So, a bond with a face value of $1,000 but with a current fair of just $750 was treated as collateral still worth $1,000 that SVB could use to borrow $1,000 from the FDIC to pay its depositors.

Try doing that with pretty much any banker and they'll either throw you out of their office, turn you in for attempted bank fraud, or demand a bribe for making the loan on those terms. But the FDIC, the Fed, and the Treasury did it anyway.

Since SVB was made a SIFI after its insolvency, and Secretary Yellen has so far been unable to provide a reasonable taxonomy of what standards would discern banks that “are” SIFIs that would be rescued and which “are not” worthy of rescue, Yellen and others, have exacerbated the risk to regional banks. The FDIC and the Fed’s mercurial, ad hoc decision-making has caused depositors to withdraw their demand deposits from regional banks and move them to large money centers, “too big to fail,” SIFIs. That, in turn, has increased the liquidity risk of the regional banks that finance most of the small and medium-sized businesses that employ most of the American workforce, thus triggering additional risks to the regional banks. Yellen and the Biden Administration’s mismanagement of a single regional bank has started a doom loop for regional banks.

Where We Are Now

I strongly sense that there were and are some opportunistic hedge funds that are short-selling regional banks in a time of crisis and hyping the SVB failure as a threat to the financial system overall, which it is not. Those hedge funds hoped to profit by selling regional bank shares, borrowed from brokers at a high price, and then replacing them with shares at a lower price after they had “talked down” the stock value in social media and the press. I believe such unfounded alarmism—the market equivalent of yelling “Fire!” in a crowded theater—is unethical; it should be criminal. It’s blatant greed—“I got mine, and the devil take the hindmost”—that unsettles markets and is dangerous to the financial welfare of the nation.

Where We’re Going

Regional banks will likely look at loan applicants with a more jaundiced eye and a heightened awareness of credit and liquidity risk.

The Fed’s dual mandates are price stability and full employment. If they hold to those congressionally authorized mandates, they should raise rates by about 50 basis points, or one-half of one percent, when they meet next week.

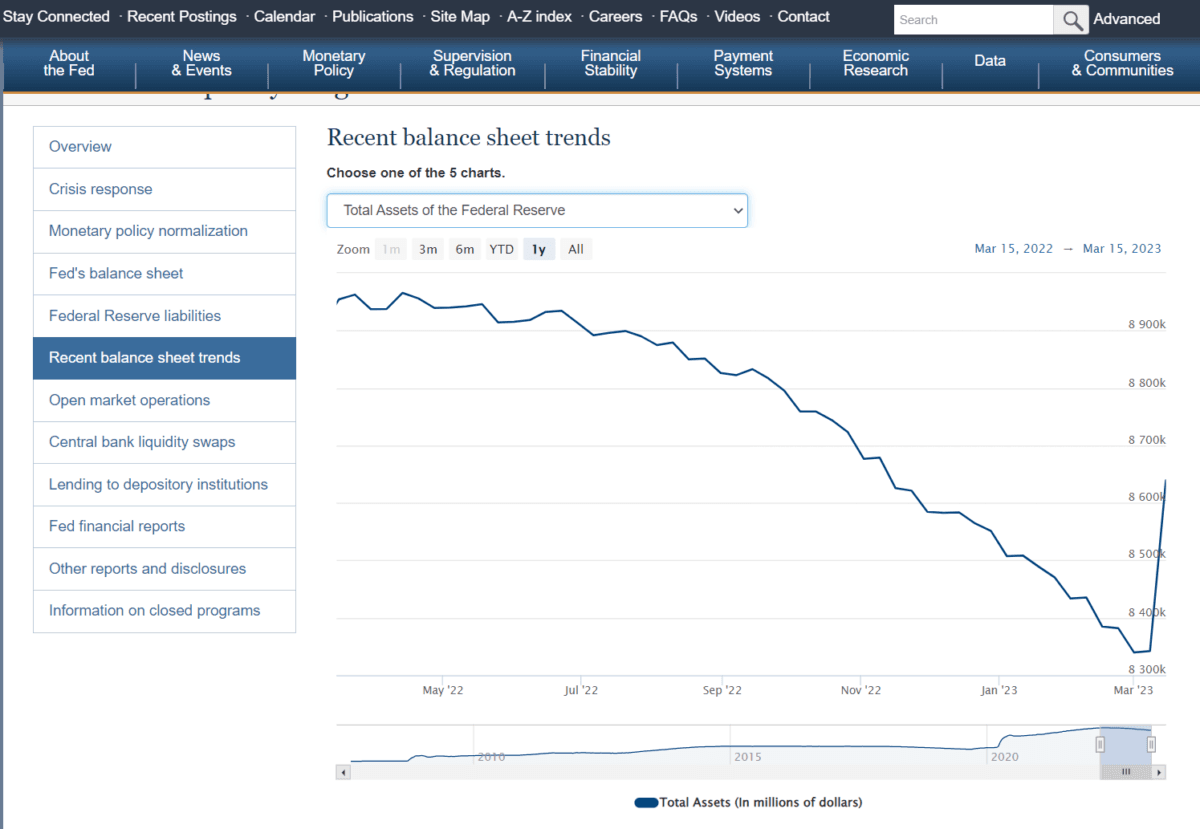

But I suspect they will recognize that regional banks’ enhanced attention to risk will likely slow the economy and go “off script” from their congressional mandates and raise rates only one-quarter point. The chart below shows that the Fed has already reversed five months of quantitative tightening in just 10 days.

Total Federal Reserve Balance Sheet Assets, 1 Year Look Back. Federal Reserve

But that is just part of it.

I believe that, prospectively, VC lenders will be much more restrained in funding their portfolio entities. Instead of handing over large sums of cash for the portfolio entities to manage, VCs will likely invest in small tranches of working capital as needed. Investors in VC and private equity funds may also be prone to heightened scrutiny regarding how the funds manage the cash given to them. Pension funds, institutions, and high-net-worth individuals who invest in VC funds may substitute bank letters of credit to be drawn down when needed. Thus the types of VC funds that were at potential risk in the SVB failure will have to fund their future VC and PE investments with capital calls supported by bank letters of credit to be drawn down only when the VC and PE funds have an investment. This will have a tremendous downside and slowing effect on the economy and restrain growth prospectively. I foresee an era of a dormant, slow, or no-growth economy, a lost generation, similar to Japan from the 1990s. Tragically, it will make China far more potent in our international dealings than the United States. It could even threaten the U.S. dollar’s position as the world’s reserve currency.

J.G. Collins is managing director of the Stuyvesant Square Consultancy, a strategic advisory, market survey, and consulting firm in New York. His writings on economics, trade, politics, and public policy have appeared in Forbes, the New York Post, Crain’s New York Business, The Hill, The American Conservative, and other publications.