This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

May jobs printed at 390,000 new jobs above the consensus estimate of 325,000. The unemployment rate was 3.6 percent, unchanged from last month, but down from last May’s 5.8 percent. The labor force participation rate was 62.3 percent, up from the 61.1 percent that printed in May 2021. The Labor Participation Rate was 62.3 percent, up 10 basis points (bps, defined as 1/100th of a percentage point) from last month. March and April jobs were revised downward by 22,000 net jobs. The U-6 Unemployment Rate, which measures total unemployed, plus all persons marginally attached to the labor force, plus total employed part-time for economic reasons, ticked up again to 7.1 percent from 7 percent last month, but was down from 10.1 percent last year.

Real wages, which we define as annualized average weekly wages minus the 12-month average trimmed mean inflation rate for personal consumption expenditures, for April (the latest available data) were mixed. The professional and business services sectors showed the biggest annualized real wage gains, while workers in the information sector showed the greatest annualized real wage losses. These are the same highs and lows that we saw last month. (We detail this data each quarter, so watch for it in our June jobs report.)

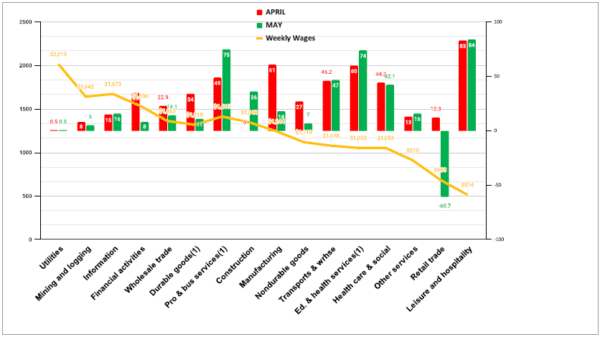

Job gains were earned across a variety of sectors. The best-performing jobs sector was leisure and hospitality, which produced 84,000 new jobs. The worst sector was retail, which lost 60,700 jobs. Construction, which produced no new jobs in April, gained 36,000 jobs in May.

May 2022 jobs by average weekly wages. The Stuyvesant Square Consultancy from BLS Data

Other Data

The Institute for Supply Management’s print of the Manufacturers Purchasing Managers’ Index, the Manufacturing PMI® , registered growth in May at 56.1 percent, up slightly from 55.4 percent in April. A reading above 50 signals growth.

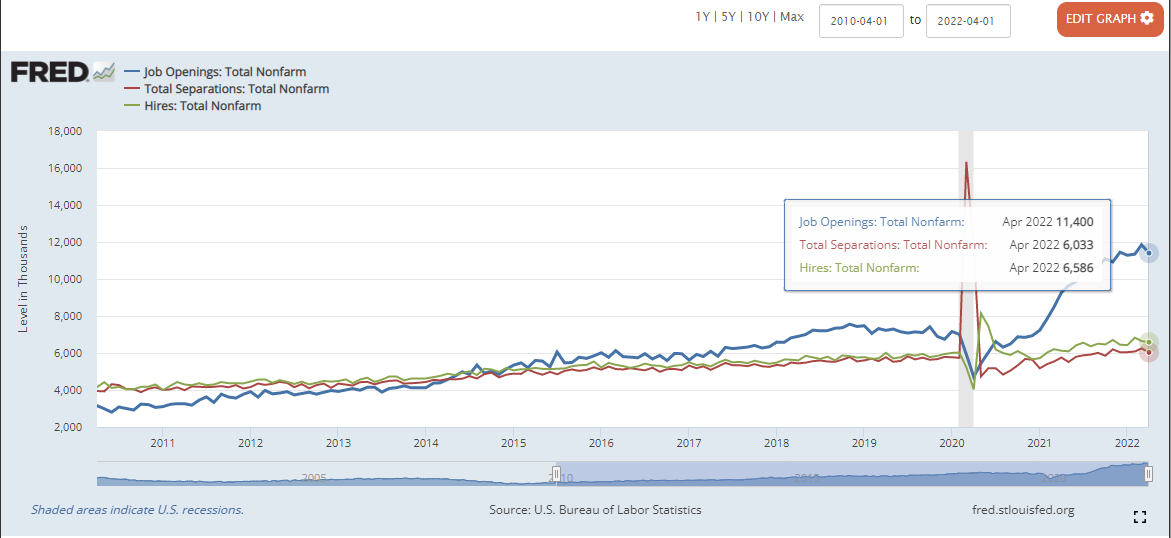

The Job Openings and Labor Turnover Survey (JOLTS) fell slightly in April, the latest available data, as illustrated. Again, as we saw last month, the jobs separation at the height of the pandemic (in green) does not appear to have been matched. The additional job openings will tend to drive wages—and thus inflation—higher.

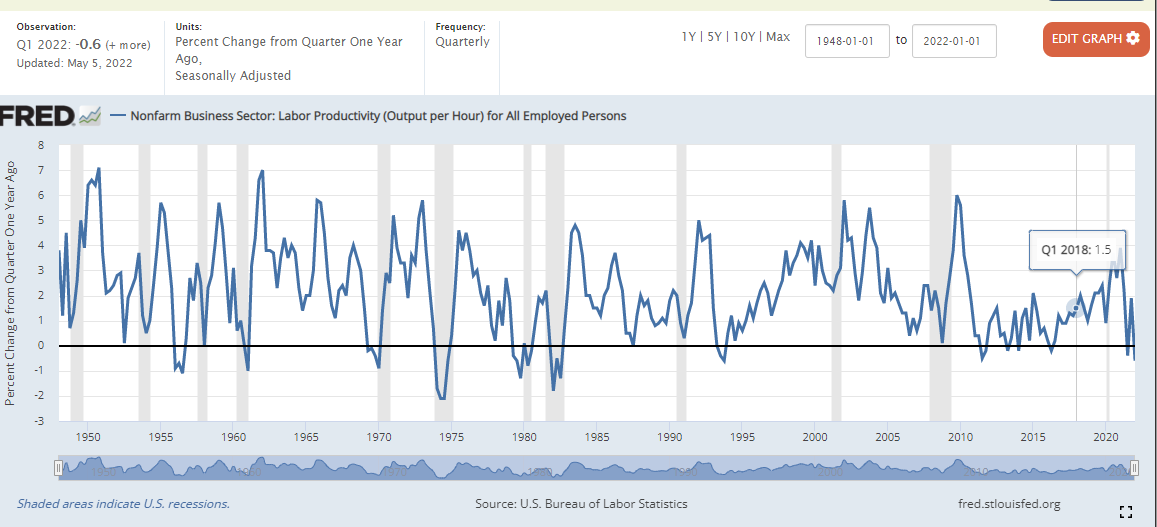

We await second quarter labor productivity, but we note a revision that improved the dismal figure we reported last month. Nevertheless, labor productivity is still the worst in nearly 30 years.

We continue to be disappointed by Friday’s labor force participation rate, which printed at just 62.3 percent, barely changed from last month’s 62.2 percent. Prior to the pandemic, the labor force participation rate was 110 bps higher, at 63.4 percent. Prior to the 2008 financial crisis, it was at 66 percent, further evidence that the economy has not recovered from that meltdown.

The productivity and labor participation rates directly affect the rate of inflation, as we discussed at greater length in our April jobs report.

A good deal of the current inflation is attributable to an excess of money in the economy and the quantity of goods and services being produced. With a relatively low labor participation rate, productivity needs to increase in order to produce more goods and services and lower the inflation rate. Moreover, the shortages in specific critical goods, like diesel and fertilizer, that I discussed here, will cause food—and thus all other—costs to continue their upward trajectory. The decision of the European Union to cut its purchases of Russian oil will likely continue to spike prices for crude petroleum as the artificial barrier to Russian oil.

The IBD/TIPP Economic Optimism Index was down considerably, signaling a sharp decline in consumer confidence that will doubtless affect gross domestic product (GDP) in later quarters. That view was reiterated by the Michigan Index of Consumer Confidence. Both surveys are polls from early May.

Federal Reserve’s Balance Sheet

The Federal Reserve’s decision to finally reduce its balance sheet, something I’ve been urging since last year, will thankfully commence on June 15. Nevertheless, the decision to simply let assets “burn off” at their maturity is insufficient. The Fed should be selling assets to reduce the level of M2 in the economy and to further bring long-term rates into line with inflation.

Evidence that the Fed’s “burn off” policy is insufficient is obvious from a glance at the yield of the 10 year treasury rate. It was over 3 percent on May 9, but has declined fairly steadily now to about 2.9 percent. In my view, as long as the Fed takes half-measures, inflation will continue its upward trajectory, albeit at a slower pace.

Events in the News Cycle

China continues its belligerence toward Taiwan and Japan, even flying sorties over the Sea of Japan and sea drills in the South China Sea while President Joe Biden was in Asia last month. There is no end in sight for the Russia-Ukraine war, and Russia continues to take parts of Eastern Ukraine. Neither the United States nor the European Union nor NATO are making efforts to deescalate or negotiate a peace.

Commentary

The likelihood of a “soft landing” is almost nil. Inflation has run too high, too long, and beating it down will take far more effort than the Fed has imposed. The only question is how steep and how long the recession will be.

While I have advocated previously for a sharp, steep, short, recession to strangle inflation and pull excess cash from the economy, news earlier this week made me more cautious. Bloomberg reported that as many as one-third of Americans earning $250,000—about the top 5 percent of U.S. earners—are living paycheck-to-paycheck and financing much of their expenses on credit cards. Given this sobering statistic, the Fed needs to proceed much more cautiously than I had previously advocated, to avoid mortgage defaults. Accordingly, we will need a more shallow, somewhat longer, recession to avoid a banking crisis.

That said, both the Fed and the Biden administration need to be more aggressive with both monetary and fiscal policy than they seem to be at present.

Even after the Fed’s series of future half-percentage rate increases, we will still be below r*, or “r-star,” the theoretical natural—or neutral—rate of interest that compensates lenders for the use of money without accounting for inflation. Former U.S. Treasury Secretary Larry Summers has been warning about this for some time. The Fed should actively sell off the bonds and mortgage backed securities that comprise its balance sheet, in order to drive up longer term interest rates.

The administration should be looking at policies that will induce private investment, employment, and productivity over government stimulus. As discussed above, a low labor participation rate has been a drag on the economy since the 2008 financial crisis.

First, both the administration and Congress need to clearly define U.S. energy policy, particularly the mix of carbon, renewable, and nuclear energy that will power the economy for the next 30 years, and the target dates for the mix in five-year year increments. This will allow investors, particularly those in the oil and gas industry, to plan out their capital investments. Right now, investors are uncertain how governmental policy will affect their investments. They think the administration and Congress are hoping to effect a green energy transition as soon as possible. Investors worry that they will implement policies to achieve the transition with little, if any, warning. Consequently, they hold back on investment across the entire spectrum of energy investments, fearing their investment will be lost.

Second, the Trump tax cuts should be made permanent. This would signal that business and investment, not government transfer payments, will power us through the measures needed to break the back of inflation.

Third, the White House should encourage states, cities, and private employers to move toward a “return-to-the-office” policy to revitalize cities—where so much of retail, food service, and other drivers of the economy are located. Jobs that can be done remotely can be done anywhere, and the ongoing demand by workers to telecommute could give employers the incentive to offshore U.S. jobs to India, the Philippines, and elsewhere, where wages tend to be significantly lower.

We continue to believe the most likely scenario is a recession starting in the second quarter of 2023 and declared in the fourth quarter. Meanwhile, we think second quarter GDP will print at around 1 to 1.5 percent.

Investing

There are not a lot of good choices in investing. As we advised some months ago, we are in a risk-off market.

It’s a good time to hold cash and AAA or AA bonds. (I would avoid big-city municipals and their insurers for multiple reasons beyond the current economy.)

In equities, commodity-ETFs (exchange-traded funds) are probably best, particularly those in the energy sector. Consumer staple ETFs that invest in things like food, cleaning products, health care, and pharmaceuticals are most likely to maintain value over what promises to be a very volatile equities sector. Selected single stocks with good cash flow and a low price to earnings (PE) ratio might also supplement portfolios. Some lower-end retailers with a low PE might be advisable, as well as some leisure and hospitality stocks.

Travel related stocks also seem to be one bright spot, as evidenced by the leisure and hospitality hiring in April and May, but upside potential is likely already priced in. The best advice would be to hold them for now, but with a stop-loss order if the economy slips into recession.

The loss in retail jobs should concern investors, as should April’s nil jobs creation in construction, as these may be “canaries in a coal mine.” Investors should watch their portfolios carefully and monitor data points as they are released.

DISCLOSURE:

The views expressed, including the outcome of future events, are the opinions of The Stuyvesant Square Consultancy and its management only as of June 3, 2022, and will not be revised for events after this document was submitted for publication. Statements herein do not represent, and should not be considered to be, investment advice. You should not use this article for that purpose. This article includes forward looking statements as to future events that may or may not develop as the writer opines. Before making any investment decision you should consult your own investment, business, legal, tax, and financial advisers. We associate with principals of TechnoMetrica on survey work in some elements of our business.

J.G. Collins is managing director of the Stuyvesant Square Consultancy, a strategic advisory, market survey, and consulting firm in New York. His writings on economics, trade, politics, and public policy have appeared in Forbes, the New York Post, Crain’s New York Business, The Hill, The American Conservative, and other publications.