The Reserve Bank of Australia (RBA) remains uncertain as to when inflation will return within the accepted range, and thus some relief for mortgage payers may be likely.

Speaking to Australian Business Economists (ABE) on Feb. 13, the Bank’s Head of Economic Analysis Marion Kohler said inflation was still high, “but it has been coming down, and at a slightly faster rate than our forecasts three months ago.”

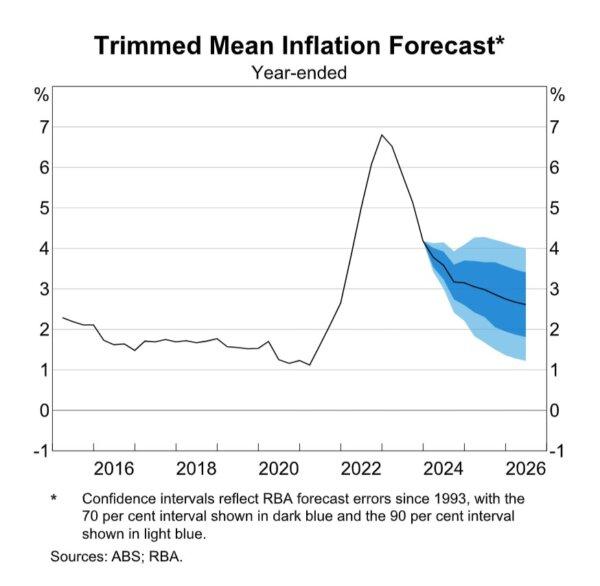

The RBA is expecting it to return to its target range of 2 to 3 percent in 2025, and to the midpoint of 2.5 percent in 2026.

However, Ms. Kohler stressed “there is substantial uncertainty around forecasts that far out,” as illustrated by the shaded blue area in the graph below.

However, the decline to date has not been even across the economy, with most of it due to lowering goods prices, which Ms. Kohler said was the “main driver” of the overall lower-than-expected figure and similar to the experience of many other advanced economies.

“Looking ahead, we expect goods inflation for many categories to be low for a time. This reflects the earlier improvements in global supply chains and below-trend global demand. Recent events in the Red Sea highlight that this moderation in global goods inflation might be bumpy, however,” she said.

Ms. Kohler attributed the disparity to “continued pressure from the level of demand exceeding supply alongside strong growth in domestic costs,” particularly the overall cost of labour.

“We expect wage growth to be around its peak and to decline gradually in line with the easing labour market,” she told the economists.

“We’re already seeing signs of easing wage pressures in some industries, particularly in business services.”

She emphasised, however, that the RBA’s forecast for inflation assumed that productivity growth returns to around its long-run average over the next few years.

“Recent weak productivity outcomes have been an important contributor to high labour cost growth,” she said, though much of this was attributable to relatively short-term influences.

“Examples of these temporary factors are the capacity challenges faced by firms related to pandemic or weather disruptions, capital shallowing (as the increase in hours worked outpaced growth in the capital stock), and additional employee training required given the high turnover and jobs growth we’ve seen in a very tight labour market.

Subdued Economic Activity Ahead

Less positive is the RBA’s outlook for overall economic activity, due to interest rate pressures.“Going forward, we expect economic growth to remain subdued in the near term as inflation and earlier interest rate increases continue to weigh on domestic demand growth, particularly household consumption,” Ms. Kohler said.

“For the next few quarters, the pressure on household budgets from declines in real incomes over the past couple of years is expected to continue to drag on consumption.”

GDP growth, however, is forecast to improve gradually as the effects of high inflation ease. The impact of earlier increases in the cash rate on GDP growth will also start to fade, she predicted.