Politicians are warned against overspending after BlackRock said pre-election pledges might spur “bond vigilantes” into action and destabilize the financial market in the UK.

While opinions are divided on whether investors will get fidgety over fiscal policy, Daniel Lacalle, chief economist at the Madrid-based investment firm Tressis and an Epoch Times contributor, said runaway government spending, when coupled with restrictive monetary policy, will increase the cost of debt servicing and perpetuate inflation.

“Very loose fiscal policy in an environment of rate hikes and monetary contraction” has two negative effects, he told The Epoch Times.

“On the one hand, debt service costs rise significantly. And that puts a burden on the budget in the following years,” he said.

“Also, the level of inflation perpetuates because fiscal policy at the end of the day is printing money, is higher deficit spending and higher borrowing.”

Mr. Lacalle said while the problem of loose monetary policy is already well-known, “the problem of restrictive monetary policy with loose fiscal policy is even worse.

“Because what it generates is a massive level of distortion that makes it much more difficult for finances to be sustainable, and at the same time, the level of debt and balloons without any significant relief for the budget,” he added.

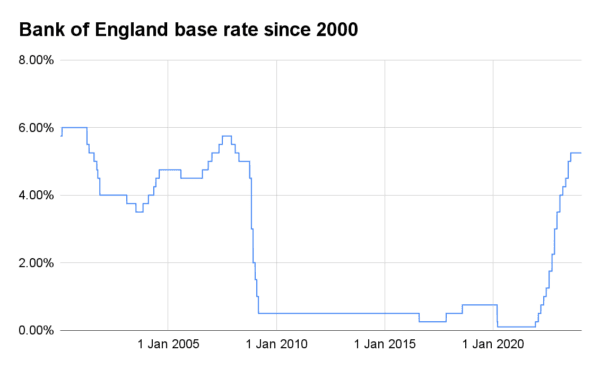

The term fiscal policy means government policy on taxation and spending, while monetary policy refers to the management of interest rates and the total amount of money supply, which is often done by central banks.

During the COVID-19 lockdowns, the Bank of England (BoE) floored the interest rate and increased money supply by buying bonds, a tool known as “quantitative easing (QE),” contributing to soaring inflation that ensued.

After the pandemic, the BoE hiked rates and began reversing QE in a bid to bring inflation down from a peak of 11.1 percent in October 2022 to around 2 percent.

The cost of debt servicing has since ballooned, hitting a record £20 billion in June 2022.

In November 2023, the UK spent £7.7 billion on servicing central government debt, the highest for the month on record.

Consumer Prices Index inflation fell back to 4.2 percent in November, prompting hopes of earlier-than-expected rate cuts and tax cuts, although BoE government Andrew Bailey didn’t make any indication of rate cuts when speaking to the Treasury Committee on Wednesday.

The warning of so-called bond vigilantes came as Chancellor of the Exchequer Jeremy Hunt suggested he may be able to deliver some tax cuts in spring and Labour leader Sir Keir Starmer didn’t rule out reports that he was mulling over tax cuts, and as Sir Keir suggested he may scale back Labour’s “ambition” to spend £28 billion a year on green projects.

Vivek Paul, BlackRock’s UK chief investment strategist, said this week that bond vigilantes is likely to return if parties are not careful with their promises.

“As inflation falls in the UK and we get closer to the general election date, major UK political parties may be more tempted to promise looser fiscal policy—the more this occurs, the greater the likelihood of the return of the bond vigilantes,” he told Bloomberg News.

According to Bloomberg, investors are watching closely as half of the world’s GDP, including the United States, is heading towards a general election this year.

The term “bond vigilante,” coined by investor Ed Yardeni in the 1980s, refers to a bond investor who dumps or threatens to dump bonds, or “gilts” in the UK’s case, over a debt issuer’s policy.

A mass-selling of bonds would push down their prices, prompting more investors to panic-sell them and push up their yields or interests, therefore making it more expensive for a government to service the debt.

Bond market veteran James Athey told The Telegraph that’s what happened when Liz Truss was prime minister.

“It is difficult to argue we have seen much vigilantism, but if there is one developed market where we have, it is most certainly the UK—that is what happened in the Liz Truss era. If you define a vigilante as the bond market disciplining the government, that very much happened.”

However, Trevor Greetham, a portfolio manager at Royal London Asset Management, told the same publication that there was “no obvious vigilante” during the mini-budget meltdown even though “everyone was screaming out at the top of their lungs.”

“Gilt investors are generally life and pensions funds. Institutional investors don’t tend to jump up and down,” he said.

The episode made Ms. Truss the shortest-serving prime minister in British history, leaving Downing Street seven weeks after getting the key.

He also said Labour’s promise, even if it’s not scaled back, is a small amount compared to the UK’s £2.67 trillion public sector debt and that the UK is “in a similar position to France and the [United States], and in much better shape than Italy or Japan.”

The latest estimates from the Office for National Statistics show the total amount of public sector net debt, excluding public sector banks, was £2.67 trillion as of November, remaining at the highest level since the early 1960s.

As the BoE is selling bonds instead of buying them, projections by Japanese investment bank Nomura suggest the UK government will borrow £206 billion from the private sector this year and a record £237 billion next year, according to The Telegraph.

However, the UK isn’t alone in the debt binge. According to the OBR, the UK’s tax burden in 2021 remained below the average across other advanced economies.