It’s not unusual to drive through Australia’s major cities only to see rows of once-unfamiliar Chinese brands—BYD, Deepal and GWM—line parking lots where Japanese and European brands once dominated.

This trend is the manifestation of China’s continuing push down under, particularly taking advantage of the net zero transition and the country’s easy tariff settings.

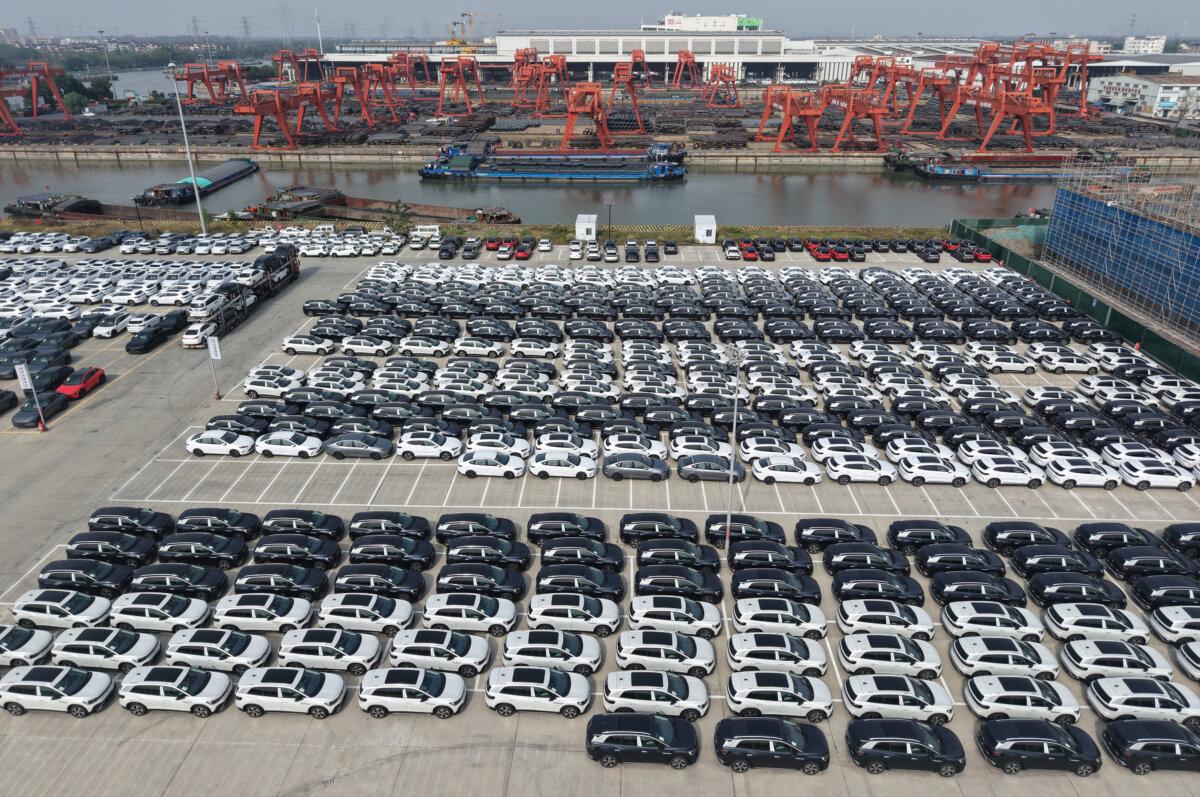

By 2031, the total number of brands will reach 75, a 92 percent increase compared to 2021—all fighting for a slice of Australia’s 1 million-car-a-year new car market.

Just last year alone, eight new entrants expressed their intention to enter the market.

Australia an Easy Market for Global Carmakers

The figures show Chinese-owned brands will continue to make up a significant share, accounting for 22 of the 67 brands in 2026—increasing to 26 of the 75 brands by 2031.

“We are currently seeing an overflooding of the Australian market with new brands coming thick and fast,” AADA CEO James Voortman said in a statement.

“These new brands see Australia as having very attractive policy settings that are geared for the supply of electric vehicles where they can test their product in a Western market with low upfront investment when compared to other Western countries.”

However, the CEO noted that not all of the new and even established brands can stay in the Australian market over the long term.

“Australian drivers will always be attracted to value-based products that offer a quality experience but more so, a quality after-sales experience with reliable and timely servicing and repair work. Brands that cannot compete on that level will struggle,” he said.

The AADA’s data follows a 2025 report that estimated China would become a “dominant” automobile supplier to Australia over the next decade.

The study, conducted by the Centre for International Economics, forecast that 43 percent of all imported vehicles in Australia would be manufactured in China by 2035.

According to the report’s analysis, China’s growing dominance results from several factors: the low retail price of its cars, low vehicle import tariffs, and Labor’s New Vehicle Efficiency Standard (NVES) that preferences lower-emission cars while penalising those with higher emissions.

China’s Overcapacity and Dumping Tactics

In recent years, China has faced industrial overcapacity, driven by a combination of factors, including heavy government subsidies, slowing economic growth and weak consumer demand.As a result, sectors such as steel and aluminium, lithium batteries, solar panels and electric vehicles have experienced an oversupply that cannot be absorbed by the domestic market.

To address this problem, the CCP has resorted to the practice of “dumping”—exporting excess goods at prices below their domestic sale prices or production costs, said Antonio Graceffo, a China economy analyst.

Both the United States and the EU have long raised concerns about China’s industrial overcapacity and goods dumping in the West.

“Fair competition is good. What we don’t like is when China floods our market with massively subsidised electric cars. And we have to tackle this, we have to protect our industry,” she said.

“Chinese vehicles pose the same kind of risks in the physical world that TikTok represents in the digital world,” said Peter Ludwig, co-founder and chief technology officer of tech company Applied Intuition.

In contrast, Australia has not imposed any tariff or taken any measures to curb the flow of Chinese EVs into its market.

At present, Australia no longer produces cars, after Ford, GM Holden and Toyota closed their manufacturing plants.

As a result, the local car industry has shifted from actual vehicle production to supporting roles such as sales, servicing, and specialised vehicle engineering (like converting left-hand drive cars to right-hand drive).