When Goods and Services Tax (GST) was introduced to Australia in 2000, income tax accounted for around 36 percent of the government’s total tax take.

The new consumption tax was sold to the public partly on the basis that the wider government would have an additional source of revenue—which would be given to the states—and not only would a range of inefficient taxes be abolished, but the future need for income tax increases would be reduced.

Income tax as a share of overall GDP duly went down, while GST (substituting for the federal wholes tax) went up.

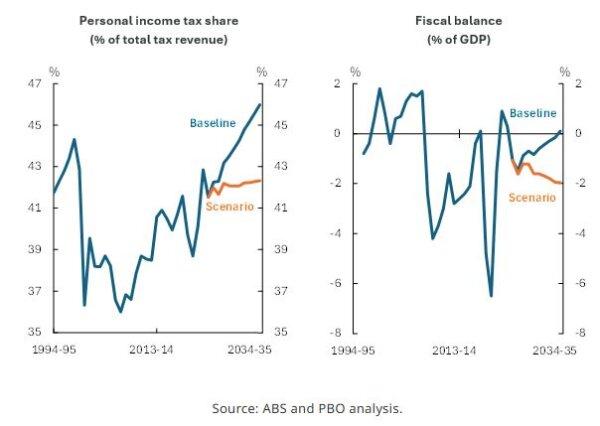

But a study by the Parliamentary Budget Office (PBO) has revealed that personal income tax is headed for a post-GST high of 46 percent of total Australian tax revenue in 2034, due to “bracket creep.”

That is, where tax brackets remain the same, but increases in wages and salaries push an earner into a higher bracket, thus paying more tax.

In total, that’s going to cost Australian workers around half a trillion dollars over the next decade.

The PBO notes that bracket creep in Australia allows the government to go about “repairing the budget over the next decade” while not announcing any rise in income tax rates.

If the government did choose to adjust the thresholds at which people had to pay more tax, it would avoid average tax rates increasing to record levels.

Assuming it decided to go without all the money that bracket creep would otherwise take, the average personal income tax rate would stay at its current level of 24.9 percent rather than increasing to 28.5 percent.

But, in an illustration of just how dependent governments have become on increasing income tax by stealth, it shows how that policy would reverse the trajectory of the Australian government’s fiscal balance and risk the Budget not returning to surplus in 10 years as projected.

The PBO concludes that, unless a future government chooses to increase other federal taxes (or introduce new ones), or reduce the amount they spend, then “future increases in public spending (and revenue shortfalls as some taxes decline) will be funded through bracket creep, further increasing the share of personal income tax.”

Changing the country’s tax mix by only 5 percent would involve policies worth around $40 billion per year—roughly the size of the entire medical and pharmaceutical benefits system and almost equal to Australia’s defence spending.

However, Treasurer Jim Chalmers says the PBO has assumed “somewhat bravely” that there will be no changes to the income tax system for a decade.

He said the stage three tax cuts, which came into effect on July 1 this year, should not be lightly dismissed.

“We cut two rates and lifted two thresholds and that recognises there’s more than one way to return bracket creep in our tax system. And we’re doing it in a way which is best for participation and making sure that every taxpayer gets a tax cut,” he told reporters on Nov. 18.

But that appears to be as far as the Albanese government is willing to go, at least in the foreseeable future.

“People shouldn’t expect us to take a big new income tax cut policy to the 2025 election,” Chalmers said.