News Analysis

An ancillary development to the worsening social-political situation unfolding in Hong Kong is that the city’s global standing as an international financial center has been irreparably damaged.

How the Chinese Communist Party (CCP) and, by extension, Carrie Lam’s government have treated the ongoing protests in Hong Kong is deteriorating to the point of no return. Regardless of how the protests are handled as the calendar marches towards Oct. 1—the 70th anniversary of the CCP’s rule over China—global investors and business leaders have been frightened enough that Hong Kong’s days as a leading business hub and financial gateway to China are numbered.

That’s a terrible development for China and its economy.

Since April, when protests against the now-suspended extradition bill first escalated, Hong Kong’s benchmark Hang Seng Index has fallen by 11 percent. On Aug. 15, the Hong Kong Monetary Authority (HKMA) slashed its 2019 GDP forecast for the city to zero to 1 percent, from 2 to 3 percent and compared to 3 percent growth in 2018.

Hotel prices have fallen, and airline traffic is down—driven by both lower tourism and lower level of business activity. Numerous global corporations have issued internal memos recommending a moratorium on Hong Kong travel. The South China Morning Post—an English-language Hong Kong newspaper owned by Chinese internet giant Alibaba—reported that some five-star hotel rooms have cut their rates to below HKD 1,000 ($128) per night, less than half of the normal rates.

Hong Kong Financial Worries Deepen

Hong Kong serves as the Asia and Greater China regional headquarters for many multinational companies. The city’s residents are fluent in Chinese and English, and Hong Kong’s proximity to China, along with its many freedoms and legal framework, all lend well to international companies in their consideration for a base for regional operations.But the increased meddling in Hong Kong’s affairs by Beijing and the CCP—despite the “one country, two systems” mantra—are undermining Hong Kong’s status.

“Hong Kong’s international reputation for the rule of law is its priceless treasure,” the American Chamber of Commerce in Hong Kong said in a statement in March after the extradition measure was first introduced.

If the business community engages in a mass withdrawal, it will have severe consequences for both Hong Kong and China.

The biggest and most immediate manifestation of business sentiment souring on Hong Kong is capital flight.

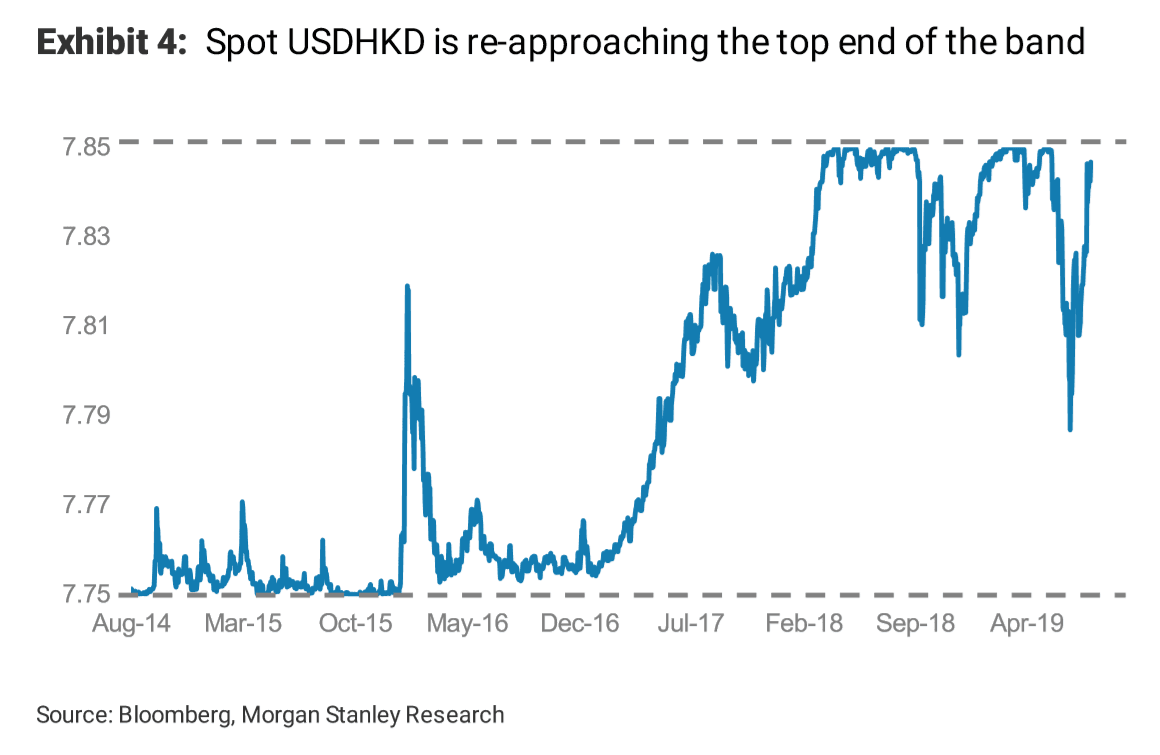

An indication of capital flight is the value of the Hong Kong dollar (HKD). The HKD has been pegged to the U.S. dollar since the early 1980s, but in recent weeks, the currency has settled at the lower end of its range because of the political turmoil.

As the HKD is pegged to the U.S. dollar, the HKMA, Hong Kong’s de facto central bank and treasury, has been spending its U.S. dollar reserves to prop up the HKD currency. In fact, Hong Kong’s interbank dollar liquidity has been dwindling over the last year. Its closing aggregate balance of $54.5 billion on Aug. 23 was 41 percent lower than a year ago, and 70 percent lower since the beginning of 2018.

This squeezes Hong Kong’s dollar liquidity and could force a spike in interbank lending rates (the HIBOR), potentially triggering a banking crisis and ultimately lead to the abandonment of the linked exchange rate system or the Hong Kong dollar as a viable currency.

In an Aug. 20 note to clients, Morgan Stanley analysts cut their 2019 Hong Kong GDP target to -0.3 percent and set a price target of 21,500 points for the Hang Seng index, which represents an 18 percent decline from the Aug. 23 close. While the bank expects the pegged exchange rate system to hold, Morgan Stanley Asia FX strategist Chun Him Cheung expects HIBOR to be volatile going forward, putting stress on the local financial sector.

Hedge fund manager and noted China bear Kyle Bass described the situation more bluntly. “Hong Kong currently sits atop one of the largest financial time bombs in history,” he wrote in a recent investor letter.

HKD weakening against USD Morgan Stanley Research

Hong Kong’s Importance to China

There’s no doubt Beijing has been preparing for a day when China’s economy is completely decoupled from Hong Kong. But that day hasn’t arrived.While China has been less and less dependent upon Hong Kong as an export hub since joining the World Trade Organization, Hong Kong still handles around 15 percent of China’s foreign trade. More importantly, Hong Kong’s status as a regional financial and business center isn’t as easily replaceable. Businesses, investors, and residents fleeing Hong Kong is a true net negative for China.

From 2010 to 2018, Hong Kong has handled about 64 percent of the foreign direct investment into China. Its liquid Western-style capital markets have been a boon for Chinese companies seeking foreign capital. During the same period, Hong Kong was the destination for 73 percent of mainland Chinese companies’ offshore IPOs, 60 percent of all offshore bond issuances, 26 percent of offshore syndicated loans, as well as the global center for offshore yuan (CNH) trading activity, according to data from French global bank BNP Paribas.

There’s simply no viable mainland alternative to Hong Kong. Its highly skilled and English-proficient workforce, free markets, rules-based legal structure, and U.S.-dollar-pegged currency environment can’t be readily replaced.

Despite recent plans by Beijing to reposition Shenzhen—a Guangdong Province city just across the border from Hong Kong—as a major financial hub, its CCP governance structure and draconian social credit system are likely a non-starter for international businesses seeking a new home.

To China’s detriment, the biggest beneficiaries to Hong Kong’s demise will likely be Singapore or Taipei.