This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

Silicon Valley Bank (SVB) failed in spectacular and sudden fashion on March 10, becoming the second-largest bank to do so in our nation’s history and triggering panic in our banking system in the process.

Although virtually everyone knows of SVB’s failure, not everyone understands exactly why it failed. Many have blamed SVB’s environmental, social, and governance policies or “stakeholder capitalism“ for the sudden collapse, but these are really just symptoms of the bank’s ongoing financial mismanagement in the face of catastrophic rate hikes rather than the underlying cause of its downfall.

SVB’s failure also highlights the immense risks facing our banking system, and the Biden administration, Congress, and the Federal Reserve share much of the blame.

These investments were made in a bid to increase the bank’s net interest margin—and thereby jack up its stock price and the stock options held by its management.

The bank made these investments in the midst of massive depositor and asset growth that was made all the worse by its concentrated depositor base of venture capital firms and tech startups.

The accounts of these customers were far larger in size than accounts at the average bank—with most accounts well above FDIC insurance limits. As a result, SVB faced a huge risk of deposit flight from customers whose accounts were primarily overnight demand deposits well in excess of insurance limits.

All of this created the perfect mix for a bank run.

A worker tells people that the Silicon Valley Bank (SVB) headquarters is closed in Santa Clara, Calif., on March 10, 2023. Justin Sullivan/Getty Images

The only thing missing was a sudden and unexpected interest rate move—which is where Biden, Congress, and the Fed come into the story.

Over the past year, the Fed has increased interest rates at its fastest pace in recent history, from zero early last year to the current rate of more than 4.5 percent. It did so in response to inflation brought on by reckless spending programs initiated by Biden and rubber-stamped by Congress. But unexpected spikes in interest rates can wreak havoc on the balance sheets of banks as the higher rates erode the value of fixed-income securities that compose a bank’s assets. As we will see, these rate hikes have endangered every aspect of our banking system.

The prices of these interest-bearing securities are inversely related to rates. As interest rates move higher, the prices of fixed-rate securities such as bonds and mortgage-backed securities fall. The lower a security’s price, the higher its yield or interest rate. And the longer the duration that a fixed income portfolio has, the greater the impact from rates.

Duration measures a bond’s price sensitivity to interest rate changes. In general, the higher the duration, the more a bond’s price will drop as interest rates rise.

By way of example, if rates were to rise 1 percent, a bond with a five-year average duration would likely lose approximately 5 percent of its value. Notably, SVB’s portfolio had a duration of almost six years. And interest rates rose by 4.5 percent in 2022.

SVB had experienced explosive growth, with total assets increasing from $115.5 billion in 2020 to $211.5 billion in 2021, an astonishing growth of 83 percent in one year. Total deposits at the bank went from $102 billion to $189 billion in 2021, a growth of 85 percent over 2020. Put very simply, a bank makes money by taking in deposits and then uses that money to make loans, along with investments in interest-bearing securities.

The interest on the loans along with interest from its investments provides the bank with a level of interest income that is higher than its interest expense—what it pays its clients to attract the deposits.

The difference between what a bank earns and what it pays is net interest income, or spread. The higher the spread, the more money a bank makes.

But here’s the thing: SVB’s asset growth was so explosive that it simply couldn’t make loans quickly enough. So it was forced to invest an ever-increasing amount of its assets into low interest-bearing government and agency securities, from $49 billion in 2020 to $128 billion in 2021.

The securities that SVB was investing in are actually quite safe in terms of repayment, but these securities are also highly sensitive to rate increases. And because these securities are considered very safe, they weren’t going to earn the bank much in the way of interest income, thereby negatively affecting the bank’s net interest margin or spread. This, in turn, would negatively affect the bank’s stock price along with management’s stock options and compensation.

But SVB management had what they thought was an easy solution.

LM Otero/AP Photo

They would simply extend the duration of their investments, buying longer-dated, longer-maturity securities that provided the bank with higher levels of interest income. In general, securities with a longer maturity provide a higher yield than shorter-dated securities. But this strategy comes with the very big risk that we’ve already discussed: interest rate risk.

If interest rates move upward suddenly, long-dated, interest rate-sensitive securities suffer the most in price. The longer the duration of a portfolio, the greater the hit to the current value of that portfolio. And SVB’s portfolio had a lot of duration.

However, SVB still had almost $15 billion in cash and $27 billion of available-for-sale securities away from its long-term portfolio of investments. Nothing to worry about, right?

As it turns out, there was quite a bit to worry about. The Fed Funds Rate, the interest rate at which banks lend reserve balances to other banks, had risen from effectively zero in February 2022 to 4.5 percent in February 2023. Meanwhile, SVB had just completed a massive buy program of fixed-income securities in 2021, directly in front of the rise in rates.

Held-to-maturity securities ballooned from $16.6 billion in December 2020 to a little more than $98 billion by December 2021—an increase of 490 percent. Now, bear in mind, these securities had an average duration of more than five years. Each 1 percent rise in rates caused a roughly 5 percent drop in their value. In addition, the bank decided to add some risky venture capital debt to its portfolio, and although this amount was smaller, it was also concentrated and much more volatile.

But the story doesn’t end there.

For starters, note that the stated value of SVB’s long-term investment portfolio, $98 billion, is held in a category on its balance sheet known as “held to maturity (HTM) securities.” Unlike the $27.2 billion in “available-for-sale securities,” which are carried at current fair market value, the bulk of SVB’s portfolio—more than 75 percent of its investment portfolio—was held on its balance sheet at stated book value rather than the current market value of these securities.

Page 67 of the bank’s 10-K, an annually filed SEC financial statement, makes this quite clear: “Securities classified as HTM are accounted for at cost with no adjustments for changes in fair value.”

The reduction in a portfolio’s value of assets that are intended to be held until their maturity is known as unrealized losses. Although long-term fixed-income portfolios are worth less due to a rise in market interest rates, the securities usually don’t have to be sold—they are intended to be held to maturity—thus the loss of value is unrealized. Nor would this loss have to be realized in a normal environment, as SVB had no intention of selling this portion of its portfolio.

But our interest-rate environment was about to become anything but normal.

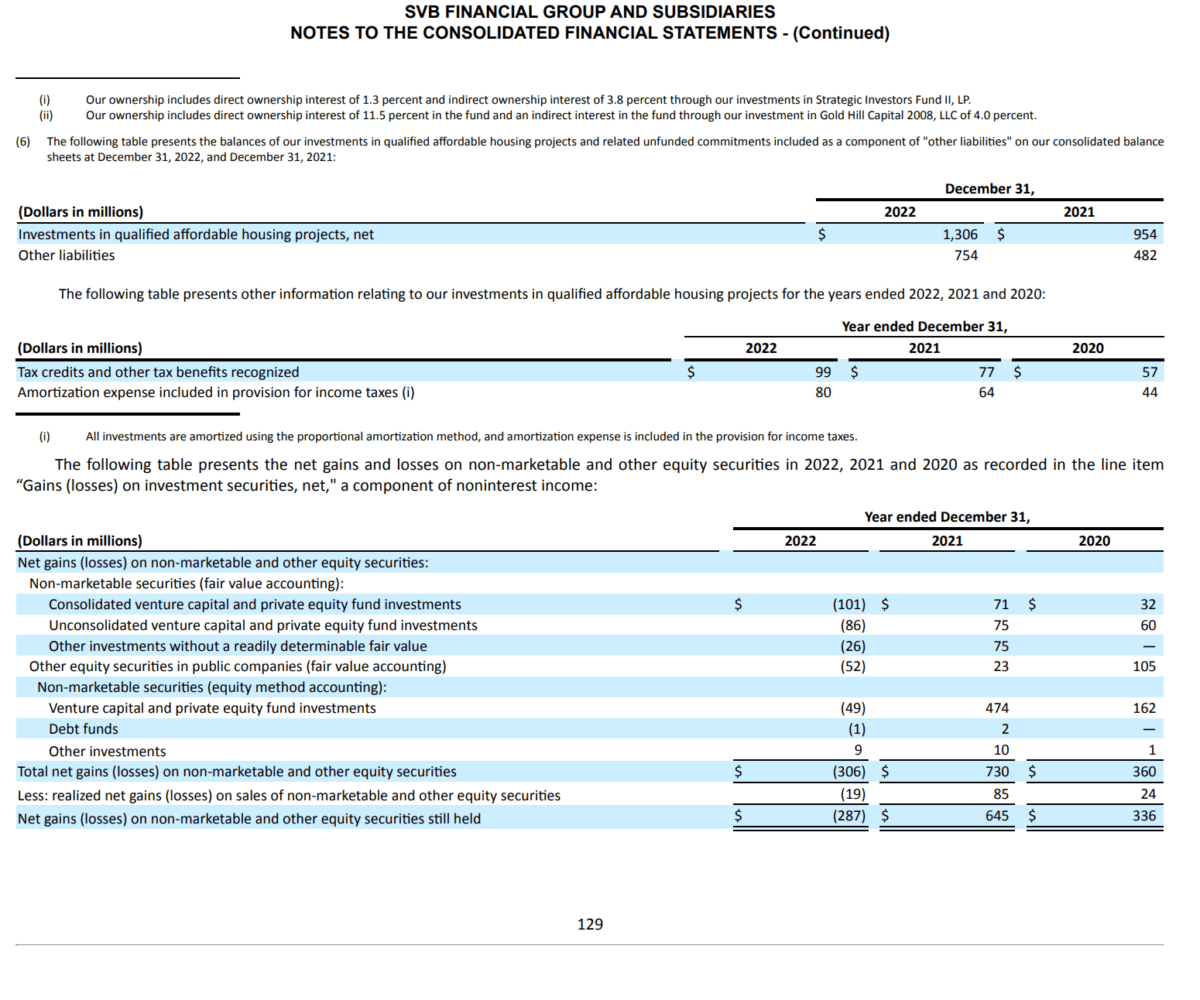

One has to delve deep into SVB’s 10-K to find the unrealized loss on the HTM portfolio. On page 129 of SVB’s 10-K, we can see that the bank had unrealized losses in December 2021 of $1 billion net of unrealized gains. In other words, SVB’s HTM portfolio had a fair market value of $97.2 billion against a book value of $98.2 billion at the end of 2021. Not too bad right? And the firm still had plenty of cash and liquid available for sale securities. But recall that interest rates were effectively zero at this point and they were set to suddenly and dramatically rise in the coming year.

Before we continue, it’s worth taking a quick look at SVB’s depositor base.

As we mentioned at the onset, SVB catered to venture capital firms and tech startups. Its clients were large, wealthy, and sophisticated. As a result, SVB’s depositor base was far more concentrated than that of the average bank. Of equal or greater importance, because of the large account size, most of these client assets rose far above the $250,000 FDIC limits and were largely uninsured.

In December 2020, total deposits were roughly $102 billion. Just one year later, in December 2021, total deposits were $189 billion, an 85 percent increase. And of the $189 billion of deposits, $166 billion was uninsured. Let me repeat that: 88 percent of the bank’s customer deposits were uninsured. To make matters even worse, $126 billion of these customer deposits were non-interest bearing—in a period of rising rates.

Now, let’s fast forward to Feb. 24. It was on this date that SVB’s 10-K for the period ending on Dec. 31, 2022, was filed. It contained some rather bad news. Total assets were stable—almost exactly the same as in 2021—but HTM securities were actually down by $9 billion, and total deposits had dropped by $16 billion to $173 billion.

Worse still, the mix of these deposits had shifted dramatically. Non-interest-bearing deposits were now only $80 billion versus $126 billion in the prior year. Customers were rightly demanding they be paid interest on their deposits, and they were drawing down these deposits at the same time.

There were other obvious concerns as well. The firm had suddenly borrowed almost $17 billion, obviously to cover accelerating outflows.

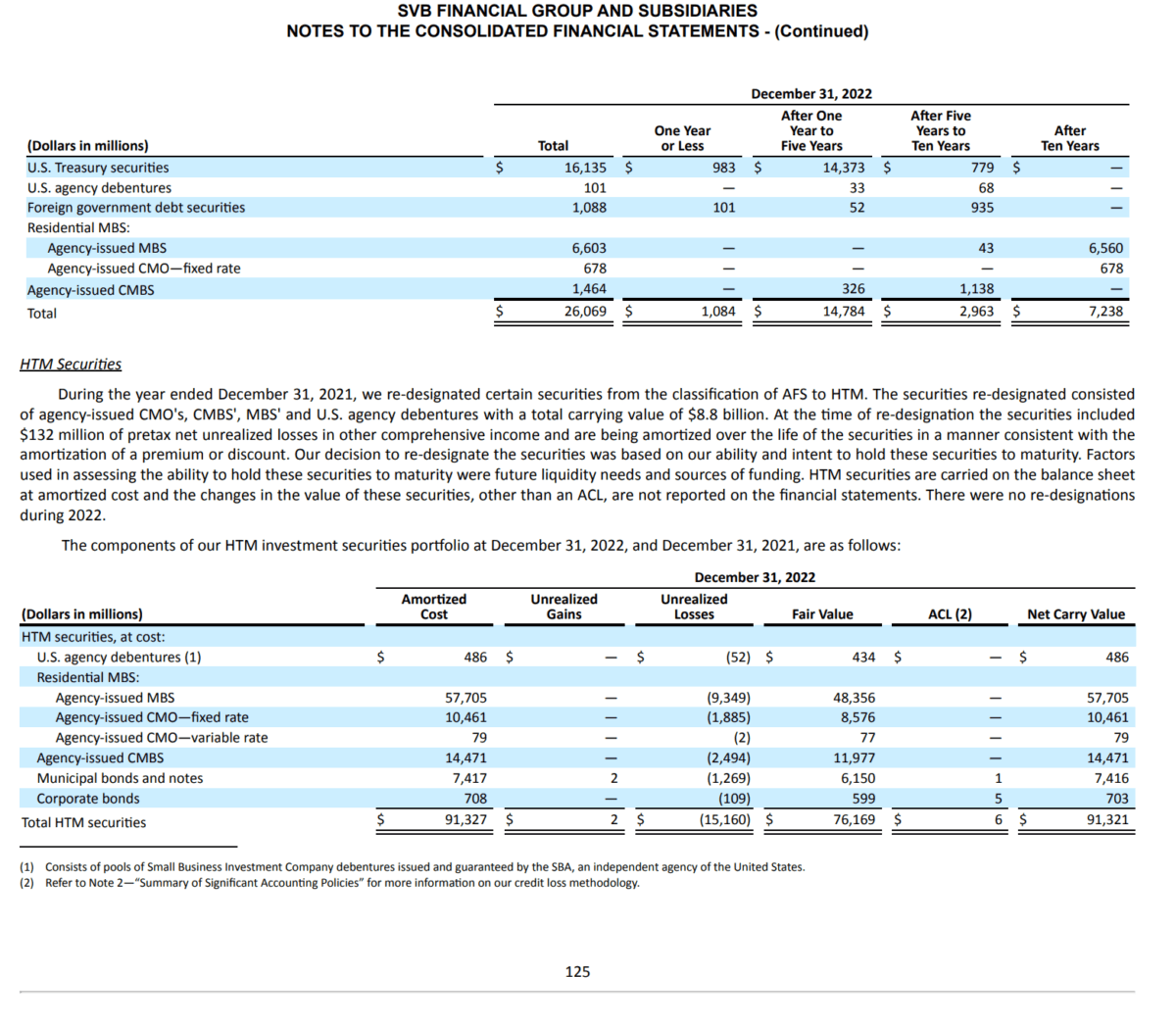

But the truly bad news was found on page 125 of the bank’s 10-K. SVB’s HTM portfolio, now at only $91 billion versus $98 billion just a year earlier, had suffered huge unrealized losses during the year—staggering losses of more than $15 billion.

While the HTM portfolio was carried on SVB’s books at $91.3 billion, it was worth only $76 billion. Investors and depositors alike rightly panicked. Less than two weeks later, SVB announced they had totally liquidated their “available for sale” portfolio, which had been $26 billion just a few months earlier on Dec. 31, 2022. They also stated their intention to raise an additional $2 billion through the sale of preferred shares.

The cash was gone, and SVB was facing a massive liquidity crisis. The following day, SVB’s share price plunged by almost 70 percent. And the onslaught of massive withdrawals far exceeded the bank’s ability to raise sufficient cash. The following day, March 10, the FDIC took over the bank that had once been the darling of the venture capital world.

SVB was the second-largest bank failure in our nation’s history. Just two days later, New York-based Signature Bank also closed its doors at the order of state officials. That bank, which had begun taking cryptocurrency deposits, was the third-largest bank to fail.

There is a postscript to this story, and it’s a scary one that’s still developing. In a Feb. 28 speech, FDIC Chairman Martin Gruenberg casually said, “Unrealized losses on ‘available for sale’ and ‘held to maturity’ securities totaled $620 billion in the fourth quarter.”

Chairman of Federal Deposit Insurance Corporation (FDIC) Martin Gruenberg. Alex Wong/Getty Images

Gruenberg then went on to note, “There has now not been a bank failure in 28 months, three short of the record of 31 months set in 2007.” Gruenberg made his remarks just four days after SVB’s 10-K disclosures and 10 days before the FDIC would take over SVB. Although the market reacted strongly, at the time, we thought Gruenberg’s estimate of unrealized losses for the banking system was remarkably small.

Unfortunately, we may have been right.

A study released on March 13 took a deeper look at the unrealized losses banks were likely holding. The study found that the actual losses to banks’ security holdings were $780 billion, not the $620 billion estimated by the FDIC.

But the authors went deeper, rightly noting, “Loans, like securities, also lose value when interest rates go up.”

They found that total unrealized losses as of December 2022 were $1.7 trillion. In a chilling warning, the authors noted that “the losses from the interest rate increase are comparable to the total equity in the entire banking system.”

We’re not out of this banking crisis. In fact, it may be just the beginning.

Before we continue, it’s worth taking a quick look at SVB’s depositor base.

Before we continue, it’s worth taking a quick look at SVB’s depositor base.