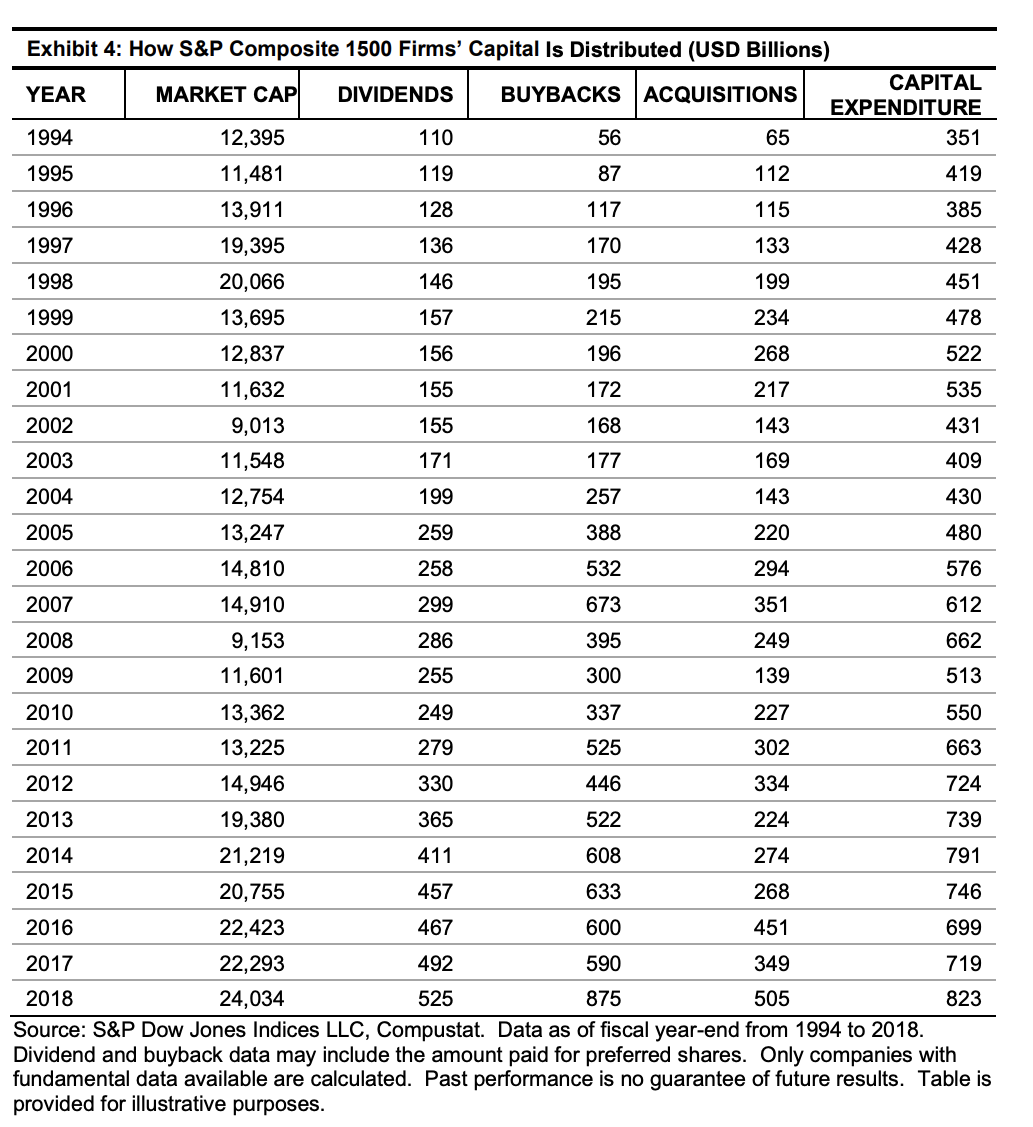

The Biden administration has passed a 1 percent tax on stock buybacks. A stock buyback is when a public company uses its own cash to buy back its own stock. Sometimes it is financially in the best interest of the company to actually borrow money to buy back stock.

- Excess cash on the balance sheet become takeover targets.

- A company will buy back stock when it doesn’t have a better use for the cash, like investing in property, manufacturing facilities, and new equipment.

- A company will buy back stock instead of issuing a dividend to shareholders. Dividends are heavily taxed in the current U.S. tax code (and is another reason why the Fair Tax is a great idea). Many institutional investors prefer buybacks to dividends purely because of tax reasons.

- If a company issues a dividend, shareholders expect them to continue paying the dividend. If they don’t pay the dividend, that market interprets it as poor performance. One way around that problem is declaring a “one-time special dividend,” but companies have shied away from that.

- Stock buybacks reduce costs for companies because buying back shares reduces the amount of shareholders. It reduces the number of claims on company capital.

- It is a way of returning capital to investors.

Stock buybacks are not a “bullish sign.” They aren’t “bearish” either. It’s simply a use of company cash. When C-level executives use their own money to buy their own company’s stock, it’s a bullish sign.

What should the government do? Make the choices tax equivalent between repurchases and dividends by not taxing them at all. More money would go off corporate balance sheets and into the hands of institutional investors or individual investors. They would be rewarded for assuming the risk of owning the stock. The 1 percent tax will increase distortions in the market and make the stock market less efficient, decreasing the returns to pension funds and individuals.