From wrong forecasts by the International Monetary Fund (IMF) and Wall Street, to wrong policies by the Federal Reserve and the Federal Government, wrong economic theory impacts everyone. Last year was a particularly bad one for the profession, as none of the mainstream forecasts on major events, from Brexit to Donald Trump’s election, and the effects of those events on markets and the economy, were correct. In fact, mainstream economics has been consistently getting it wrong since the Great Financial Crisis of 2008.

So why hasn’t the mainstream realized something is profoundly wrong with the models and theories it uses? Why do they marginalize alternative theories and theorists? Why are the people who have been getting it wrong still in charge?

If you worked for companies like General Motors or IBM and are now out of a job because they have outsourced it to Mexico, you can blame wrong economic theory for this.

The free-trade model advocated by elites from the IMF to Harvard has promised jobs for the developing world, while keeping the ones in the developed world. It hasn’t worked because the theory behind free trade, developed by 19th-century economist David Ricardo, is 200 years old and obsolete.

“Ricardo’s theory fails in a world of mobile factors [of capital and labor]. It only works if everyone plays by the rules. Free trade ... does not produce optimal outcomes because it is never free. It is a house built on the quicksand of assumptions that don’t reign in the real world and never will,” wrote analyst James Rickards in his book “The Road to Ruin: The Global Elites’ Secret Plan for the Next Financial Crisis.”

The elite economists at the IMF and the Fed have missed their growth forecasts for almost every major economy leading up to and following the financial crisis. Governments and companies making their plans based on the optimistic forecasts (these models never predict a crisis) are in for a rude awakening when they don’t materialize.

“They have models that extrapolate what is going on, they have to agree with one another, and they are covering their backs within their profession. That’s why they are always wrong,” said Woody Brock, president of consulting firm Strategic Economic Decisions.

Wall Street risk managers still use the same risk models that led to the subprime crisis. When the house of cards collapsed, it wiped out the savings of millions and plunged the country into the worst recession since the Great Depression. Because these same models are in use, another crisis is just around the corner.

“They are treating the financial sector as an outcome of economic action, not as a cause. But we know that the financial sector is a cause if something goes wrong,” said Steve Keen, a professor at London’s Kingston University and author of “Debunking Economics.”

After the financial crisis, fiscal stimulus and unprecedented money printing by central banks in the United States, Europe, and Japan promised us a solid recovery that has not materialized.

“The elite view is if the right Ph.D. economist is seated as Fed chair, with the dual mandate firmly in mind, and money supply as a lever to move the world, the global economy may be pushed to equilibrium and made to run like a fine Swiss watch,” wrote Rickards.

Wrong Models

Economists like to pack the world with all its idiosyncrasies into neat little mathematical models that are supposed to predict the future, an undertaking historically reserved for prophets and magicians, at least in the humanities. Actual science like physics gets a pass.

However, the models, no matter how sophisticated, follow the old rule of computer science first discovered in the 1950s: “garbage in, garbage out.”

The most important model in the toolkit of mainstream neoclassical economists is the Dynamic Stochastic General Equilibrium (DSGE) model. It states that supply matches demand, and the economy functions like clockwork until some not-to-be foreseen exogenous shock comes around that disrupts the model.

These models have been disproven in theory and in practice, and rely on assumptions that don’t apply in the real world. For example, the model expects the agents (us) to make decisions based on math and economic models and not based on whether we are bored at our jobs and feel like a bit of online shopping.

And yet, they are still being used by the world’s central banks as well as institutions like the IMF and world governments to craft monetary and fiscal policy.

“The herd [of monetary elites] agrees that markets are efficient, albeit with imperfections. They agree that supply and demand produce local equilibria, and the sum of these equilibria is a general equilibrium. When equilibrium is perturbed, it can be restored through policy,” wrote Rickards, who also notes that equilibrium is “a facade that masks unstable complex dynamics.”

The models’ shortcomings are so obvious, however, that the chief economist of the World Bank, Paul Romer, has broken ranks with the economic elite and last year published a scathing critique of macroeconomists in general and the equilibrium models in particular called “The Trouble With Macroeconomics.”

His verdict: “Macro models now use incredible identifying assumptions to reach bewildering conclusions. ... Macroeconomists got comfortable with the idea that fluctuations in macroeconomic aggregates are caused by imaginary shocks, instead of actions that people take. ... Once macroeconomists concluded that it was reasonable to invoke imaginary forcing variables, they added more.”

It is the DSGE model that led former Fed chairman Ben Bernanke to declare the following about the equilibrium interest rate on his blog for the Brookings Institution in 2015:

“If the Fed wants to see full employment of capital and labor resources (which, of course, it does), then its task amounts to using its influence over market interest rates to push those rates toward levels consistent with the equilibrium rate, or—more realistically—its best estimate of the equilibrium rate, which is not directly observable.”

So the rate the Fed wants to achieve, one that will supposedly bring about the best use of capital and labor (remember the assumption behind equilibrium here), is not directly observable, so the Fed is left guessing.

Small wonder it can never predict a crisis and instead often causes one by leaving rates too low for too long and then later raising them at the most inopportune moment. And no wonder the economy still hasn’t taken off, despite zero interest rates for close to a decade, which brings us to another problem.

Crises Don’t Fit

“They ignore money and credit, probably the most important determinants of where the economy goes,” said Keen.

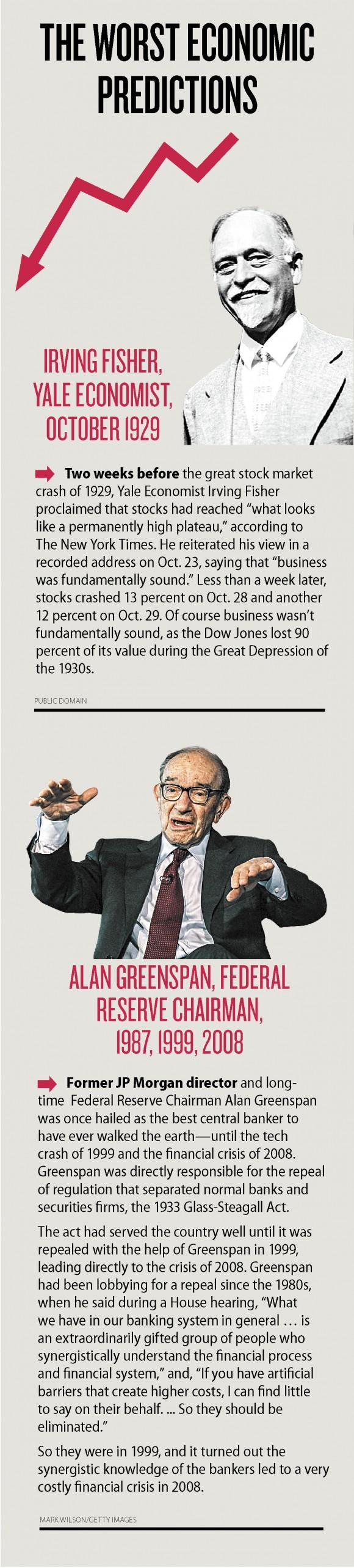

For instance, Bernanke told Congress in March 2007 that “the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained.” It wasn’t.

“They only extrapolate the current trends and that only matters if there is no change in the things they are ignoring. So if there is a change in money, credit, and debt, then they are going to be completely wrong, and that’s what happened in 2008,” said Keen.

“What matters in the model is not money but the imaginary forces,” wrote Romer.

Mainstream economists usually use the excuse that nobody saw a particular event coming, like the crisis in 2008, which is only true if the somebodies are mainstream economists and everybody else is a nobody.

Keen did predict the crisis of 2008 using post-Keynesian models, which include private debt, and so did hedge fund legend Ray Dalio of Bridgewater Associates, who also built models around private debt. There are scores of others who did the same and profited from it. None of them follow the mainstream.

Rickards predicted the 2008 crisis using complexity theory borrowed from physics, which has nothing to do with DSGE models and the so-called “normal” occurrence or distribution of risk.

“Crises emerge because regulators don’t comprehend the statistical properties of the systems they regulate,” Rickards wrote.

“There are models that do a good job identifying bubbles using complexity theory, causal inference, and behavioral economics, although the exact timing of collapse remains difficult to predict,” he wrote.

It is mostly physicists who use complexity theory, but it can also be applied to capital markets. Unlike equilibrium models, complex systems allow for extreme events to occur rather frequently. They also have dynamic feedback loops so agents can learn from their past actions and from other agents.

Brock also believes economists at the Fed and elsewhere rely too much on historical data to make predictions for the future.

“They are trained that history is everything,” Brock said. Enough data will identify economic relationships.

“That’s fine until structural changes occur and the previous relationship breaks down,” he said. Structural changes, like too much debt in the system, brought the economy to its knees in 2008 and now prevent us from realizing our maximum growth potential. “Structural changes mean historical samples won’t be good. You must use your subjective judgment so you know what is different,” he added.

In a nutshell, “capital markets were condemned to a succession of calamities while academics-turned-central bankers waited decades for more data to convince them of their failures,” wrote Rickards.

With the exception of Romer, however, mainstream economists aren’t convinced that there is something at all wrong with their way of doing things.

Living in the Ivory Tower

There are several reasons why economists cannot or do not want to see the evident flaws in their models and their way of thinking.

According to Brock, it’s the fact that subjective analysis of structural changes would expose the economists to being wrong, a risk they cannot live with.

“Most people who go for those jobs are risk-averse in the extreme. Subjective probabilities can’t be proven true. They do things where they can always back up positions with data. The fact that the data is irrelevant doesn’t matter,” he said.

Keen thinks this risk aversion combines with a desire to hold on to power. “If the mainstream economists admit that they are wrong and the post-Keynesians are right, they would have to abandon their posts, resign, and let us take over. That’s the last thing anybody will do,” he said.

But given their dismal performance, how can these people stick around for so long? Keen said the problem starts in academia and then seamlessly flows through to the centers of power.

“In economics, all the non-orthodox people can’t get jobs in the main universities because we don’t push the mainstream paradigm,” he said, adding, “We don’t get the exposure, and we are not even part of this debate.”

It is this lack of creative debate that has robbed academics and policymakers of better tools to interpret and handle economic problems. Mainstream economists live in their bubble and have given up serving science. They would rather serve their leaders, according to Romer.

“Because guidance from authority can align the efforts of many researchers, conformity to the facts is no longer needed as a coordinating device. As a result, if facts disconfirm the officially sanctioned theoretical vision, they are subordinated,” he wrote.

“Eventually, evidence stops being relevant. Progress in the field is judged by the purity of its mathematical theories, as determined by the authorities.”

Romer also states that while some mainstream economists have been angered by his critique, others by and large agree but do not dare to speak out in public.

What Romer describes as a “general failure mode of science” is not new. When Nicolaus Copernicus told his fellow scientists in the 16th century that the earth revolved around the sun rather than the other way around, he was in for some trouble.

Both Keen and Romer think of science as a belief system. Humans find it difficult to give up widely held beliefs, even if they are proven wrong.

“Humanity shares belief systems. If you have a belief system, you live in a world that promotes that belief system, and you will be critical of opposing belief systems. The initial response of any discipline is to reinforce its current belief system,” said Keen.

“It starts by distinguishing ’research‘ fields from ’belief' fields. In research fields such as math, science, and technology, the pursuit of truth is the coordinating device. In belief fields such as religion and political action, authorities coordinate the efforts of group members,” wrote Romer. He thinks macroeconomics has morphed into a belief field.

What Can Be Done?

Economics is called the dismal science, but it is not useless. There are economists and models that can explain complex human behavior, leading to better policy decisions. Mainstream scholars just have to admit their equilibrium-centric view of the economic system is wrong.

“In the 20th century, we developed the technology to send people to the moon. It involves non-equilibrium systems. If you assume an equilibrium in that process, you have dead astronauts,” said Keen.

He said economists should borrow from these branches of science to model the economy as a non-equilibrium system, and of course include money and debt.

Brock said economists have to allow themselves to be wrong from time to time to grasp structural changes.

“You have to be trained in game theory and political theory to understand” these changes, he says. Neither provides a neat outcome with 100 percent certainty but rather different probabilities. This is somewhat ironic, as the mainstream now claims its models are always right and yet they are wrong at the crucial times.

Rickards thinks capital markets should be analyzed as a complex system with a non-normal distribution of risk.

However, all these changes would only be possible if economists started to adhere to scientific methods again.

“By rejecting any reliance on central authority, the members of a research field can coordinate their independent efforts only by maintaining an unwavering commitment to the pursuit of truth [via the consensus] that emerges from many independent assessments ... assessments that are made by people who ... accept their own fallibility, and relish the chance to subvert any claim of authority,” wrote Romer.

Safe Bets

In the here and now, there are some policies most non-mainstream economists consider safe bets. One of them is the reinstatement of the 1933 Depression-era Glass-Steagall Act. The act separated consumer banking from the securities business and served the country well until its repeal in 1999 by President Bill Clinton.

“Glass-Steagall worked for exactly the reason complexity theory suggests. By breaking the banking system into two parts, Glass-Steagall made each part stronger by shrinking systemic scale, diminishing dense connections, and truncating channels through which failure of one institution jeopardizes [everything],” wrote Rickards.

In fact, the repeal was a classic case of trying to make reality fit economic models rather than the other way around. “Economists were for the repeal because it fits their model on how the economy should operate,” said Keen.

Another safely established danger signal is private debt. Keen says that once private debt passes 150 percent of GDP, a financial crisis is almost inevitable. “There are danger zones you don’t want to enter,” he said.

Keen and Rickards both argue for strengthening the role of labor in the economy, including enacting some protectionist trade measures and giving workers more influence at their companies.

Brock said infrastructure spending, lower taxes, and deregulation are the right fiscal policy levers. “It’s the incentives that are most important to determine growth,” he said.

Neither of the cited economists and analysts believes, however, that humans could ever achieve perfection with modeling or predictions. It’s rather more important to let go of a false sense of pride and learn from past mistakes.

“Science and the spirit of the enlightenment are the most important human accomplishments,” wrote Romer. “They matter more than the feelings of any of us.”