According to the most recent CPI numbers released from the Bureau of Labor Statistics, CNBC reported on July 13th: “Energy prices surged 7.5 percent on the month and were up 41.6 percent on a 12-month basis. The food index increased 1 percent, while shelter costs, which make up about one-third of the CPI, rose 0.6 percent for the month and were up 5.6 percent annually. This was the sixth straight month that food at home rose at least 1 percent.”

CNBC continued: “After the report, traders priced in virtual certainty that the Fed will increase its benchmark rate by three-quarters of a percentage point at the July and September meetings, with a one-third chance of a full-point increase at this month’s gathering.”

As the country continues to see the worst inflation in 40 years, these new numbers will likely trigger an immediate response and subsequent rate hike by the Federal Reserve.

Right now bonds are slumping because bond traders are betting on a 1.00 Fed hike, but more confusion is ahead. Futures markets indicate a rate cut in 2023 or 2024. Yes, that is correct; the Federal Reserve is raising rates but they also intend to cut rates as soon as next year.

As Jacob Sonenshine at Barron’s reported earlier this year: “The fed funds futures market is also signaling that the central bank isn’t too far from lowering borrowing costs again. Prices in the futures market indicate that the Fed will cut rates in late 2024, sending the fed-funds rate down to 2.25 percent, the equivalent of two quarter-point cuts from the expected peak.”

Nomura, a Japanese bank, expects much of the same. The bank’s economists are in anticipation of Federal Reserve rate hikes peaking at 3.75 percent in early 2023; then the economists are forecasting rate cuts in September 2023.

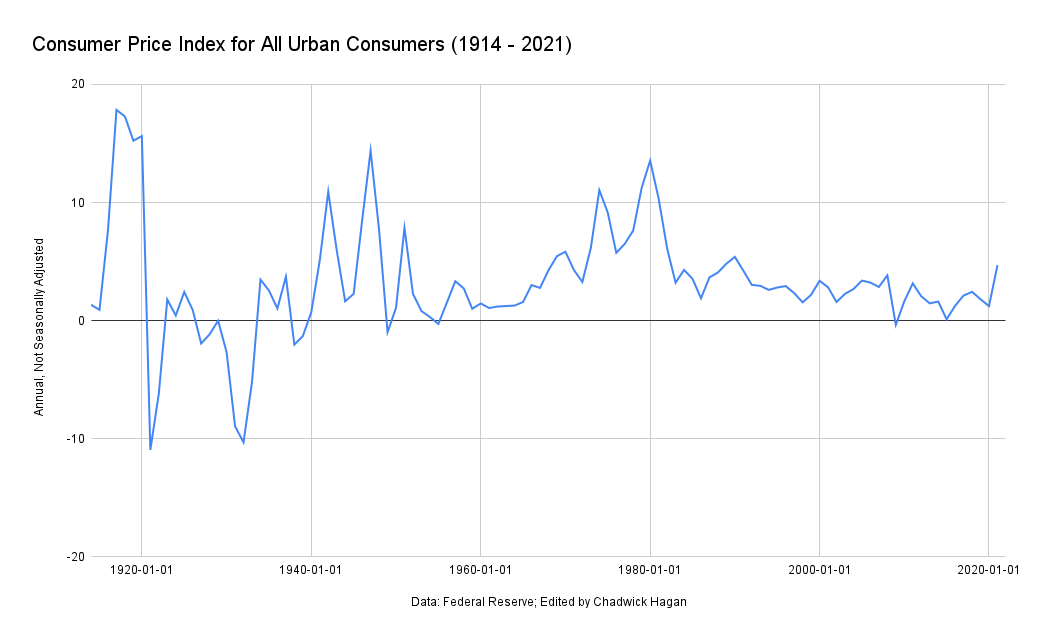

But what about a return to normal? As you can see from the charts I’ve included, some prices have dropped recently but that is after prices topped out at multi-year highs. I have also included a chart showing annual CPI prices since 1914.

Adding insult to injury, in a speech to AFL-CIO union members in Philadelphia in June, Biden said: “I don’t want to hear any more of these lies about reckless spending. We’re changing people’s lives!” If you believe in sound fiscal policy, then words like that—coming from the U.S. President—are nearly impossible to digest.

Adding insult to injury, in a speech to AFL-CIO union members in Philadelphia in June, Biden said: “I don’t want to hear any more of these lies about reckless spending. We’re changing people’s lives!” If you believe in sound fiscal policy, then words like that—coming from the U.S. President—are nearly impossible to digest.Recently, economist Steve Hanke, whose predictions have been on the mark, chimed in on Twitter, saying: “The markets are pricing in 3%/yr U.S. inflation over the next 2 yrs. SPOILER ALERT: The mkts are wrong. Inflation will be between 6-7%/yr thru 2023. How do I know? The Quantity Theory of Money. M2 growth fuels inflation, & has grown by 41% since Feb 2020.”

Looking at the quantity theory of money (QTM) that Professor Hanke referenced in his tweet, we can expect the quantity of money available—called the money supply—to grow at the same rate as prices. Basically, QTM is a theory that states the money supply has a direct relationship with prices. Print more money and you have higher prices. To dig a bit deeper, according to the St. Louis Federal Reserve: “The quantity theory of money asserts that aggregate prices and total money supply are related. A central implication of the QTM is that a given change in the rate of money growth induces an equal change in the inflation rate.”

As Milton Friedman said: “Inflation is always and everywhere a monetary phenomenon, in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.”

National Economic Council Director Brian Deese recently said that we can “address high inflation by passing more spending bills.” The real truth is a very different story. We have already spent more than we can afford. As for 2021 numbers—in March 2021, total COVID spend hit $5.2 trillion. World War II cost the equivalent of $4.5 trillion (in 2021 dollars, give or take a few billion). The 2021 year-end total was around $13 trillion. I’m not even including money spent in 2022. Printing more money would cause further destruction.

As soon as we control government spending, then we will begin to see an end to this inflationary chaos. There is a chance that inflation will be under control by Q3 2023, but there is also the risk that inflation lingers until sometime in 2024 or beyond. Regardless, this will be one of the only things on voters’ minds while in the voting booth.

I’ll close with an excerpt from Richard W. Rahn, the chair of the Institute for Global Economic Growth: “The good news is that inflation will end. The bad news is that, given who is making economic policy, it is more likely to end badly than benignly. The proper way to end inflation is to reduce the rate of government spending so that it is increasing at a slower rate than economic growth.”