Many investors are noticing that technology stocks are going down much more than the general market recently, and we’ve been getting a number of questions regarding the reason. This has to do with the expected increase in interest rates, which has been a frequent topic of this column. This phenomenon is well-known to market professionals and is the result of something called duration. Duration is simply a fancy word for how long it takes to get paid on an investment.

Let’s take a simple debt as an example. If a friend owes you $1,000 and promises to pay you back tomorrow, you don’t have to spend a lot of time worrying about interest rates. Now, let’s say you’ll be paid back in a year. That increases the duration (or length of time) involved and depending on the interest rate, you might care a bit more about the value of that $1,000 a year from now. If we take the example out of another order of magnitude, and the promise is to pay you back the $1,000 in ten years, you definitely care about the rate of interest. Simply stated: The longer the length of time involved (duration), the more you care about interest rates.

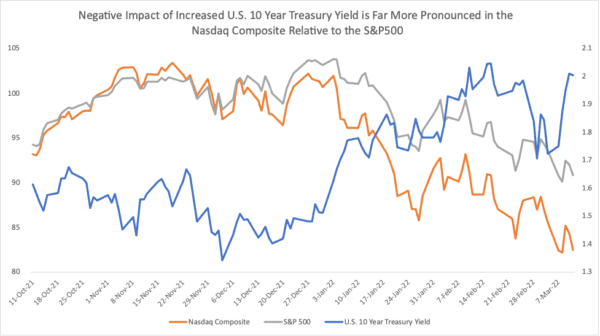

We’ve seen that relationship in recent market returns. The 10-year U.S. treasury bill made a recent low on Dec. 3, 2021 (blue line in the graph below). Since then, concerns about inflation have pushed the U.S. Federal Reserve to talk about starting to raise interest rates. The current 0 percent Fed Funds rate will start to go up later this month. If we calculate from the closing prices on Dec. 2, 2021, the Dow Industrial Index is down 4.9 percent, the S&P 500 which has a higher weighting of technology stocks is down 9.1 percent (gray line in the graph below), and the NASDAQ 100 which is focused primarily on technology stocks is down 17.5 percent (orange line in the graph below). So, clearly, this relationship between interest rates, duration, and stock valuations is holding in recent months.

In general, many technology companies focus on revenue growth and market share first. The strategy for these companies is once they gain critical mass or leading market share, they can shift the business model later to focus on profits and free cash flow. Amazon is one of the best examples of this. The company was famous for its patient shareholders who waited almost two decades for the company to turn a profit. The stock traded at high multiples because shareholders understood that Amazon’s revenue growth and market share would eventually turn into huge amounts of net income and free cash flow. It was the perfect example of a long-duration stock; one where investors understood that the greatest amount of value was far in the future.

Contrast this with Dow component 3M Company. This consumer products firm is expected to grow revenue 3-4 percent in each of the next two years and trades at a modest 12.9 times earnings. Compared with Amazon, 3M is a shorter duration investment with more of its value tied to current earnings. While each company has individual factors that affect its business outlook and stock price, as we saw above, the general market indexes show a more consistent relationship between duration and interest rates.

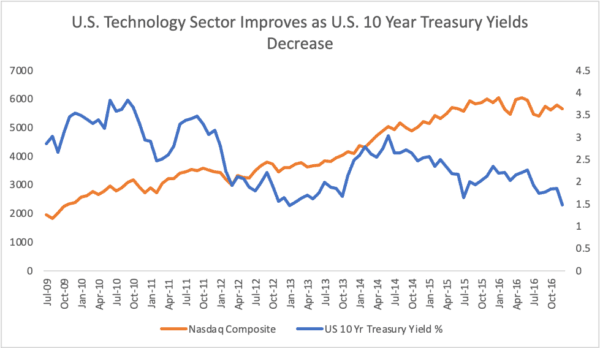

It’s worth illustrating that the reverse effect is also common. Declining interest rates tend to be a positive for technology and growth stock valuations:

Basically, the greater the growth component of the stock, the more of the value resides further in the future. The further in the future the value of the stock is, the greater the duration. And the longer the duration, the more sensitive the stock will be to interest rates. As always, an individual security could announce financial results, a buyback, a takeover, or a new contract that becomes more important than the effect of interest rates. However, the reason you’re seeing a recent contraction in growth stocks in general and technology stocks, in particular, is due to rising interest rates.

We often like owning high-growth stocks over long periods of time, and there’s nothing wrong with owning them in a rising-rate environment. However, if you’re going to do that, you might consider different ways of hedging that duration risk using either options or shorting one or more of the market indexes against your technology equity exposure. These can be both profitable and risky strategies so as always, it might be a good idea to seek out the counsel of a trusted professional if your chosen investment strategy gets more complicated than you’re comfortable handling yourself.