This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

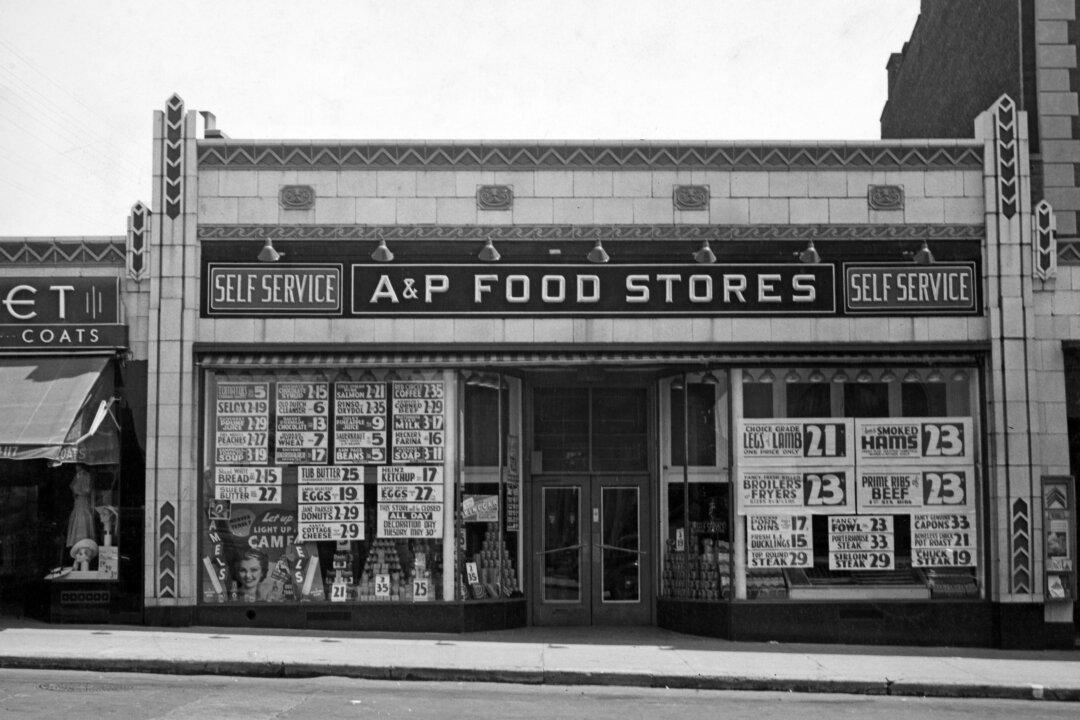

Federal Reserve Chairman Jerome Powell testifies during a Senate Banking Committee hearing at Capitol Hill in Washington on March 3, 2022. Tom Williams/Pool via AP

In 1984, Nobel economics laureate Milton Friedman said he would replace the Federal Reserve Board with a computer, a machine programmed to increase the money supply by no more than about 2 percent per year. The esteemed co-author of the landmark “A Monetary History of the United States, 1867–1960” knew that a series of interconnected circuits and silicon chips would be insensitive to pressure from Washington politicians. But recent days and weeks have shown that most of the flesh-and-blood members of the Federal Open Market Committee (FOMC) have less guts than Friedman’s imagined robotic monetary regulator.

On March 16, the Federal Reserve announced a tepid 25-basis-point increase in the federal funds rate, the short-term interest rate at which banks make overnight loans to one another. That means that the fed funds rate is now above the zero-to-near-zero range for the first time since 2018. As a remedy for inflation raging at a level unseen in 40 years, this is like an eyedropper substituting for a fire extinguisher.

One of the greatly brandished points of pride of the U.S. economy and financial system is the fact that we have long enjoyed the benefits of an independent central bank. Although the proposition has recently been challenged by some interesting unconventional academic research in Europe, there is a strong, long-held consensus that countries with central banks that are exempt, under law and in practice, from direct political interference have experienced significantly lower inflation.

Accepting this notion, one would expect, in the current environment of the worst inflation in the memory of most Americans, something like the following scenario: a Federal Reserve chairman announcing to the public that major rises in interest rates are about to begin, and the equity markets and borrowers should prepare for some sour medicine; following that, the president of the United States, various members of Congress and other elected leaders, as well as labor union bosses, express alarm and issue threats against these unelected bean counters for daring to “take away the punch bowl” from the economy.

Yet what we found was New York Federal Reserve Bank president John Williams last month saying he didn’t “see any compelling argument to take a big step at the beginning” of the Fed’s new policy of rate hikes. We also have Federal Reserve Chairman Jerome Powell, still unconfirmed in his renomination by President Joe Biden, talking happy talk that “the economy is very strong and well positioned to withstand tighter monetary policy,” that it won’t just “withstand but certainly flourish, as well,” despite the coming rate hikes, and that “the probability of a recession within the next year is not particularly elevated.”

This is wishful thinking at a bad time by someone who should know better. The yield curve, which differentiates longer and shorter-term Treasury securities and is a key indicator of economic weakness, is flattening fast. Clinton Treasury secretary and Obama senior economic adviser Larry Summers just warned of much higher inflation next year—three percentage points, at variance to the 4.3 percent inflation rate the Fed officially expects at the end of this year—and the risk of a consequent “wage-price spiral.”

Quill Intelligence founder and CEO Danielle DiMartino Booth, who for many years advised the Federal Reserve Bank of Dallas, including during the 2008 financial crisis, warned on “Fox Business” on March 17 that Powell’s dovish course means “we lose complete control of inflation, at least in the short term.”

Toward the end of his questioning from reporters on March 17, Powell remarked that “no one wants to have to really put restrictive monetary policy on in order to get inflation back down.” Clearly, this is no Paul Volcker, who decided that killing the inflation beast meant boosting the fed funds rate to above the inflation rate—20 percent in June 1981—as opposed to characterizing rising a few basis points above zero for the first time in years as tight policy. Powell’s Fed is now on track to execute six rate hikes of 25 basis points each to arrive at about 1.9 percent by the end of the year, then four more such increases next year.

James Bullard, president of the St. Louis Fed, may be the lone insider with his feet on the ground, calling for an increase of 50 basis points at the March, May, or June scheduled FOMC meeting. He believes that such “forthright and transparent actions designed to keep inflation under control will give the U.S. economy the best possible chance at a long and durable expansion.”

But why should we expect the Fed to be serious when, like so much of the rest of government, it’s turning woke faster than gas prices are rising?

Sen. Joe Manchin of West Virginia, very nearly the only Democrat in Congress willing to dissent from some of his party’s environmentalist fanaticism, days ago killed Biden’s nomination for the Fed’s Vice Chair for Supervision, green activist Sarah Bloom Raskin, who would likely have encouraged private lenders to disfavor the oil and gas industry at a time of severe and ongoing rising fossil fuel prices.

Equally disturbing at least, Nova Southeastern University finance scholar Emre Kuvvet, in an Independent Review article previewed in The Wall Street Journal earlier this month, revealed that nearly all of the Federal Reserve system’s 780 economists are affiliated with the Democratic Party. And as inflation rages out of control, they have somehow found the time to focus “on issues such as climate change, race and sex discrimination, and economic inequality.” Among the Fed’s most senior economists, who are in leadership positions, “the Democrat-to-Republican ratio is 22.25 to 1,” Kuvvet discovered.

With such staff around him, it is less shocking to find Chairman Powell saying things that may leave voters less angry at the party in power on election day this November. But it goes beyond rhetoric.

The Fed’s ability to inflate the money supply is unlimited, and it has been accommodating the government’s big-spending ways. No one can excuse or rationalize the Fed going on a bond spending spree and maintaining a near-zero fed funds rate while inflation raged at 7 percent and the economy boomed back from the COVID lockdowns.

Now that we know for sure Powell’s timid strategy, Americans will have to look elsewhere to fight inflation–like demanding the liberation of the country’s energy companies, allowing them to drill for oil and gas to the maximum extent, a move that would bring gasoline prices down dramatically and produce a massive ripple effect to dampen overall inflation.

Of course, the Biden administration, at war with fossil fuels, will never do any such thing. So all Americans can do is contemplate what point there is to having an independent Federal Reserve when those appointed to run it have neither the brains nor the spine to exercise their independence.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times.