Netflix’s announcement this week that it had lost 200,000 subscribers should sound a warning on the real costs to the economy of continuing high inflation. I suspect Netflix is just a canary in a coal mine: a warning of bad times for us all, not just binge-watching couch potatoes.

Consumer spending is almost always the largest single component of GDP. In 2021, the category of “Food service and accommodations” within consumer spending—the restaurant meals and vacations that Americans say they will cut back—accounted for more than 1 percentage point of the average 5.5 percent of average quarterly 2021 GDP.

While spending in the food service and accommodation area of GDP is the most likely to be cut, based on the survey, it’s important to note that inflation will affect spending in all categories of spending, including consumer staples such as housing, clothing, and transportation.

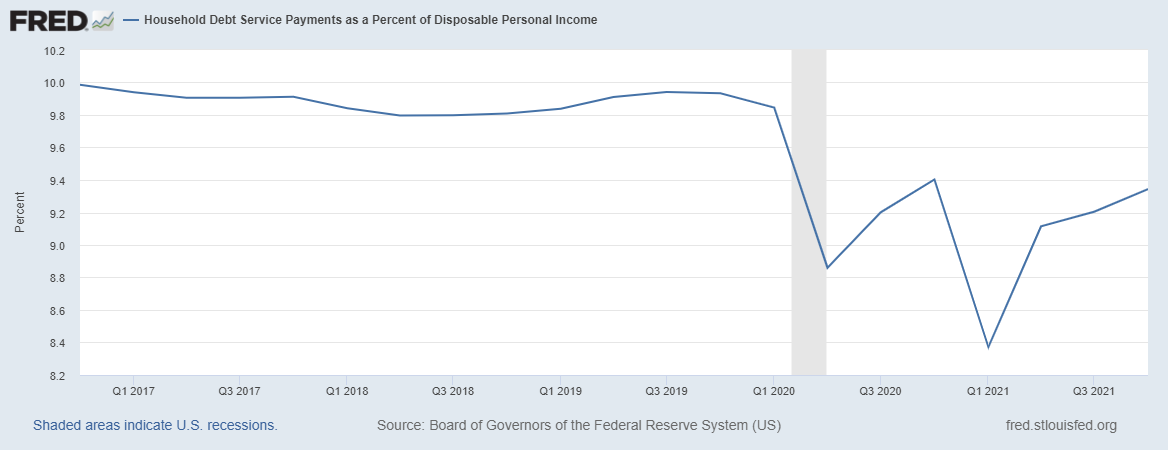

At the same time, the rising inflation has caused Federal Reserve observers to predict the Fed will raise the federal funds rate, the rate at which banks lend to each other overnight, to as much as 2.25 percent, to further impinge spending. Debt service as a percent of disposable income is already increasing and, with higher interest rates, will increase even more, choking off even more of the spending on goods, services, and investments that comprise GDP.

With Fed rate hikes in the offing, prospective home purchasers will be able to purchase even less and, with that, they will need less carpeting, less furniture, and less “stuff” to furnish their new home. If they try to upsize and pay more mortgage carrying charges than they can comfortably afford, they’ll have less disposable income after paying their mortgage to spend on other things.

Economists in the 1970s coined a term for this phenomenon, where inflation leads to a slowing or stalled economy: They called it “stagflation,” a portmanteau of the words “stagnation” and “inflation.”

But I fear now that “stagflation” may not be the right moniker for what lies ahead. Just as the bell bottoms, platform shoes, and polyester leisure suits of the 1970s wouldn’t be fashionable clothes for today, neither is stagflation suitable for our coming economic woes.

That’s because, after nearly 14 years of the Fed’s near-zero interest rate policies, there will be another knock-on effect to further reduce consumer spending: the Wealth Effect.

Simply put, the Wealth Effect assumes that people who have more wealth tend to spend more. But the opposite is also true: As people see their wealth erode, they tend to watch their spending more carefully and cut back on discretionary spending.

When consumers look at their 401(k) plan statements or their stock portfolios in the coming months, they will likely see an erosion of their wealth that will tend to discourage discretionary spending. Vacation plans may be cut back or canceled altogether. That new Lexus will look less appealing. Dinner out is more likely to be a Denny’s than that fashionable bistro everyone is raving about.

And all those reductions in spending will tend to further slow GDP and drive stock prices further lower.

So, I propose we update the 1970s “stagflation” vernacular to a more descriptive new phrase; one that adds an adjective that takes account of the decline in spending in GDP that will occur as the Fed raises rates and stifles the values of stocks. I say add an adjective to the portmanteau and call this new era, “Bear market stagflation.”

Whaddya think?