Los Angeles County, Orange County, San Diego, and “the Inland Empire” have many similarities in their economies but also some very important local differences.

Anaheim, in Orange County, is highly dependent on families and convention-goers coming to Disneyland and the Convention Center, while Irvine is the center of the county’s medical device community. Orange County has five times the number of people working in the medical device industry than the U.S. average would dictate.

Meanwhile, in L.A. County, the economies and real estate markets of San Pedro and Long Beach are heavily tied to the United States’ most important trade terminal, while other parts are heavily tied to film and TV show production. Still other parts of Los Angeles and much of the Inland Empire (Riverside, San Bernardino, Fontana, and Ontario) are tied to warehousing and distribution.

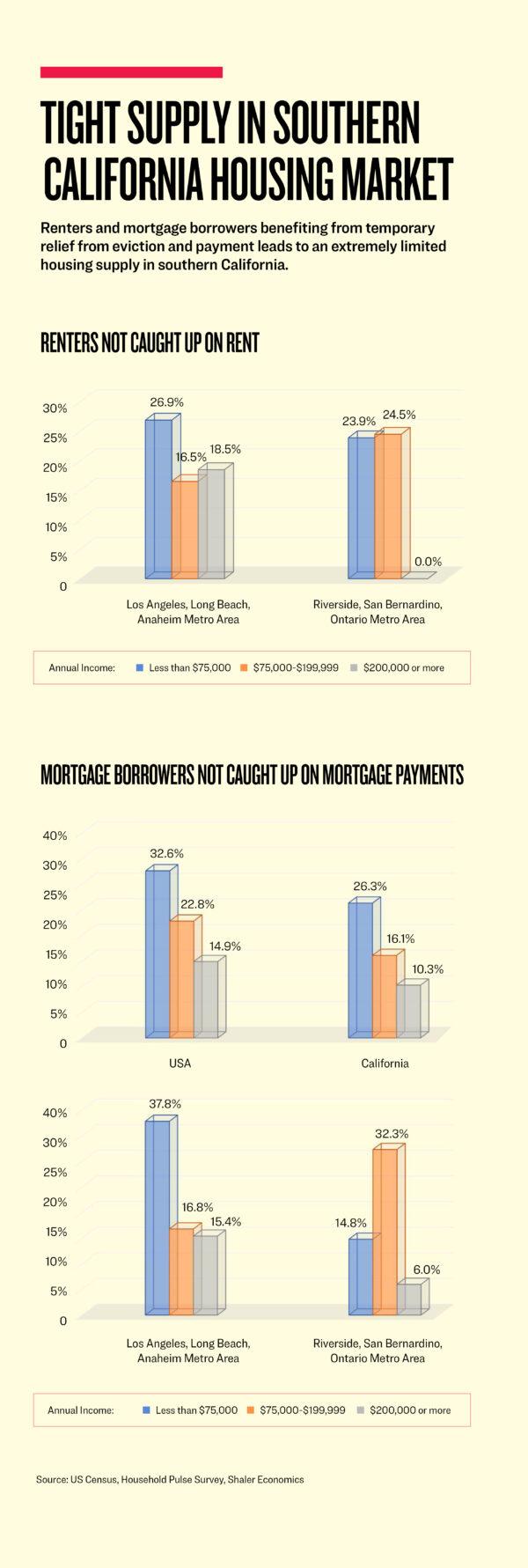

Data made available this past week from the Census Bureau shows that a very high portion of mortgage borrowers and renters aren’t current with their mortgages or rent payments. However, many jurisdictions aren’t allowing evictions and many lenders are providing deferment programs to keep homeowners in their homes.

All of these nuances are coming together to push up property values quickly, in municipalities where industry is more stable during the pandemic (i.e., medical devices in Orange County and warehousing in the Inland Empire). In some places, real estate prices are going up even more quickly because they are popular among people relocating to from higher-density areas or seeking places that can accommodate families working, studying, and entertaining themselves in the safety of their own homes.

We learned last week that property values are reaching heights last seen during the price bubble of 2006. Indeed, according to CoreLogic’s Southern California Resale Activity Report, the August median price for transacted single family homes across L.A., Orange, Riverside, and San Diego counties were up 13.5 percent to 15.2 percent from a year ago, while the price of San Bernardino County single-family homes rose 9.3 percent from a year ago.

Of course, this could all change, depending on the course of the public health crisis, the election cycle, whether people keep moving now that their kids are getting back to in-person instruction, and also how the situations resolve for the people who lag on their rent or mortgage payments.

But, for now, property prices in Southern California are at the highest level in a generation.