This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

The Volcker recession of 1981–82 crushed inflation out of the economy, and presented economists with a new challenge: Rather than high and rising inflation, their new dilemma was low and falling inflation.

This was a dilemma they were happy to have, and in fact, they took credit for it. They eventually labeled this period of not merely low inflation, but also, for a time, falling levels of unemployment—see bottom chart in Figure 1—as the “Great Moderation.” Volcker’s successor from 2006 till 2014, Ben Bernanke, waxed lyrical in October 2004, saying that:

The sources of the Great Moderation remain somewhat controversial, but … there is evidence for the view that improved control of inflation has contributed in important measure to this welcome change in the economy. Paul Volcker and his colleagues on the Federal Open Market Committee deserve enormous credit both for recognizing the crucial importance of achieving low and stable inflation and for the courage and perseverance with which they tackled America’s critical inflation problem.

Then the Global Financial Crisis hit in August 2007, and that comfortable “pat on the back” explanation for low inflation and unemployment went out the window—or it should have.

Inflation of 5 percent in 2006 collapsed into deflation of 2 percent in 2007, unemployment exploded from 5 percent to 10 percent, and the Central Bank inflation problem turned weird. Having spent decades trying to get inflation down to their target of 2 percent, after the Global Financial Crisis they struggled to get it up to that target.

Until, that is, inflation blasted right past 2 percent in 2021, and reached over 8 percent in June. Faced with this unexpected shock, economists are wheeling out the tools that they think caused inflation to fall back in the 1980s: a sharp rise in interest rates to tame “inflationary expectations.” Having set its target interest rate at 0.25 percent since March 2020, it started hiking the rate in March 2022. It is currently at 1.75 percent, and most economists are expecting further hikes to 3.5 percent by the end of 2022.

The mainstream economist Paul Krugman believes that the job of taming “inflationary expectations” is already done. He notes that the bond markets are forecasting inflation at 3.6 percent in 2023—well below the current 8.5 percent—and declares that the message we’re getting from the markets “is, don’t panic. Inflation is not, in fact, out of control, although the pain many consumers are feeling right now is,” he wrote for the NY Times.

I wish I could agree. But instead, I think inflation is “out of control,” and the cause has nothing to do with the chimeras of “inflationary expectations,” or other mainstream economics fantasies like the Non-Accelerating Inflation Rate of Unemployment (NAIRU), which the columnist Michael Pascoe satirized well in a recent column.

Data: Federal Reserve Economic Data [FRED], St. Louis Fed [CPIAUCSL & UNRATE]; Chart: Steven Keen

Instead, we can use a much more realistic approach by the Polish engineer-turned-economist Michal Kalecki, when he divided the factors that cause inflation into three categories:

The markup that manufacturers put on their input costs, in order to make a profit;

The input costs they have to pay; Kalecki focused on wages, but this can also include energy inputs, minerals, etc.—basically, anything not made in the manufacturing sector; and

The productivity of those inputs: basically, the ratio between the output in terms of goods, and the inputs in terms of units—workers, tonnes of oil, etc.

Sticking just with workers, that identifies three factors that can lead to rising prices: rising markups, rising wages, or falling productivity.

We can pretty rapidly rule out rising wages as a cause of today’s unemployment: even with the tightest labor market in decades, wage growth is lagging well behind the rate of inflation.

The first factor—rising markups—is a potential factor today. Markups are fundamentally restrained by the degree of competition that manufacturers feel in the aggregate in their markets. When demand is buoyant, as it is now, markups are likely to rise. But that buoyancy is largely due to the enormous and necessary deficits that countries ran at the beginning of the pandemic. If governments reverse direction now to focus on “budget repair”—another Neoclassical chimera—then that buoyancy will disappear, and markups could fall.

But the key factor that makes inflation today totally different from inflation in the past is the last one: falling productivity. Right now, this is being driven by three primary factors: COVID, the Russia–Ukraine War, and declining productivity from fossil fuels and mining.

COVID-induced absences by critical staff are hampering production in the world’s factories, and lengthening the time it takes to ship goods from the world’s factory nations to its consumer nations (a division that has been created by the globalization of production over the last four decades). On top of the damage done to manufacturing, a COVID-affected workforce in the West is hitting transportation and services there.

Hypothetically, COVID could be a transient factor; there could be some miracle cure that removes it from the world, making a return to a pre-COVID environment possible. The same could happen with the Russia–Ukraine war: Russia is the world’s No. 1 wheat exporter, and Ukraine is No. 5. The war has drastically reduced their exports and is driving food costs higher. But, if it ends, then perhaps their grain exports could resume.

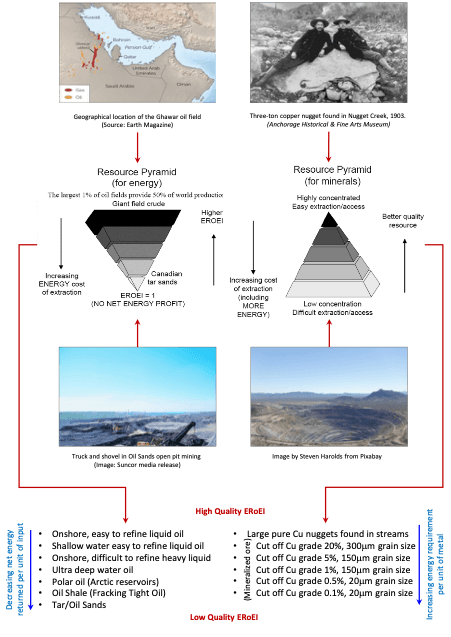

But no such fantasy is possible for the next factor, which is brilliantly captured in the graphic shown in Figure 2, from Australian mining engineer Simon Michaux. An Associate Professor of Geometallurgy at the Geological Survey of Finland, he has a doctorate in mining. In the past, a tiny amount of energy was needed to mine oil and coal: the “energy return on energy invested” was huge. Equally, mineral deposits were rich, and easily processed using cheap energy.

Graphic created by Simon Michaux which illustrates the declining quality of energy and mineral resources over time. Reproduced with the permission of Michaux (original is Figure 59 in ”The Mining of Minerals and the Limits to Growth”).

We have drastically improved the efficiency with which we mine energy and process minerals today, but the physical constraints of much more difficult to mine energy, and much lower quality minerals, can’t be eliminated by ever-rising productivity. These two factors also multiply together: the energy is more expensive, and more of it is needed to process lower-quality ores into final goods. One problem amplifies the other.

Since this is also happening in the context of dangerous global warming, and fossil fuels still provide over 80 percent of our energy inputs, there is no possibility of replacing fossil fuels with renewables or nuclear power in time to address these cost pressures.

The likely prospect, therefore, is rising prices—not because of wage demands or excessive markups, but because of a sheer increase in the cost of turning raw materials into finished goods.

The Neoclassical “cure” for this disease—rising interest rates, and cutbacks on government spending—are as effective as 18th-century medicine was against cancer. They will probably cause a recession, which may reduce markups and thus some inflation. But with real wages falling, rising unemployment on top of falling real wages could break the West’s already brittle social compact.

Inflation is, therefore, likely to be a permanent feature of society. The question is not how to eliminate it, but how to avoid it causing social breakdown.

Professor Keen is a distinguished research fellow at University College London, an author, and has received the Revere Award from the Real World Economics Review. His main research interests are developing the complex systems approach to macroeconomics and the economics of climate change. He has entered politics as the lead candidate in New South Wales for the new Australian political party The New Liberals.

His main research interests are developing the complex systems approach to macroeconomics, and the economics of climate change.

In an unusual step for a retired academic, he has entered politics as the lead candidate in New South Wales for the new Australian political party The New Liberals.

![(Data: Federal Reserve Economic Data [FRED], St. Louis Fed [<a href="https://fred.stlouisfed.org/series/CPIAUCSL">CPIAUCSL</a> & <a href="https://fred.stlouisfed.org/series/UNRATE">UNRATE</a>]; Chart: Steven Keen)](/_next/image?url=https%3A%2F%2Fimg.theepochtimes.com%2Fassets%2Fuploads%2F2022%2F07%2F18%2Fimage001-600x1025.png&w=1200&q=75)