The older a bull market gets, those who are paid to comment on it become more and more desperate for new things to say about it — a professionally pressing need which tends to split the pundits into two distinct camps, each equally one-eyed about whether prospects are good or bad.

Among them is a group of doomsayers who first peddled the line that loosening monetary policy has become ineffective; now they say that the central planners at the Federal Reserve (Fed) are about to set the whole temple crashing down by tightening monetary policy again.

Alas, they can’t point to serious interest rate rises yet, not when the Fed has so far only managed a paltry one percent upgrade in the Fed Funds Rate to 1.25 percent, still lower than annual consumer price inflation. Also, the fall in long-term yields and credit spreads means that financing terms are, if anything, easier than they were before the Fed began to tighten.

Beyond that, they say the Fed is about to reduce the size of its balance sheet and reverse the Quantitative Easing (QE) programs launched after the financial crisis.

Balance Sheet Dynamics

Given that the post-crisis quintupling of the Fed’s balance sheet to the present $4.5 trillion was the very essence of ‘quantitative easing’ — the process by which banks and zombie firms were rescued, borrowers favored at the expense of creditors, spendthrifts helped and savers hindered, capital allocation tainted and stock markets turbo-charged — how can the reversal of this process not cause financial destruction? In fact, it has already happened — without the ensuing destruction.

Here, it may surprise the reader to learn that the Fed stopped expanding its balance sheet a little over three years ago and that, notwithstanding this, the narrow money supply has grown by around $700 billion, and a broader measure of money in the banking system (M2) by about $2.4 trillion; personal income has risen by an eighth, and economy-wide spending by around 10 percent.

But the base on top of which all other money grows is composed of the reserves that banks hold at the Federal Reserve. They have fallen by roughly $600 billion, or by just over a fifth, without much of a fuss.

So, what gives? How has such a mighty change been effected and yet been almost entirely disregarded by market observers? There are three main reasons.

Regulation and the Eurodollar

Firstly, we must point out that modern, advanced economy banking does not, in fact, operate via the classic reserve-multiplier mechanism on which this forecast relies, but rather on the basis of its constituents’ regulatory (risk-weighted) capital, as first standardized in the so-called Basel Capital Accord of 1988.

This means that even if banks have excess reserves at the Fed, they may not be able to make more loans because regulation prevents them from doing so.

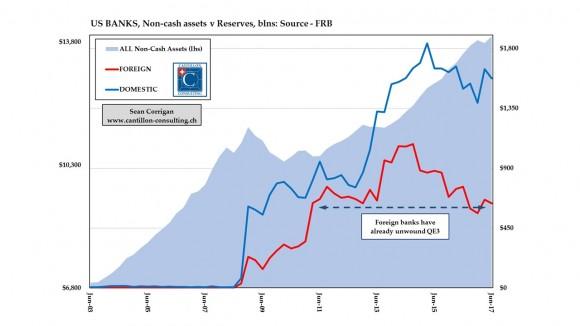

The second factor arises from the behavior of those foreign banks horribly caught out in 2008 by the huge cross-border financing they had been running to finance both America’s and their own, home-grown bubbles.

One estimate of the resulting ‘Eurodollar’ credit market puts its size at around $10 trillion on the eve of the Great Financial Crisis. This market is a ’shadow' banking market where foreign banks lend each other dollars they create independently of the U.S. domestic banking system. It is roughly equal in magnitude as the entire U.S. banking system itself.

Against this vast lending effort, foreign banks in the United States held less than $1 billion in reserves.

In the wake of the collapse, the Fed was soon scrambling to ease some of the ensuing pressure by supplying $500 billion in dollar ’swaps’ to its various counterparts around the world. This allowed foreign central banks to supply dollars to their banking systems as the global credit pyramid collapsed.

Suitably chastened, over the next few years, foreign banks entirely reversed themselves and built an unprecedented $1.1 trillion war chest of reserves at the Fed — a sum that represented a massive 40 percent both of their combined total assets and of the overall total of such reserve balances conjured into existence via QE. Finally, they could sleep at night.

But here’s a little secret. As the perceived need for such a backstop has faded, nine years on from the catastrophe, foreign banks have already reduced their holdings of reserves by over $500 billion – or by a little under a half. Did you notice the accompanying crisis?

The Money Factor

This brings us to our final factor, one which is rooted in a subtlety of money itself.

In normal circumstances, people can be relied upon to hold as little of their wealth as possible in the form of ready cash since it yields little or nothing and, more broadly, because its retention represents an abstention from the enjoyment of other goods and services with little reward for associated self-denial.

Thus, when everything is running smoothly, the bulk of the money in existence is only there to provide a transactional medium; a means through which to buy and sell all the countless billions of things we exchange with one another each day.

Currently, however, we are in a situation where the difference between the (classically zero) yield on money and that on the safer alternatives – such as savings accounts, money market funds, and T-Bills, for example – has become negligible.

Because there is no opportunity cost to holding money in cash or demand deposits, its use as a store of value has increased. People just save cash rather than spend it, which is why the velocity of money has collapsed.

Not only does this partial ‘immobilization’ of the Fed’s money flood explain the relatively sluggish response of inflation to the new abundance of QE money, but it also strongly suggests that, as ’renormalization' progresses, it can be unwound to a large degree without any adverse consequences ensuing, as people switch back to holding what they are not about to spend in the traditional forms instead.

In fact, through an ongoing process of substitution between the medium of exchange and a primary store of value, that missing $500-odd billion has been quietly locked away out of harm’s way, elsewhere in the system.

$200 billion has gone into issuing extra notes and coins - some of which circulates outside the territory of the fifty states, to boot.

Also, the U.S. Treasury, the Government Sponsored Enterprises, and various foreign central banks have increased their accounts with the Fed to the tune of some $350 billion rather than depositing it with the commercial banks. Finally, increased use of the Fed’s new-fangled reverse repos (repurchase agreements) have absorbed another $80 billion or so.

All of this means that while the Fed has not strictly reduced its balance sheet yet, it has already neutralized around a sixth of it by lowering the crucial bank reserves. It has achieved this to the accompaniment of precisely zero dogs barking in the night.

Sean Corrigan is the principal at investment advisory Cantillon Consulting.