Many people in Washington hoped for much better inflation numbers in February. Below zero would have released tears of joy following the recent rough weekend of bank failures and the first signs of financial instability in these three years of nonstop terrible. Alas, that didn’t happen.

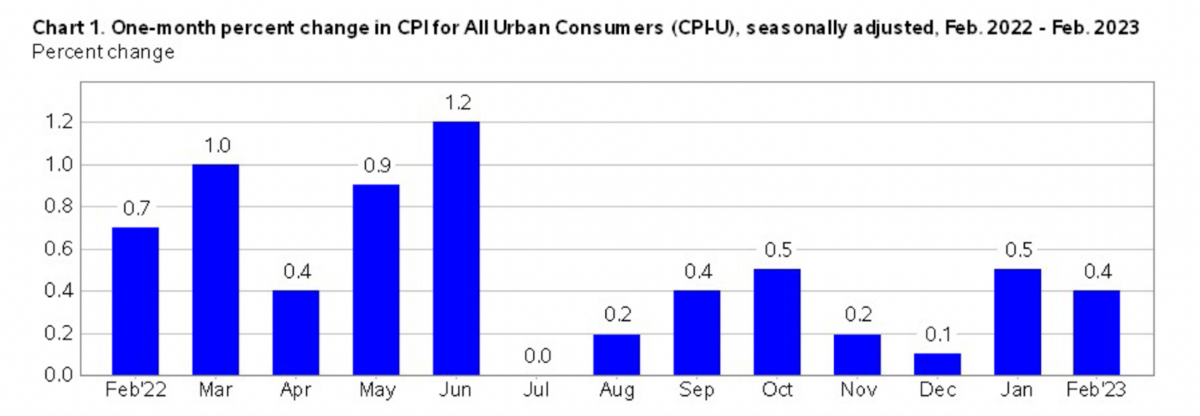

The report came in at a 0.4 percent increase for the month and 6 percent for the year, or three times the Federal Reserve’s target.

Drilling down, there are some really terrible hot spots. Food at home, energy services, and transportation all registered double-digit increases on an annualized basis. You know this intuitively by looking at your utility and grocery bills. Shopping used to be a pleasure. Now, it’s nothing but pain. We look at those steaks, eggs, and even veggies and think twice and three times. We stand at the cash register with dread. The bill comes and we shake our heads with sadness at what we’re going through.

Remember the days when we would shop with smiles on our faces, see and greet friends, and leave with a spring in our step? Those days are gone, replaced with grumbling, sadness, and deep annoyance all around. Every aisle is filled with crabby people who have a sense that they’re getting pillaged. We’re alarmed not only by the high prices but also by the magically shrinking packages.

“Good time to be on a diet,” everyone thinks. The diet called “one meal a day” (OMAD) starts looking very attractive. And truly Americans of all classes would do well to examine their eating habits. But one might prefer to do that under less financial duress.

It’s fair to observe that inflation isn’t getting worse at the same pace it was last year. But a declining rate of worsening is nothing to cheer about. The Fed must still deal with a depreciation rate of the dollar in terms of goods and services that it can’t tolerate. The dollar has already lost 17 cents of value in two years. Something has to change.

Informed opinion over the weekend hoped that the Fed would stop the wild war on inflation with fewer rate increases over the coming months. My own read on central bank Chairman Jerome Powell is that he’s in no mood to do that. He made up his mind two years ago that he was wrong to accommodate Congress’s spending mania because of a virus and reversed course.

He further knew that his rate increases would naturally devalue the portfolios of major banks that had stored their cash excess in fixed-rate government securities and other mortgage-backed products. They had plenty of time to sell those at a discount. As far as he’s concerned, the balance sheet problems of Silicon Valley Bank aren’t his problems. They’re a matter for the risk-management team to solve.

It also appears that there’s a real difference of opinion between the Fed and the Biden administration at this point. The Biden administration, via the Treasury and the deposit insurers, has gone out on a limb to guarantee the deposits of failing banks—an absurd and dangerous promise that can’t be applied across the board. Powell didn’t make that decision but neither is he in a position to stop it. That’s for regulators to decide, and he isn’t among them. His job is to land the economy away from inflationary excesses come hell or high water. Unless someone gets to him, my bet is for rate increases to continue.

There are two theories concerning why last week’s bank failures haven’t led to a broader contagion. One credits the Biden administration’s policy of universal deposit insurance, although it’s more likely that the particular failures weren’t systemic but rather trace to poor management by the banks themselves. It would be nice to know. All the Biden administration had to do was let them fail and watch the results. Alas, that didn’t happen.

A major factor in why the Biden administration did the wrong thing owed to major players in industry and banking screaming that something had to happen. In a panic and watching financial opinion turn ever more south on a Sunday, the regulators jumped in to promise something that’s simply impossible: universal guarantees. This was a huge error.

Another error was putting President Joe Biden on stage to promise the American people that the banking system is sound; it’s like these people truly believe that they still have credibility. They don’t. Viewers listen to them and naturally assume that the opposite is true. Free advice: Never trot that geezer out to assure anyone in a crisis. He has zero credibility, and his every word does damage to any message they want to deliver.

As a result of this mess, we now have two de facto monetary policies operating at cross purposes. We have the regulators captured by the Biden administration pushing looser money and credit and indeed promising more floods to fix any problems that emerge in the future. On the other hand, we have Powell and the Fed sticking to their guns on tighter money to restrain the effects of excesses of 2020 and 2021.

The March 14 Consumer Price Index numbers for February make the point that the Fed still has a lot of work to do. In addition, it’s actually difficult to discern long-run and underlying trends from month-to-month numbers. After all, last summer we saw one month (July) when inflation actually registered as flat. Last month’s numbers seemed to indicate a reacceleration, despite what the headlines said.

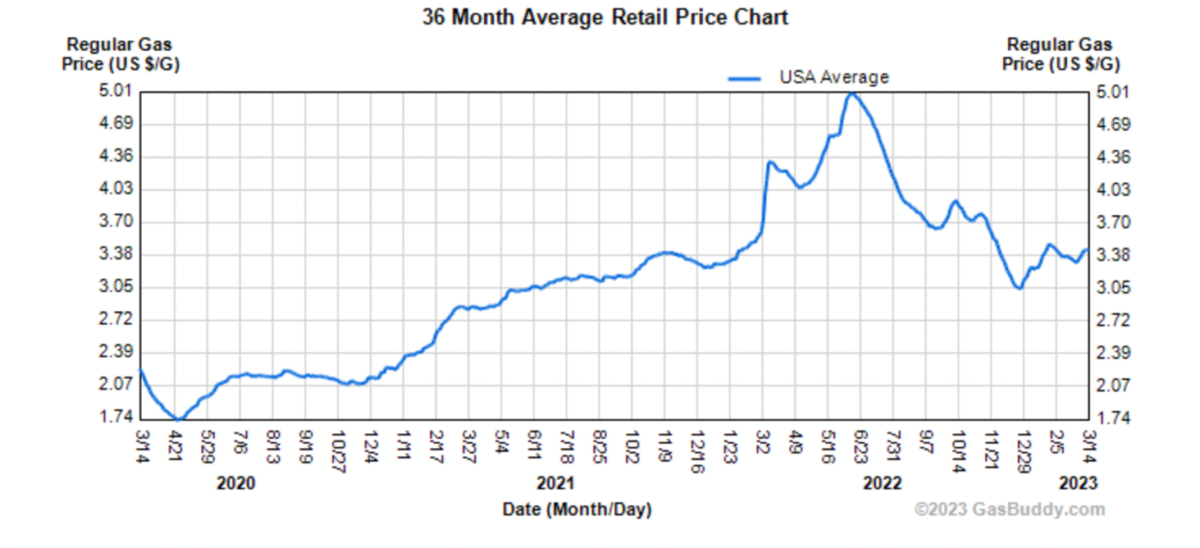

Remember that these numbers are always in the past. What’s going on now? We’re certainly seeing the rate at which food is going up beginning to relax a bit. February was certainly terrible, but March is less so. On the other hand, have you seen gas prices lately? For the year, we’re up by 40 cents per gallon. It doesn’t look good. And we can fully anticipate that renewed demand with spring and summer coming is going to put more upward pressure on gas prices.

Overall over three years, there’s no room for optimism about the price at the pump. This became obvious to me recently when the discount, members-only station had a line around several blocks. People are willing to wait 45 minutes just to save a few bucks on gas. That’s when you know that matters are becoming more intense.

The Fed has more than enough evidence on its side to continue the tightening campaign. This will put more pressure on heavily leveraged companies because the costs of servicing their debt are rising ever more and eating into their capacity to retain huge labor costs. For a sign, have a look at Meta/Facebook, which just announced another huge round of layoffs. This indicates some hardcore balance-sheet pressure.

We’re nowhere near done with this. The right side of the yield curve will continue to offload capital to the left and that means growing layoffs in information technology and professional services, even as retail and hospitality are facing real shortages. The Fed’s determination to arrest the inflation problem means that this shift will continue.

As for the “woke” banks, they'll all likely bite the dust before this is over. And herein we find the silver lining in all this upheaval. We’re getting back to the realities of finance about which markets have been in denial for many years.