Many critics of mainstream economics believe that economists are in the pocket of Big Business: that they’re paid shrills who say what their corporate paymasters want them to say.

With 50 years of experience of economists—and 30 years of that as an academic economist myself, though a decidedly non-mainstream one—I can categorically say that that belief is false.

That is why they are so dangerous.

It’s not because their intentions are bad—anything but. It’s because the vision which they fervently believe accurately describes the real world—and how it can be made better—is utterly false.

My favorite analogy to mainstream economics is Aristotle’s model of the Universe, in which Earth was at its center and the Sun, Moon, planets and stars revolved around the Earth on perfect concentric crystalline spheres. Aristotle’s vision had to be modified, most notably by putting the planets on circles that rotated on their spheres (called “epicycles”), because the planets regularly reversed direction in the sky. But with epicycles and other tweaks, Aristotle’s core vision gave rise to Ptolemaic astronomy, which could predict, with reasonable accuracy, where the planets would be decades into the future. However, as we now know, those models were completely wrong about the structure of the Universe.

Today, we ridicule “Flat Earthers” who continue to believe, despite overwhelming evidence, that the Earth is the center of the Universe. But for 1500 years, that was “mainstream astronomy,” and people who believed—correctly—that the Earth orbited the Sun, were treated as heretics.

That is the state of economics today. There is overwhelming evidence that the mainstream vision of the economy is wrong. But mainstream—or “Neoclassical”—economists steadfastly believe in their vision, and ridicule the heretics like me (Keen 2011) who point out its manifest flaws.

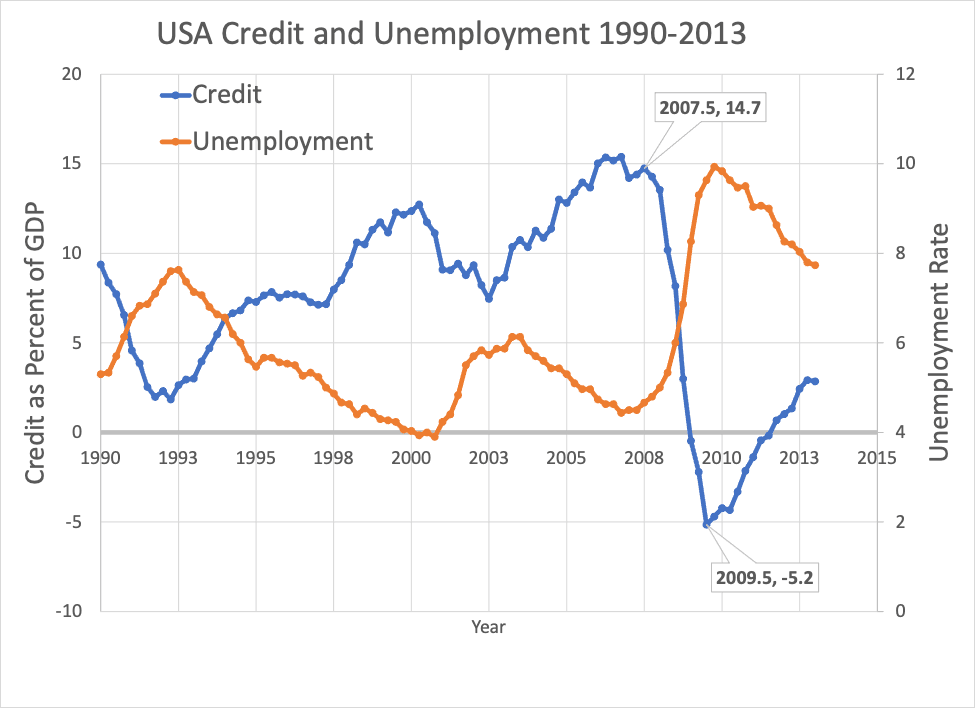

According to mainstream economists like Ben Bernanke, White’s concerns were unfounded because, in mainstream economics, banks are just “intermediaries” between savers and borrowers. “Absent implausibly large differences in marginal spending propensities among the groups,” Bernanke opined, “pure redistributions should have no significant macroeconomic effects.” (Bernanke 2000)

We heretics were right, and the mainstream was spectacularly wrong: rather than 2008 being a year of “sustained growth … and falling unemployment,” it was the beginning of the biggest crisis in capitalism since the Great Depression.

A neutral observer might expect that this huge difference between what mainstream economists predicted, and what actually happened, would lead to some serious soul-searching by economists. And yet the theories that dominate the mainstream today are the same ones that dominated it before the crisis—if anything, these mainstream ideas are even more entrenched now than they were 15 years ago.

Why has the mainstream vision of economics remained unshaken? It’s largely because that vision is one of a perfect world—a Utopia. In the Neoclassical vision of capitalism, there is no power, no coercion: everybody does what they want, subject solely to the constraints of their own resources. Furthermore, everyone receives what they deserve—they get their “marginal product,” to use the econ-speak. The coercive power of the State is something that necessarily makes things worse—we are better off leaving everything to the impartial “market mechanism.” It is, fundamentally, a vision of a self-managing system that would work perfectly, if only all the pesky non-market elements of modern society—governments, trade unions, monopolies, regulations—can be abolished.

Humans seem strongly predisposed to dream of a perfect world, which for religious people is a Heaven. To Neoclassical economists, human society could be made into a Heaven on Earth, if only we followed their guidance. Little aberrations on this march to Valhalla, such as the Global Financial Crisis, are incapable of shaking their faith that this Valhalla is attainable in this life.

That would not be a problem if their vision of capitalism was actually correct, but in reality, it is fundamentally flawed. Since their model is false, their attempts to make capitalism better end up making it much worse. But they remain so committed to their vision that they ignore these aberrations and continue on regardless. In their steadfast belief that they are doing good, they continue to do enormous harm.

References

Bachmann, Rüdiger, David Baqaee, Christian Bayer, Moritz Kuhn, Andreas Löschel, Benjamin Moll, Andreas Peichl, Karen Pittel, and Moritz Schularick. 2022a. ‘Was wäre, wenn … ? Die wirtschaftlichen Auswirkungen eines Importstopps russischer Energie auf Deutschland; What if? The macroeconomic and distributional effects for Germany of a stop of energy imports from Russia’, ifo Schnelldienst, 75.White, William R. 2007. “Bank for International Settlements 77th Annual Report 1 April 2006–31 March 2007.” In. Basel, Switzerland: Bank for International Settlements.