One of the most common arguments stock investors use is that “there is a lot of cash on the sidelines” that doesn’t yield anything and could be more gainfully invested in the stock market.

“It’s just the beginning of money coming in. That’s a large inflow, but certainly not to the point of alarm. I would want to see that for five or six quarters in a row before I would get worried,” said Keith Springer, president of Springer Financial Advisory, to CNBC, commenting on a $75 billion move from money-market funds into stocks in February this year.

So this record cash on the sidelines, whether it’s in brokerage accounts or money-market funds, could be used to invest in stocks, which are producing solid returns. And the language used in the argument implies that if people were smart enough to use that cash to buy stocks, then cash balances would fall and stock prices would go up higher.

There is only one problem with this argument: The cash doesn’t go away.

Indestructible

People have indeed been using the “cash on the sidelines” to buy stocks and plenty of them, but buying stocks doesn’t extinguish cash assets. The money just goes from the buyer to the seller and then sits on the sidelines in his account.So instead of looking at the absolute amount of money that’s held in cash, one needs to look at the relative amounts. Because it is true that the frequent changing of hands of that cash and the buying of stocks does bid up the price of the stock market. People value owning stocks more than owning that cash. So the stock buyer has to make a better offer to the seller who may say, “What do I want with all this idle cash? Give me more of it to part with my dear stocks.”

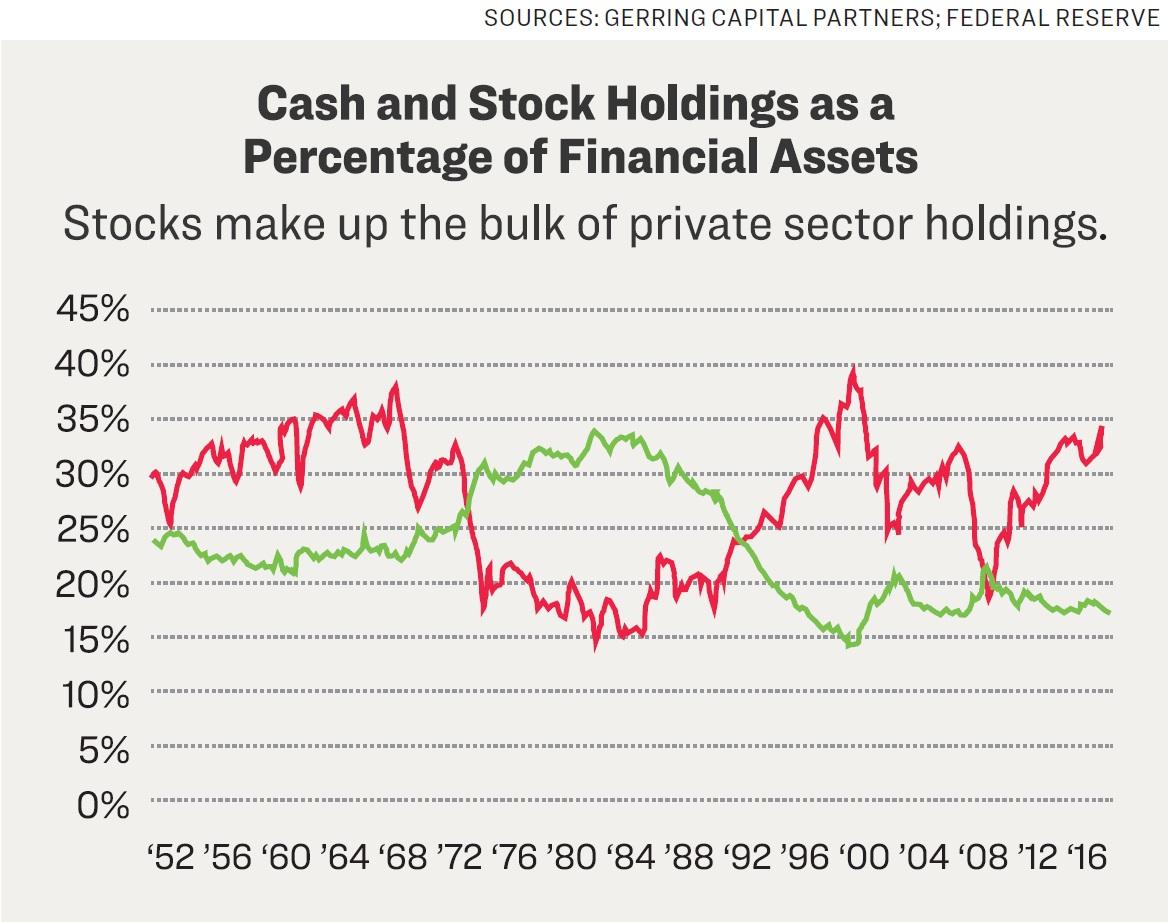

The adjustment or the valuation of “cash on the sidelines” works through stock prices. As prices move up and cash prices stay the same—it is cash, after all—it naturally becomes a smaller part of the asset allocation mix of households and companies.

No Cash Left

In fact, if we start looking in some other places, we find that there isn’t that much stock-ready cash at all. Mutual fund cash holdings, for example—and these are the people who pull the trigger and buy stocks—is at an all-time low of 3.3 percent, after reaching an intermediate high of 6 percent just after the last financial crisis.This does not mean that the money-market holdings can’t change hands a few more times for higher stock prices until the fundamental drivers of the rally have exhausted themselves. So as long as interest rates don’t rise too high, earnings keep growing, and we don’t experience a recession, stocks may well continue to go higher.

Cash on the sidelines, however, has nothing to do with this.