News Analysis

U.S. stocks have experienced a high level of volatility over the past two weeks. But that pales in comparison to the declines sustained by the Chinese markets over the same period, as a confluence of factors has driven Chinese stocks to their lowest levels in years.

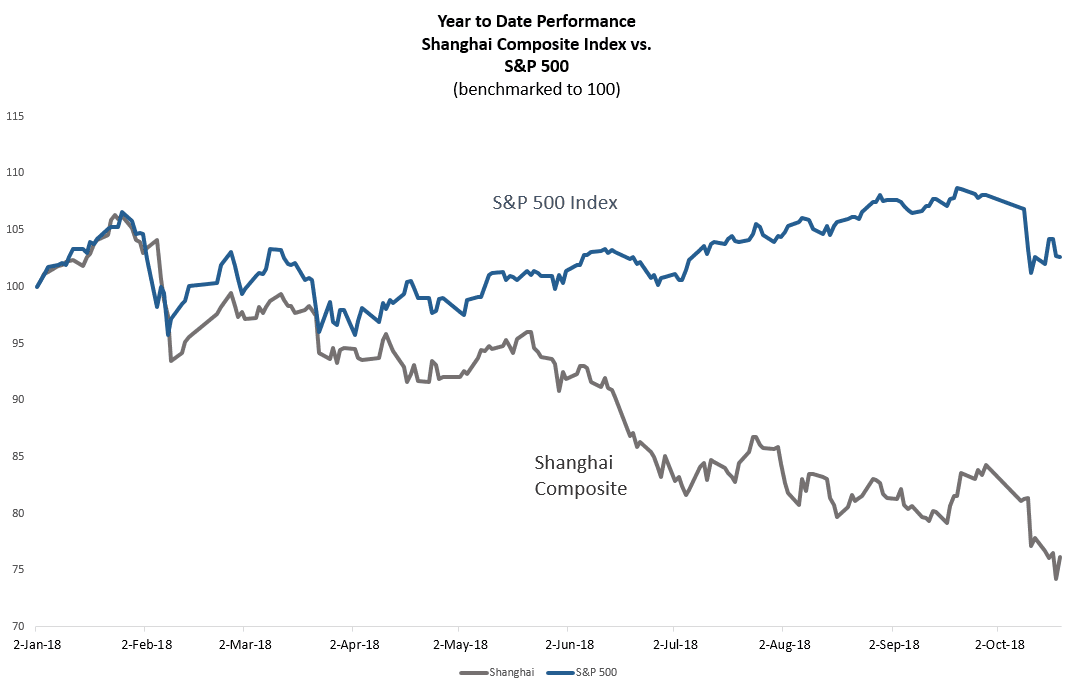

Before a sudden rally on Oct. 19, China’s benchmark Shanghai Composite Index had been down almost 11 percent over the previous 10 trading days, and down about 25 percent year-to-date. The recent downturn sent the Shanghai Composite, which was already the weakest major global benchmark by performance in 2018, to its lowest since 2014.

Stocks turned positive on Oct. 19, after multiple Chinese regulators urged investors to remain calm. The loudest of them was Vice Premier Liu He, a Politburo member and the top economic adviser to Chinese communist leader Xi Jinping.

That snapped a string of four straight losing days for the Shanghai Composite, which rose by 64 points, or 2.6 percent, by the close. The index closed down 2.1 percent for the week.

Liu sought to calm investors by touching on several topics. He downplayed the impact of the continuing U.S.–China trade war by announcing that the two countries “are now in contact with each other,” according to a report by Xinhua, the Chinese state-owned media. Regarding collapsing equities, “the corrections and sell-offs on the stock market are creating good investment opportunities for the long-term and healthy development of the stock market,” he said.

Liu also implored banks to support privately owned companies of all sizes, to “roll out precise and effective measures to help them.”

Liu’s statements came out moments before the release of more bad news. The National Bureau of Statistics posted official data that showed the GDP grew in the third quarter at only 6.5 percent, the slowest quarterly growth rate since the last financial crisis.

Echoing Liu, other regulators also came out to support the Chinese economy, including central bank governor Yi Gang, insurance and banking regulatory chief Guo Shuqing, and securities regulator Liu Shiyu. In addition, the China Banking Regulatory Commission unveiled new draft guidance to give banks greater leeway to invest in the country’s stock market, reversing a recent trend of tighter risk management.

Chart by The Epoch Times

A Perfect Storm

The events of Oct. 19 were a well-coordinated effort by several regulators to stop the stock market bleeding. But will the good vibes last more than one trading session?The selloff in Chinese equities has been propelled by several factors. Major drivers include the trade war with Washington, negative sentiment regarding big tech stocks (which isn’t exclusive to the Chinese markets), concerns over Chinese consumer spending, and currency weaknesses. Unfortunately, none of these catalysts are about to subside anytime soon.

One of the topics receiving less coverage has been the underlying weakness among Chinese technology giants.

While Tencent, at one point, could seemingly do no wrong, the mobile and gaming giant has struggled recently. The company has been caught up in a broader global downturn of technology stocks. Chinese regulation on gaming has also had a negative effect; Tencent recently reported its first quarterly profit decline in almost 13 years.

Gaming has been Tencent’s bread and butter. But its growth has been hampered by Beijing’s decision last month to restrict approving new video games, limit the number of new game releases, and crack down on the amount of time children are allowed to play games. Last month, Tencent announced a divisional restructuring to increase focus on cloud computing and services toward business and corporate clients.

The tumbling domestic markets have also propelled the Chinese yuan towards the key threshold of 7 yuan per U.S. dollar, a level not seen over the past 10 years. China’s domestic problems could send the yuan lower and draw renewed criticism from the United States—a weaker yuan alleviates impact of the trade war by making Chinese exports cheaper.

“So far, we think the tariffs’ impact will more or less be offset by the fall in the renminbi. We'll see a bit of an increasing headwind next year, as tariffs come up. The economy is slowing, but mainly due to domestic factors,” economist Chang Liu of Capital Economics told CNBC on Oct. 18.

The Worst Is Yet to Come

Amazingly, the brunt of the impact of President Donald Trump’s trade war on China hasn’t yet been reflected in economic data.“There hasn’t been any real impact from the trade war yet,” Andrew Polk, from the Beijing-based consultancy Trivium, told the Financial Times. “There’s always another round of tariffs coming that traders want to front-run.”

Through the first nine months of 2018, Chinese exports have actually increased more than 14 percent compared to 2017, which is partially helped by the fact that the Chinese currency has declined against the dollar during the same period.

China’s economic growth could slow at an accelerated pace as more U.S. tariffs take effect early next year. Any attempt to stimulate economic growth could risk undoing recent efforts in promoting financial responsibility. Beijing also faces an uphill battle in its trade war with the United States and rising U.S. interest rates.

Another wildcard for Chinese stock markets is the risk for margin calls, which will make any stock selloff go from bad to worse. Bloomberg estimates that more than $600 billion of Chinese shares are being pledged as collateral for loans, a level that is 11 percent of the country’s total market capitalization.

These aren’t individual investors who borrow on margin, but companies who used their restricted stock as collateral for leverage.

“At least 144 Chinese companies have more than half their shares pledged, often the result of founders using their stakes to raise cash,” according to data from Bloomberg, which noted that almost half—60 companies—have seen their stocks tumble by more than 50 percent this year.

A falling market will force companies to sell their pledged shares, further exacerbating any selloff.

Some of the policy changes introduced last week readied the country’s banks and investment companies to support a wide range of publicly traded companies. Policymakers are no doubt concerned about the potential for a further downward spiral of the stock market.

But investors could soon realize that rescuing Chinese markets will require more than rhetoric.