It would accomplish the ultimate goal: “the euthanasia of the rentier class.” Only this would eliminate “the cumulative oppressive power of the capitalist to exploit the scarcity-value of capital.”

By “rentier class,” he meant the people who live off the earnings of their savings and capital. They don’t have to do anything but watch their bank accounts grow, he said. This is because they are holding on to so much in the form of savings and high-earning capital that they can stop creating, working, or caring much about anything. End that with zero interest rates, and you create a magic world of prosperity for everyone.

The idea sounded bonkers at the time, but economists kept pushing out the core of it, which is that wealth comes from consumption, not savings, and the idle rich are really a drain on productivity. The first nation to attempt this was Japan in the 1990s. It didn’t work. In fact, it led to economic stagnation. If the experts paid any attention to empirical evidence, that would have been the end of the whole theory.

Oddly, instead of learning from others, the United States drifted in this direction starting after 2000. There was a brief pullback from insanity. But then 2008 hit, and the Fed went the whole way. It flattened interest rates out completely. People braced themselves for inflation, but it didn’t happen. The reason: The Fed was paying a higher rate on deposits to banks than banks could earn in the markets. That kept inflation in check.

For 15 years, the central bank patted itself on the back for a job well done. The mastermind of the new Keynesian policy was Fed chairman Ben Bernanke, who was awarded a Nobel Prize for his tremendous innovation. The wicked language of euthanasia of the rentier class had long ago been dropped and replaced by the pretense of scientific management, but the ethos remained.

What happened? The policy created an enormous distortion in production structures. Money hunts return. With zero interest rates, it abandoned regular savings and looked further down the yield curve, where large corporations and highly speculative financial products live. Flush with new cash, they went on a massive hiring spree and built nearly the whole of what today is called the Zoom class or what I would call the overclass.

This was the very class of workers who rallied around “woke” management theories and developed the most profound psychology of entitlement of any workers in the history of capitalism. Their sense of leisure backed by riches far exceeded the expectations of the English aristocracy of the Victorian age. The only difference is that the Zoom class pretended to have jobs while the aristocracy pretended not to.

This whole charade was completely unsustainable, but it did massively corrupt corporate America. In a period of tremendous technological innovation that should have reduced labor costs, the opposite happened in the corporate sphere. They met every need by throwing human labor at it, even while eschewing new digital tools.

Just as one example, one of the fastest-growing sectors of corporate life has been the human resources department. It’s all been preposterous since every function of HR, from payroll to whiny complaints about co-workers, is easily handled by software platforms that cost a mere 1 percent as much as whole HR departments. But did they use them? No! They puffed up the management structures, the C suites, the mid-level positions, and HR to preposterous extents.

It got to the point that vast numbers of white-collar workers in this country had nothing to do except pretend to work. This is why lockdowns appealed to them. Why not do nothing at home in your PJs rather than slog to the office and do nothing? This is a generation of workers that had already and long ago lost touch with the basics of productivity itself. And they had learned to otherize people who do work as bit players not worthy of their attention.

2020–2022 was their heyday. They could sleep late, slip into comfy clothes, turn on their mouse jigglers, watch movies, and still enjoy the creeping up of their stock portfolio. Food you could get with a few clicks. The workers and peasants take care of the rest.

In other words, Keynes’s solution to the supposed problem of the rentier class actually created something far worse: the ultimate leisure class that had massive income flows but no work to do at all! The Zoom class is far more egregious than the rentier class ever was. At least the rentier class wasn’t woke.

I knew when the Fed started to raise interest rates that this would have revolutionary economic, cultural, and social implications. It would massively shift labor resources away from the right side of the yield curve to the left. This would mean retraining an entire generation away from fake jobs into real ones. It would amount to a massive trauma.

“We need people to fix cars, deliver goods from ports to stores, flip the rooms in hotels, make the omelets, and put up drywall in new houses. Those require skills and actually moving one’s body, which is anathema to the under-40 demographic that studied anthropology and the history of social oppression of everyone during the four-year, debt-financed vacation we call college.

“A prediction: there are hard times ahead for the corporate laptoppers as these companies are forced either to become profitable or go bankrupt. And this will lead to a massive crisis and demoralization of an entire generation that has been taught that anyone with the right credentials and connections can get rich forever without doing a lick of real work.

“Decades of debt financing have created a spoiled overclass in America that has been taught to hate capitalism and also believe they and their friends can forever earn a high-income stream off the fruits of that system. There could be a rude awakening and it could come sooner rather than later. They wanted a great reset and they are going to get it good and hard.”

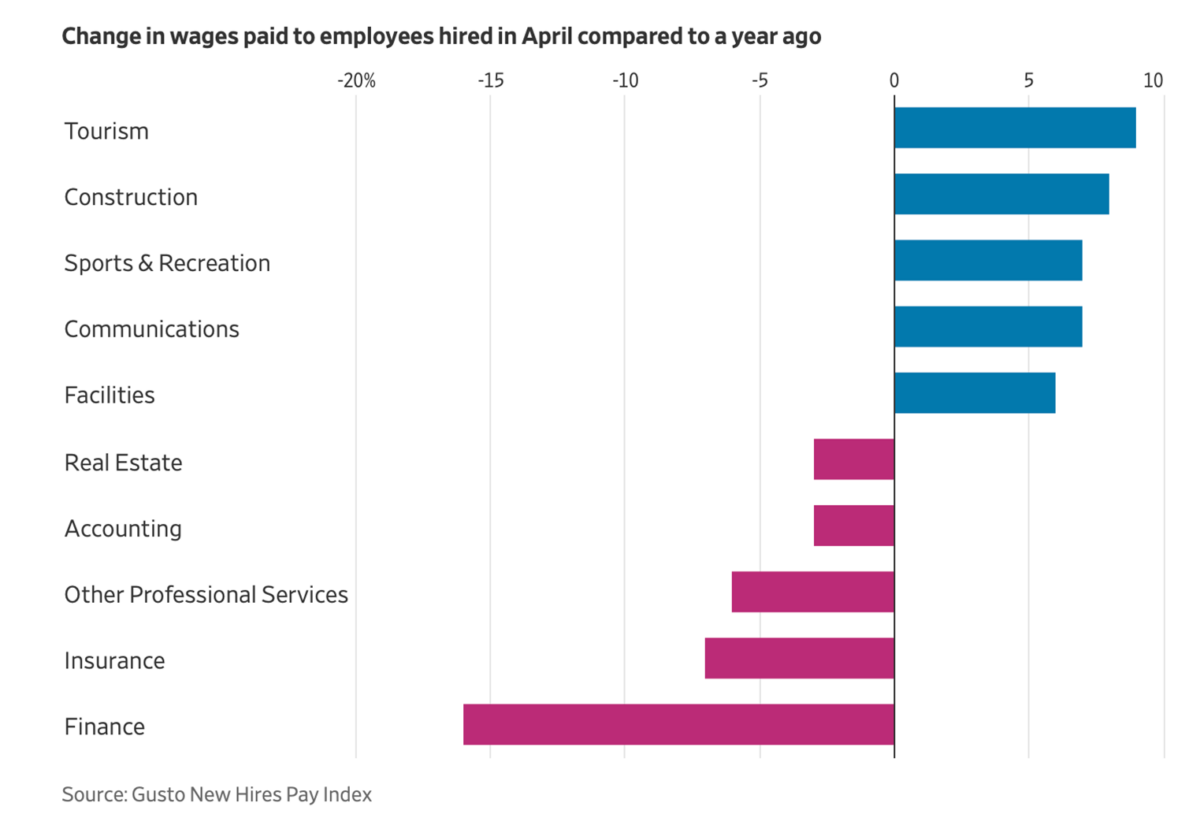

The layoffs are coming fast and furious in high-end sectors. Layoffs in the information sector were up 88 percent in March from a year earlier. They are up 55 percent in finance and insurance. Companies are keeping restaurant cooks and servers, warehouse workers and drivers, but middle managers are biting the dust. It’s the euthanasia of the overclass. That’s precisely what one would predict with rising interest rates.

This is the great challenge for an entire generation: to rediscover actual work and how that is related to pay. It’s affecting everyone now in their early 20s who are considering careers for their future. It’s utterly traumatizing white-collar workers in their 30s and 40s.

But no matter the wailing and gnashing of teeth, economic reality will have its way. The ground is shifting beneath our feet. America has to learn to work again, even if that means changing the white collar to blue, or else there will be no economic future about which anyone will have bragging rights.