“As the Federal Reserve aggressively raises rates to combat persistent inflation, the tough stance could come at a price. Already, falling stock markets have wiped out more than $9 trillion in wealth from U.S. households.”

Fed Chairman Jerome Powell also warned the central bank’s upcoming moves to fight soaring prices may cause “some pain” ahead.

Interestingly, while individuals continue to suffer from “recession fatigue,” the economy is technically not in a recession. At least not yet, because the National Bureau of Economic Research (NBER), the official arbiter of recession dating, has not made that assessment. With unemployment rates at record lows, jobless claims at historically low levels, and consumer spending still above trend, an official recession likely has not yet begun.

However, don’t ask the average American whether there is a recession or not. According to the Bankrate.com report, the average American has an entirely different view.

According to Bankrate.com analyst Sarah Foster, “Recession depression, recession fatigue, whatever you want to call it, the hits to Americans’ financial security keep coming. First, it was the devastating coronavirus pandemic, followed by 40-year-high inflation, and now the growing risk of another downturn. Sustaining motivation for two-plus years to prepare for tough economic times can no doubt feel exhausting.”

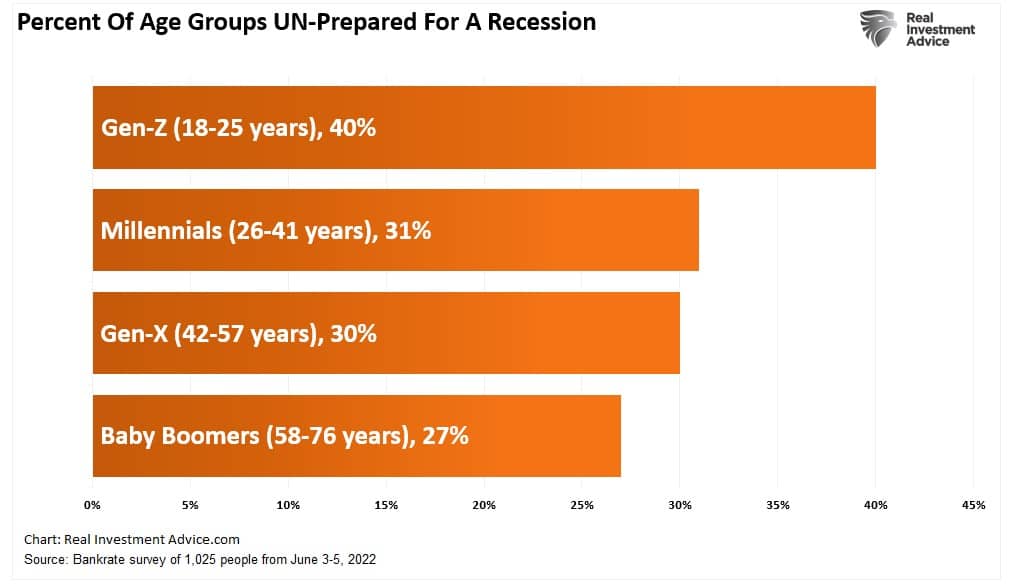

When respondents are broken down by generation, younger adults, those of Gen Z, are more likely to experience “recession fatigue” than millennials, Gen Xers, and baby boomers. In the report, “recession fatigue” is primarily afflicting younger generations, leaving them unprepared to face a recession. Such data certainly fly in the face of media reports of households having “strong financial balance sheets.”

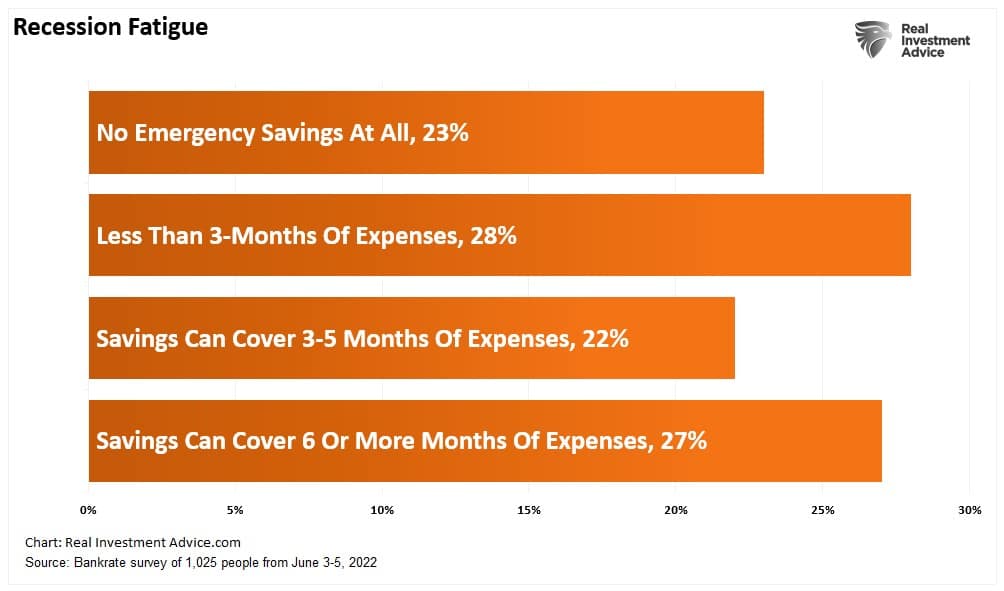

As we have discussed, households remain woefully short on savings, despite a booming stock market over the last 12 years and $5 trillion in fiscal stimulus.

The Great Termination

During 2020–21, as the federal government sent checks directly to households and companies forced older workers into early retirement, the period became known as the “Great Resignation.” Naturally, that all worked well—until inflation surged to the highest level in 40 years, and all those that opted for “retirement” began looking for work to make ends meet.Now, as the economy begins to slow and individuals are struggling with “recession fatigue” just trying to pay bills, the “Great Termination” is coming. Such is evident from a recent KPMG survey of C-suite executives who are ringing alarm bells about a looming recession.

“Nine in 10 CEOs in the United States (91 percent) believe a recession will arrive in the coming 12 months, while 86 percent of CEOs globally feel the same way,” according to the findings by the international audit, tax, and advisory firm KPMG.

In the United States, half of the CEOs (51 percent) say they’re considering workforce reductions during the next six months, and in the global survey overall, eight in 10 CEOs say the same.

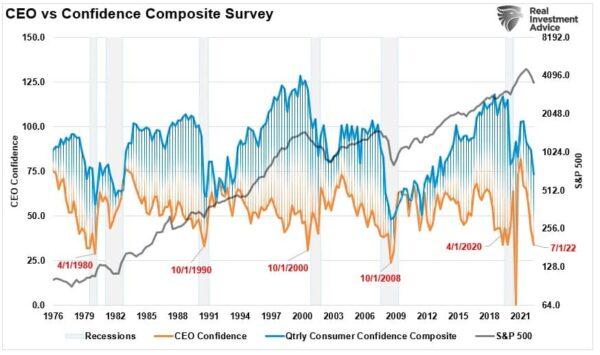

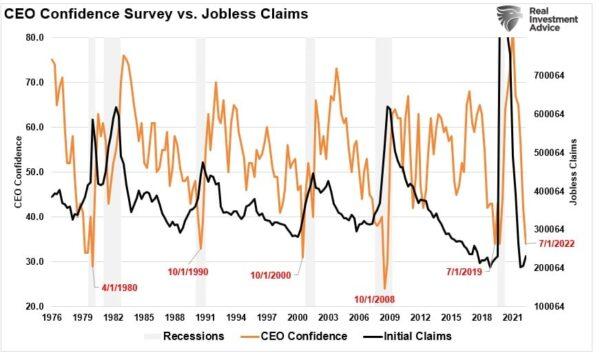

That sentiment is not surprising, given the symbiotic relationship between consumers and corporations. As shown, there is a high correlation between consumer sentiment and CEO confidence. Corporate revenues are derived from consumer demand. Therefore, when consumers limit their spending due to “recession fatigue,” corporations take defensive actions to protect profitability.

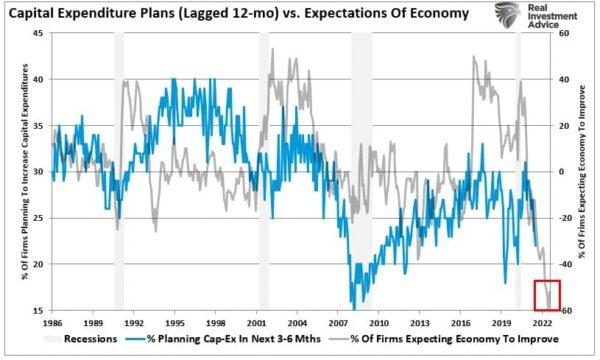

Notably, given that “good” employees are hard to find, expensive to train, and challenging to replace, companies tend to be “slow to hire and slow to fire.” As such, they start with essential cost-cutting and then proceed to cuts in capital expenditures (capex.) According to survey data from the National Federation of Independent Business, the current level of capex spending is associated with previous recessions.

Once corporations reach the limits of cost-cutting, terminations eventually follow. As shown, CEO confidence at such low levels coincided with low jobless claims. Notably, jobless claims do not trend higher; they spike as terminations come rapidly.

‘Recession Fatigue’ Won’t End Soon

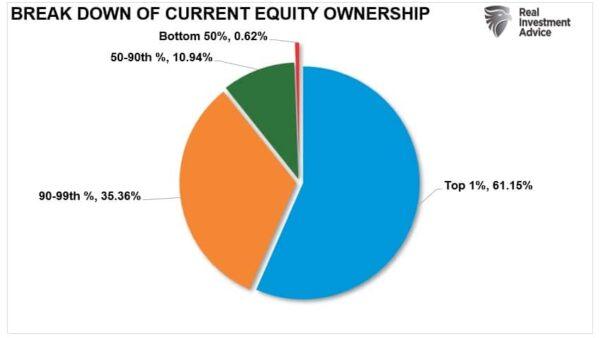

Numerous articles suggest the economy remains healthy due to the “fiscal health of household balance sheets.” For example, from the Harvard Business Review:While that is a true statement, the reality is far more insidious. Most of those savings are held by the top 10 percent of income earners. Those are the same individuals who own about 90 percent of the household stock market wealth.

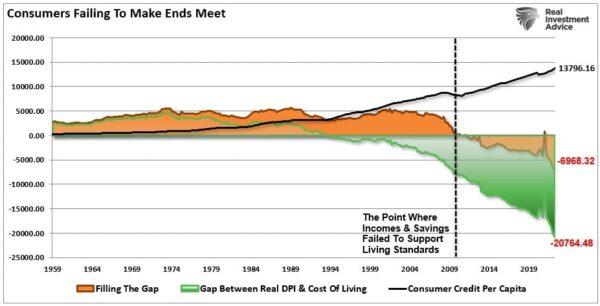

It is a far different picture for the bottom 90 percent of Americans. Those households have few choices but to tap credit cards to fill the gap between living costs and incomes.

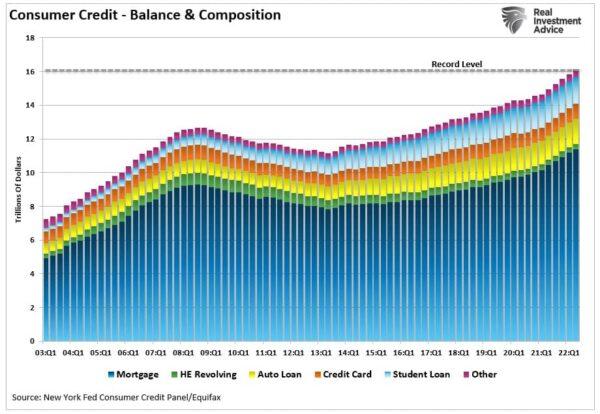

According to the latest report from the Federal Reserve Bank of New York, credit card debt surged by $46 billion in the second quarter. As shown above, such is not surprising as consumers struggle to maintain their standards of living. The 13 percent annualized increase in new debt was the largest in more than 20 years. Moreover, aggregate limits on cards marked their most significant increase in the last decade.

One thing is likely certain: When the economy breaks, inflation will no longer be a problem. What will be problematic is when the Federal Reserve scrambles to fix what it once again has broken.