When a writer starts a new column, his first battle is to justify why people should read it. Paul Krugman has just made that task much easier for me, by publishing a column on money that, to use his favorite phrase, is “all wrong.” The crucial point at which Krugman gets it “all wrong” —yes, a Nobel Prize winner in Economics is wrong about money—is his assumption that, when they lend, banks lend out reserves:

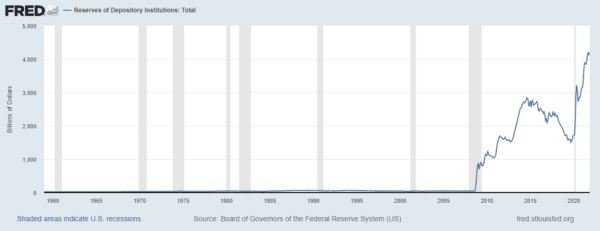

Since the 2008 financial crisis, however, banks have been voluntarily holding vast excess reserves, apparently because they don’t see enough good lending opportunities.

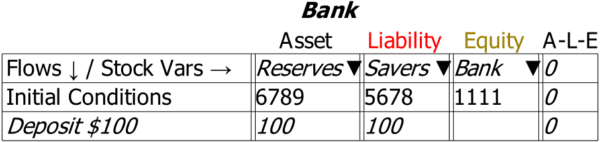

Firstly, a deposit in a bank does create reserves for that bank. If you deposit a $100 note, then the bank physically puts that note in its vault, and gives you a receipt that it owes you $100. The actual note in the vault is an asset of the bank; your receipt—which these days is an entry in a computer database—is a liability of the bank. The bank’s reserves rise by $100, and the bank accounts of savers rise by $100, as shown here:

So, after the deposit, the bank’s reserves rise to $6,799, and the savers’ bank accounts rise to $5,688. Now, what happens when the bank wants to loan $100 to borrowers? The real-world situation—the one described by the Bank of England, not Krugman—is shown here. The bank credits the borrower’s deposit account with $100, and simultaneously records that the borrower owes it $100:

Notice that nothing happens to reserves: they have nothing directly to do with real-world lending. Instead, as the Bank of England says, “the act of lending creates deposits.”

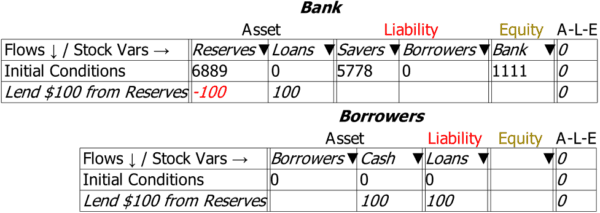

It’s useful to try to model what Krugman, and all other mainstream economists, think actually happens—to show why they’re wrong. Lending from reserves means that the banks takes $100 out of reserves—so the entry there is -$100. Simultaneously, the loan to the borrower goes up by $100:

So far, so good, but there’s a problem: the borrower now has a debt to the bank, but at the moment, no money! Where is the money for the borrower?

There are only two ways to make the “lend from reserves” story work. One is that the loan is in cash (or some other negotiable instrument, like a bank cheque) to a customer of that same bank. Then, the borrower leaves the bank with $100, which makes up for having a debt of $100 to the bank:

Now ask yourself: when was the last time you got a loan from a bank in cash? It happens occasionally, when someone uses their credit card to get cash out of an ATM (at a prohibitive rate of interest), or a shopkeeper borrows a cash float from a bank. But the vast majority of loans today involve the bank simply crediting a deposit account.

The other way (not shown here) is that one bank lends only to customers of another bank. But this doesn’t actually involve “lending out reserves” in the aggregate, which Krugman is musing about in his article: the reserves of the lending bank fall, while the reserves of the borrower’s bank rise.

So, one way of making Krugman’s “banks lend from reserves” model work is fanciful in the modern age, while the other way doesn’t actually cause aggregate reserves to fall. And both ways involve something far more complicated than the simple and realistic model of banks crediting a deposit account, and simultaneously making an identical entry on a loan account.

Therefore, the fact that banks create deposits when they lend is not a mystery: it’s obvious. The real mystery is, why do mainstream economists persist with a cumbersome, false model of what banks do, when a simple, correct model exists?

Partly, it’s laziness: this is what they learnt from the textbooks they learnt from, and it’s easier for them to repackage the same-old-same-old today than it is to model something new.

I’m all for including the banking sector in stories where it’s relevant; but why is it so crucial to a story about debt and leverage?

Why indeed? I’ll discuss that in my next column. In the meantime, if you subscribe to the New York Times in order to read Krugman, you might consider making a better use of your money, and subscribing to The Epoch Times instead.