You didn’t want or need more bad news on the price front. But here we are in any case.

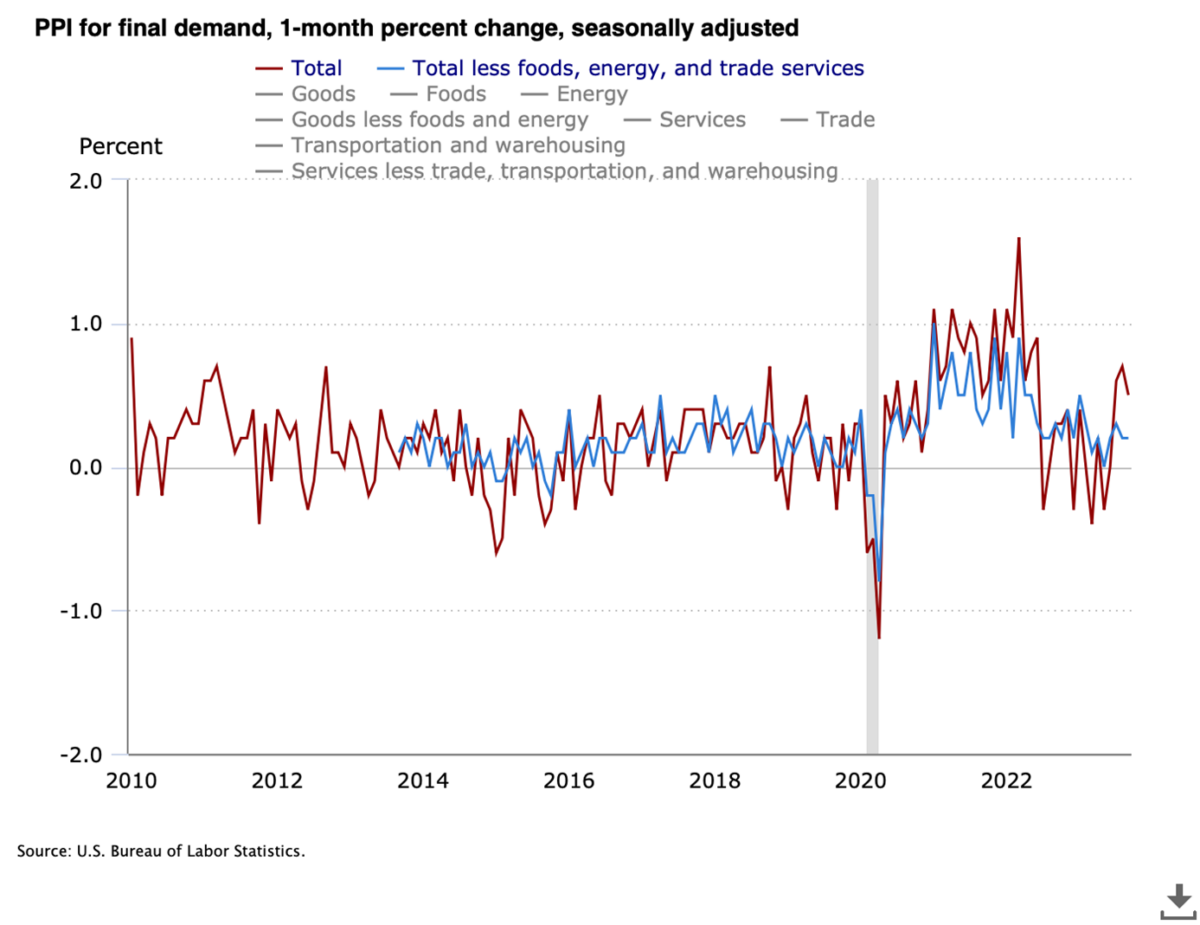

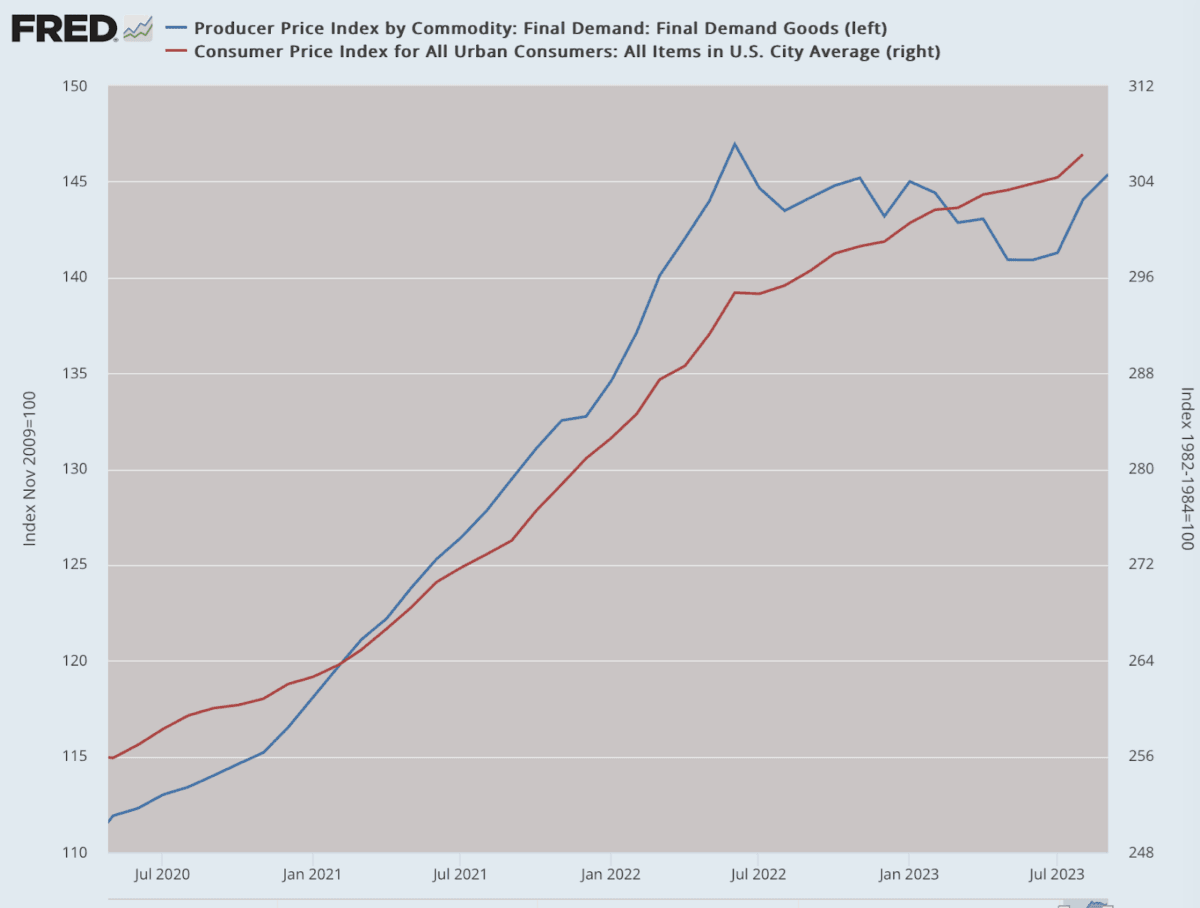

Close watchers of price trends had a bout of optimism as we approached summer this year. Wholesale prices (producer price index) seemed to be settling back down again. Businesses at all levels experienced some relief. I was among those who fully expected this good trend to be reflected in consumer prices. It seemed like the great inflation was coming to an end.

Sadly, this didn’t happen. Consumer prices continued to rock on. That turned out to be a very bad omen that few expected. The grim truth is in the producer price index report. In short, after a brief respite, they’re surging yet again. This is all about the rising costs of doing business.

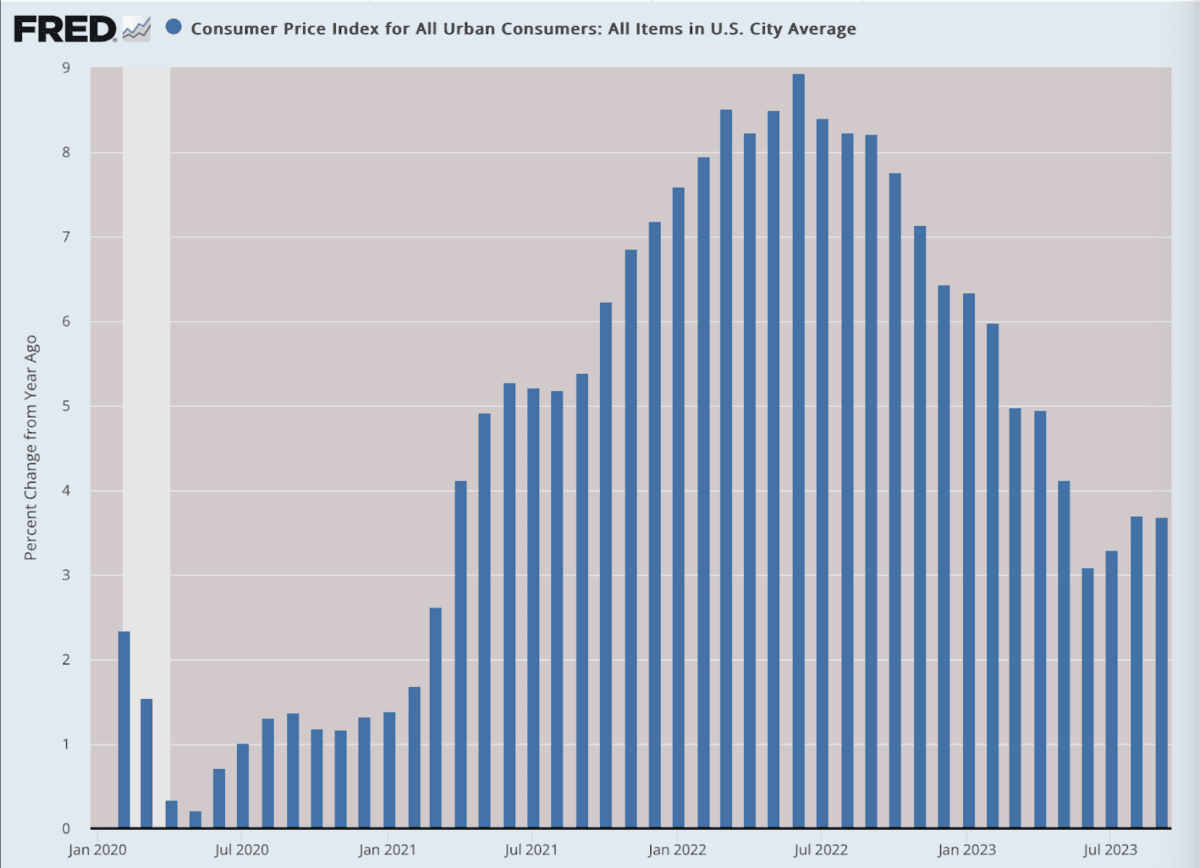

By now, we should have experienced flat or, even better, dramatically falling prices. That would have been a boon to businesses all over the country. Instead, we’re confronting the opposite. This will probably be reflected in consumer prices, too, over the coming months. Already, the latest consumer price index shows no improvement over the past month. The numbers were too hot (3.7 percent) even for the press to attempt a good spin.

By now, we should have experienced flat or, even better, dramatically falling prices. That would have been a boon to businesses all over the country. Instead, we’re confronting the opposite. This will probably be reflected in consumer prices, too, over the coming months. Already, the latest consumer price index shows no improvement over the past month. The numbers were too hot (3.7 percent) even for the press to attempt a good spin.

The much-heralded end of high inflation turns out to be a head fake. There’s no reason now to assume that high inflation is in the rearview mirror. It could last and last.

You can already feel it at the grocery store: Prices are on the move again.

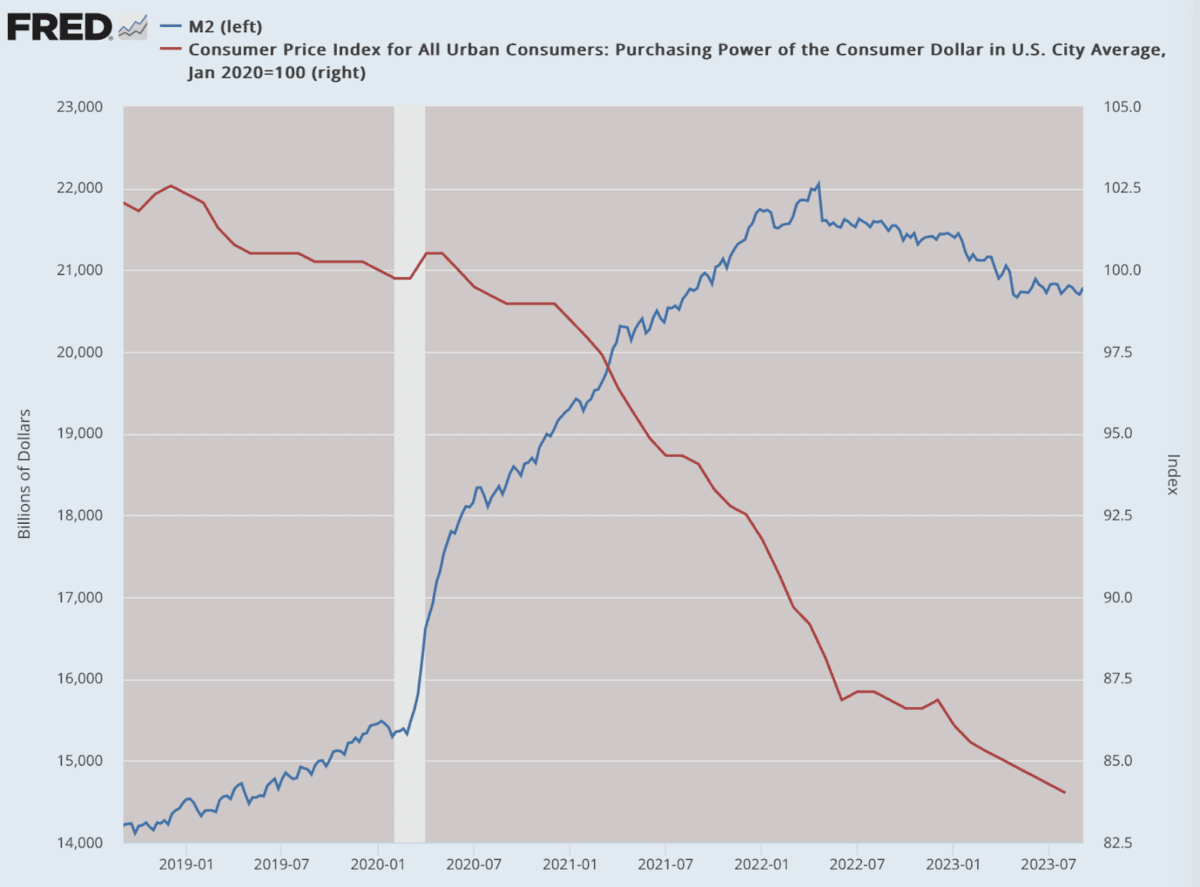

Part of the problem with predictions on prices these days is that we’ve never been in a pickle like this before. The core issue is this: Between January 2020 and October 2023, the quantity of money in circulation as defined by M2 has surged by 34.4 percent.

That’s just the raw truth. Because we’ve never seen anything like that in the history of the Federal Reserve, we’ve had no real gauge to anticipate how long it would require before that increase integrated itself fully into the economic landscape.

And it hasn’t happened evenly. Just as one sector settles, another settles, and then it moves back again, like a virus that grants no immunity from recovery. The stuff just keeps sloshing from place to place. The Fed’s policy of rate increases put a stop to the surge in money quantity but hasn’t effectively put a stop to the impact of past printing.

Like a virus, it has to become endemic. There’s no vaccine that works. How and when we'll achieve herd immunity is the great unknown. And as with epidemiology, the models didn’t work. Nothing about the Fed’s behavior in these years has mitigated against economic crisis; indeed, the opposite has happened.

In just three years, the effect has gobbled up at least 16 cents of every dollar—and maybe as much as 20 cents—with an incredible effect on the purchasing power of money. In broad terms, this feels like a confirmation of Milton Friedman’s model of money and its relationship to inflation. But even more than that, the policy comes on the heels of 15 years of wild distortions in the production structure that are nowhere near being resolved.

This strain on household finance is like nothing we’ve experienced in four decades. For several generations now living through this, it’s all entirely new. Plus, people younger than the age of 40 never had to balance a checkbook. It was done by the bank. Same, too, with payments. Just throw down that card and never look at prices. People got out of the habit of even comparing prices.

Now they look at their cash balances and their bills, and the shock arrives. Even though the inflation goes back 2 1/2 years, it seems like people are only now waking up to the terrible reality of dramatic declines in living standards.

Sadly, too many people believed our rulers when they promised that all of this was transitory and that the economy was in excellent health. Just look at the unemployment numbers—and never mind that 5 million people having dropped out of the workforce after lockdowns skew the numbers to the point of being completely useless.

Frugality should have been the practice starting in the spring of 2020. Now, it’s too late, and panic is starting to set in among a middle-class cohort. Savings are declining and debt is rising, exactly the opposite of what’s supposed to happen when interest rates rise. This is because people have already committed whatever income they have. So they’re trapped.

What can the Fed do to fix this? Nothing. The damage is done. What will they attempt to do? Very likely, if there’s another crisis—and that increasingly seems likely—they‘ll crank up the printing presses yet again. Then we’ll see another bout of inflation on top of the one that’s here and not going away.

The temptation for any central bank to accommodate the spending habits of the political elite is too great to resist. We have more than a century of evidence to that effect. The Fed’s power must be curbed. This is the only long-run solution to the problem.