President Donald Trump has fired Lisa D. Cook from the board of governors of the Federal Reserve. Not a soul in the know believes that this one step is fundamentally disruptive to Fed policy or monetary stability or will have any meaningful impact on anything at all. And yet, within minutes after the letter came, it was the above-the-fold in every major news source in the world.

Why might this be? Because Trump is the first president since the Fed’s founding who has dared to fire a governor of the Fed. The first ever. He is testing the system. Is the president the president, or does the central bank stand over him in authority? Everyone in the United States and the world should care about the answer. It’s a matter of who is in charge: the people or the bankers?

Meanwhile, Cook has told the media that she will not resign.

“I will not resign,” she said through her attorney. “I will continue to carry out my duties to help the American economy as I have been doing since 2022.”

What does the boss do when the employee he fired refuses to go? He or she files a lawsuit, which is exactly what has happened. The courts will decide. The stakes are high. The Fed itself will finally face a test after so many long years of confusion over its status in American constitutional government.

Article 2, Section 1 of the U.S. Constitution is clear: “The executive power is vested in the President of the United States.”

I see no wiggle room there. The Fed is, in fact, an agency under the executive branch.

But can the president really remove a governor? Certainly, says the U.S. Code: 12 U.S.C. §242. Any can be “removed for cause by the President.” In business, this is called “at will” employment. The president is the boss. It’s not complicated.

Trump found that Cook had filled out mortgage applications listing two simultaneous primary residences. You and I cannot do that. It would be flagged quickly. If it was not flagged, you can bet we would hear about it eventually. Technically, it is a federal crime.

How common is it? We don’t know, but most people would never attempt such a thing, knowing they face potentially serious trouble down the line, perhaps even forced foreclosure.

We have no idea about Cook’s intentions. Was it an accident that she listed two primary residences within two weeks of each other, one in Ann Arbor, Michigan, and one in Atlanta? Maybe, but there are potentially huge financial wins that come from doing so, if you can get away with it.

Banks give a better mortgage rate on the primary home, which is considered lower risk. You are also allowed to deduct interest on the primary. This one little trick of writing down two residences as primary could save hundreds of thousands of dollars in financial liability—if you can get away with it.

It seems overwhelmingly obvious that someone who attempts such a thing should not serve on the Federal Reserve board.

And yet we know that there is more going on. Trump has been very clear that he wants a big cut in interest rates. He has treated the Fed the way a borrower treats a lender, demanding the lowest interest rate possible. Right now, the payments on U.S. debt are very high and are busting the U.S. budget.

Trump wants lower rates on U.S.-issued debt. And he wants lower rates to help spur economic growth. There is grave danger associated with such a policy. Rates are already very low in real terms, and lower rates certainly mean higher inflation over the long term. That is a risk that Trump cannot afford to take right now.

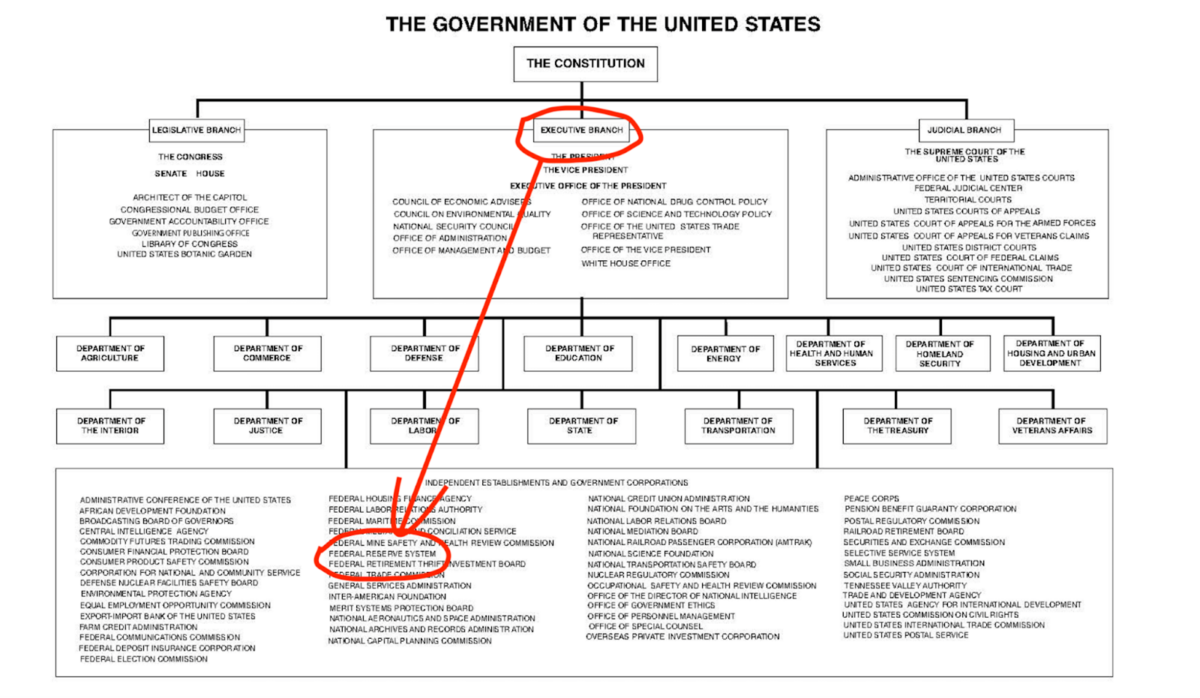

That said, this move has profound implications. Since the Fed was founded in 1913, it’s been uncertain precisely who is in charge of it. It is privately owned but serves at the pleasure of the government. The website of the Fed itself is a dot gov website.

The Fed and many other agencies are called “independent agencies.” You can scour the U.S. Constitution all day and find no such thing. It’s true that Congress created them, but they all live under the executive branch. If you try to make sense of this, you will come up with nothing. There have been few, if any, serious court attempts to adjudicate their existence and make sense of them in light of the words and structure of the law. They are just there, mostly unquestioned.

For more than 100 years, these agencies have ballooned in size and power. It’s called the administrative state—a state within a state. How this fits with republican-style government under the people has never been clear. No one I know can give a standing-on-one-foot defense of this system.

The Supreme Court has indirectly addressed the question some half a dozen times over the course of the century. In each case, it has sided with the agency over the president. But here’s the thing. The latest rulings from the Supreme Court have made it very clear that the court has every intention to reverse that precedent, based on the words of the Constitution itself.

It’s one thing to rule concerning the Department of Labor or some other regulatory body. But ruling on who controls the Federal Reserve is another matter entirely. The Fed is the nation’s printing press of money. It is what makes possible the gigantic debt, funds the welfare state and wars, keeps the financial system liquid, and generally works to make big government possible.

Long before the Fed, there were many efforts in the 19th century to create a national bank—a bank that serves the government. It was established and then abolished. President Andrew Jackson was most famous for his war against the national bank. He won it. He was a thorough-going populist and probably serves as the best ideological precedent for Trump’s second term in office.

In other words, Trump has picked a soft target to go after, one that has never previously been hit by a U.S. president. This battle is necessary. It had to happen at some point. The Federal Reserve was created in 1913 with no clear basis in law, and the results have been disastrous for the country. One need only look at how poorly it has protected the value of the dollar.

One must hope that this presidential intervention does not make a bad system worse, as The Wall Street Journal predicts. Pressing the central bank for more credit expansion is a dangerous way to generate prosperity. A highly politicized Fed could be worse than a seemingly independent one.

That said, something has to be done to bring a modicum of public accountability to the centralized system of banking and finance. In the context of American history and law, this is the way.