The bid-ask spread in the housing market persists. Over the past several years, home sellers have become accustomed to double-digit percentage price increases annually, going under contract within a week, and—very often—fielding competing offers above list price.

Still a Seller’s Market

According to a Realtor.com report, delistings are up by 47 percent nationwide in May from a year earlier and up by 35 percent year to date over the same period last year.Clearly, there is no pressure for sellers to sell. Most have mortgages that carry interest rates at half the level prevailing today. The prospect of paying 7 percent on their next home mortgage when they’re paying 3.5 percent today does little to motivate sellers. By the same token, most of them are sitting on huge amounts of home equity built up over the course of the last several years, as asset price inflation has raged. There is little threat of falling prices putting them underwater and thus no sense of urgency to sell at prices they don’t like.

Most analysts have argued that the deluge of delistings indicates seller frustration, but this is misleading. Combine the previously described dynamic with the fact that median list prices have essentially stayed the same since 2023, and it’s clear that sellers remain in control of this market.

Downstream Effects

The inability of a market—in this case the housing market—to clear is a sign of dysfunction. And this dysfunction has obvious origins and reasons. The zero-interest-rate policy (ZIRP) era lasted from roughly 2008 to 2022, hitting its zenith in December 2020 when $18.4 trillion in bonds worldwide offered negative yields. The impact of such an aggressively ignorant policy, especially on individual Americans, can’t be understated.

For starters, driving down interest rates is inflationary by definition. New money is created ex nihilo by the central bank. That new money is used to purchase securities from commercial banks (and sometimes indirectly from non-bank entities), thus expanding credit and loanable funds. This brute force method of reducing interest rates, driven by inflation of the money supply, is also price-inflationary. Over the past 15 years, that price inflation has been especially prevalent in capital markets, including the housing market.

As asset prices climbed and interest rates remained low, only those with significant asset exposure were able to see appreciation in their net worth and standard of living at a pace that approximated overall price inflation. Those without such exposure, to the extent they had any savings at all, were left to stow away cash in CDs and other instruments yielding next to nothing on a nominal basis and negative rates in real terms.

The result, as it pertains to housing, is a massively bifurcated market where—increasingly—only the old and wealthy can afford to participate. So what we appear to have now is a housing market where the old and wealthy are simply selling to others within their cohort.

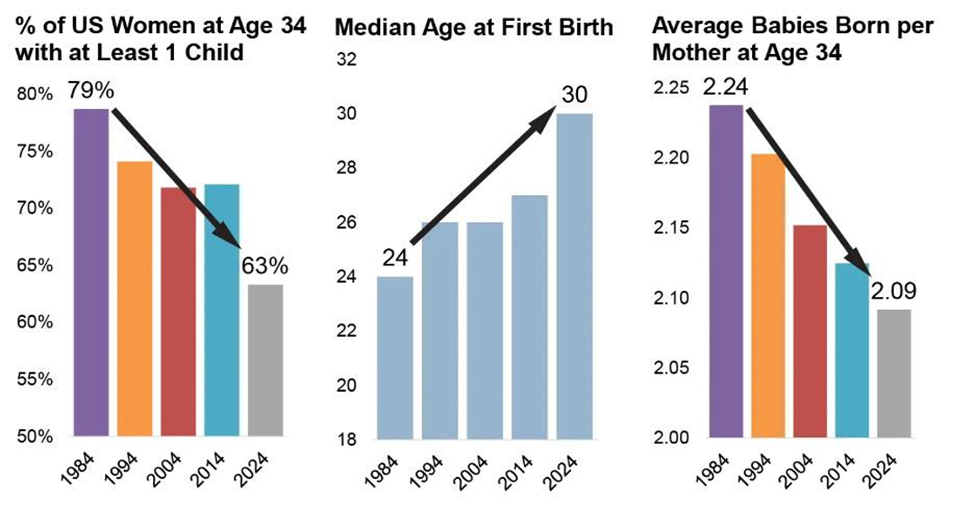

The aforementioned dynamics in the homeownership market are not limited to financial analysis—they have an impact on the life path of the individual American. To wit, the average age of first-time homebuyers is now at an all-time high of 38, while the average age of all buyers is also at an all-time high of 56. As the younger, necessarily less wealthy, are crowded out of the housing market, family formation is delayed. The data support this.

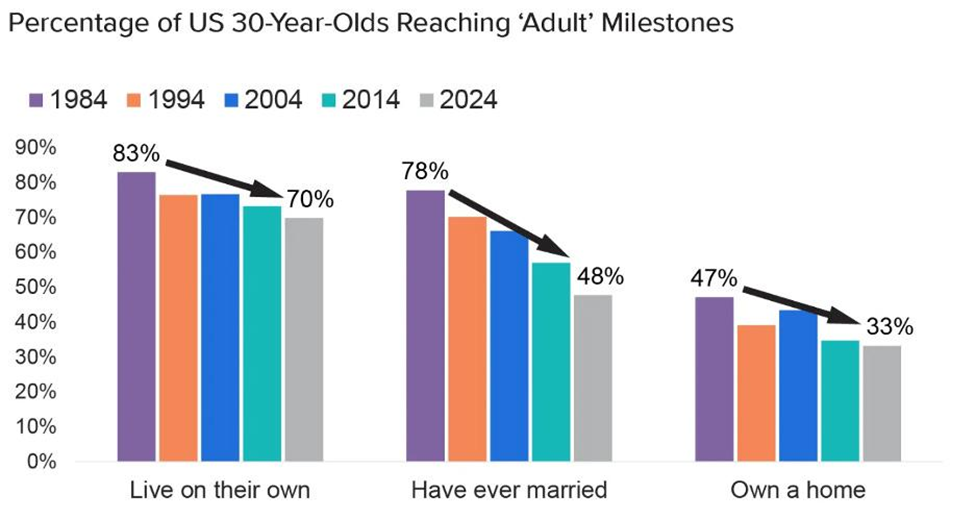

Along the same lines, today’s average 30-year-olds continue a trend of “delayed adulthood” by many measures. Only 70 percent live on their own, only 48 percent have ever married, and only 33 percent own a home.

Nefarious Causes

Monetary inflation—pushed by the central bank and supported by the administration—is not simply an inefficient way to allocate resources. Rather, it is a pernicious curse unlike any other in scope and magnitude. From pointless wars that kill millions to the productive retardation of entire generations, monetary inflation enables a spectrum of evils hard to imagine in its absence.That successive administrations have not recognized this is no coincidence, as the ability to print money is the ultimate weapon of the state—that which makes all others possible. Riding on the success and credibility of our more free-market past—and the prosperity it created—we are now amortizing that credibility quickly. Impossibly expensive homes are simply one item among the laundry list of ill effects.