This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

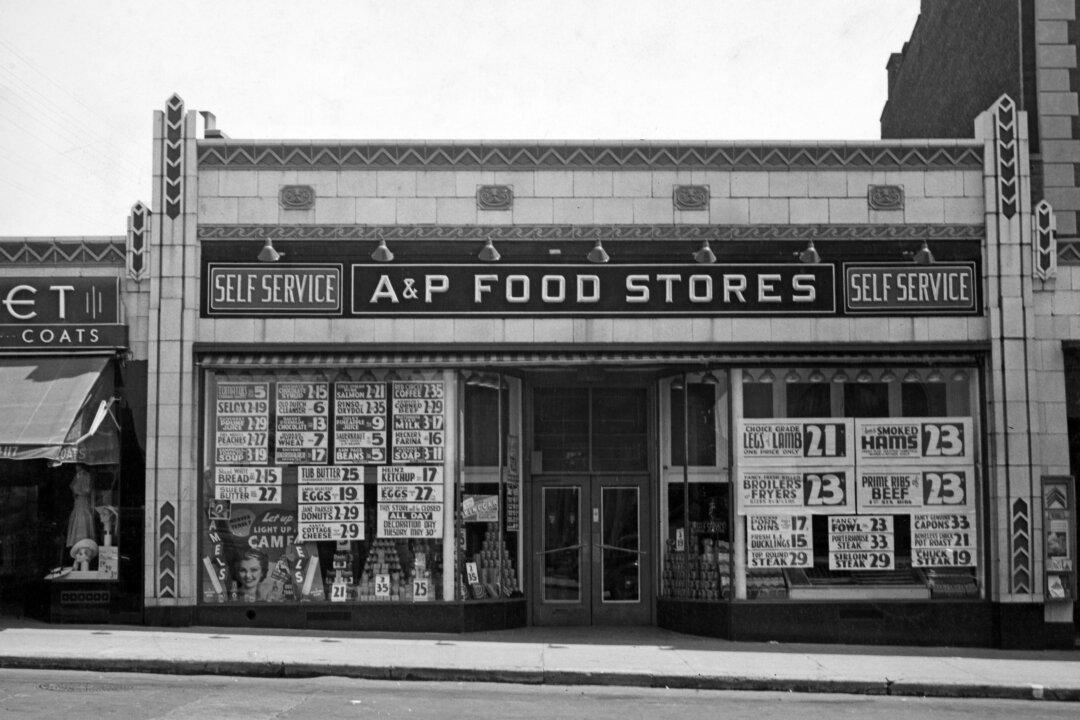

Federal Reserve Board Chairman Jerome Powell speaks during a news conference following the Federal Open Market Committee meeting at the Federal Reserve in Washington on June 14, 2023. Mandel Ngan/AFP via Getty Images

The Federal Open Market Committee’s unanimous decision on Wednesday not to raise the federal funds rate, which banks charge each other for overnight loans, has champagne corks popping in some quarters, where it is hailed as evidence of the long-in-coming conquest of inflation; while others see Federal Reserve Chairman Jerome Powell turning chicken in the face of a long-term price problem that needed far more drastic, sustained measures than ten consecutive months of Fed funds rate increases totaling 500 basis points.

The Consumer Price Index may have dropped every month for almost a year now, sinking to its current 4 percent. But core inflation—which excludes the volatile, and therefore sometimes misleading, categories of food and gasoline—rose another 0.4 percent in May, as it has on average during the preceding months of this year. It remains at a year-over-year high of 5.3 percent. Both that and the 4 percent CPI are far above the Fed’s target of 2 percent inflation.

Until President Joe Biden’s arrival in the White House nearly two and a half years ago, inflation of any consequence was unknown in America for decades. In the 1980s, Fed Chairman Paul Volcker wrenched the curse of persistent high inflation out of the economy, and President Ronald Reagan, while providing Volcker with all-important political cover by withholding any real criticism of the Fed, immediately ended the long-standing price controls on domestic oil within weeks of his taking office—an intrusion by government that had been diverting global supply and causing lines of cars at gas stations. Reagan also demonstrated that Big Labor’s power was on the wane by firing illegally striking federal air-traffic controllers. And his massive 25 percent income tax rate cuts, attacked at the time by establishment economists as inflationary, proved that allowing Americans to keep more of their wealth does not aggravate prices.

The Reagan-Volcker low-inflation legacy withstood a lot over three-plus decades but it has not been able to take the punch of Biden’s and ever-more-radicalized congressional Democrats’ spending spree. He and a Congress controlled by his own party set in motion well over $3 trillion in additional spending, while the Fed, fearing COVID-spurred economic collapse, deployed its prodigious lending powers “to an unprecedented extent … forcefully, proactively, and aggressively” in response to COVID, buying hundreds of billions of dollars in Treasury securities and mortgage-backed securities guaranteed by the federal government.

Since the beginning of last summer, the Fed has shifted gears violently from its previous strategy of excessively loose policy. But the upshot in light of the Fed’s Wednesday action, absurdly characterized as a “hawkish pause,” is that inflation is far from cured, and the economy can’t depend on long-term Volckeresque help from Jay Powell. His comments on Wednesday, that not a single FOMC member supported easing at any time in 2023 and that there would two more Fed funds increases later in the year, amount to touting the strength of the aspirin being prescribed for a debilitating illness.

And for what? There is no avoiding economic downturn. Not only does the Conference Board forecast three quarters of negative GDP on the horizon, but simultaneously, “Asian economies are expected to drive most of global growth in 2023, as they benefit from ongoing reopening dynamics and less intense inflationary pressures compared to other regions.”

In the wake of the federal government handing out spending money to employees rendered idle by the lockdowns, credit card debt now actually stands at a higher level than before COVID—nearly $988 billion. Meanwhile, the Consumer Financial Protection Bureau is going to force credit card lenders to increase rates, and yank away some customers’ credit by regulating new restrictions on the ability to charge late fees—which are a disincentive to the over-extending of credit card use.

Then, there is the federal government’s own taxpayer-financed credit card. The Congressional Budget Office determines that Social Security spending will overtake revenues to the program in less than a decade, in 2033, while the same fate awaits Medicare.

Indeed, Powell admitted once again on Wednesday that the country is on an “unsustainable fiscal path.” But Biden’s glee earlier this year in attacking Sen. Rick Scott, the Florida Republican, for proposing a universal five-year sunset on federal spending legislation, including entitlements, points to the Democrats’ wish to wait and wait until the last possible minute before reducing Social Security and Medicare benefits on their terms, i.e. paired with tax increases that will bring the private sector job environment more in line with socialist-leaning Europe.

Recession is not the only trouble ahead for the private sector. Far under the radar is deep blue New York State’s ongoing crusade against business—with national consequences—under the assumption that the 10 percent of the nation’s Fortune 500 companies based in New York will put up with anything the state and city governments can throw at them, rather than relocate to somewhere where you can’t find a good bagel or with inadequate museum and theatre life.

Under the pretense of fighting monopolies, the State Senate has passed a bill that would slap corporations with a fine of as much as $100 million for, truth be told, simply being too successful. A State Assembly committee is now examining the proposed law. Both chambers are dominated by left-wing Democrats.

In its twisted, anti-free market thinking, the legislation considers a company that controls only 40 percent of the market to be a monopoly. New York State already suffers from the highest combined income tax rate in America, and even has the shameful distinction of being the only state to have increased income taxes during the COVID lockdowns. If there is a sizable exodus from the Empire State of major businesses in the financial and other sectors, it could mean the forced geographical upheaval of this country’s financial establishment, with unpredictable impacts.

Underlying all of this—from a long too-powerful Fed incapable of managing inflation properly to spending-induced inflation, to the political hazards of fixing entitlements, to the left’s unquenchable hatred of the private sector—can be found apparent immoral governmental overreach.

Exposing the ubiquitous, poisonous tentacles of the state wouldn’t make a bad theme for a presidential candidacy.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times.