The Federal Reserve last year lost $114 billion on its portfolio, something that has never happened in the history of this institution. People hear this and are completely confused by what it could mean. After all, if we know anything about the Fed, it’s that it has the power to print money out of thin air.

Why would the Fed have to bear losses at all?

It is very weird, to be sure. But the reason traces to the completely insane finance that was kicked off with the COVID-19 response. The Fed was there to make possible many trillions in new spending and stimulus. But because of the way the Fed operates like a quasi-bank, it still has a balance sheet with assets (from which it earns money) and liabilities (from which it pays money).

Things are so out of whack at the Fed today that it’s losing money hand over fist. You could observe that the whole system of accounting is an illusion, and maybe that’s right. But the reality still has consequences.

Let’s see how this whole shell game works.

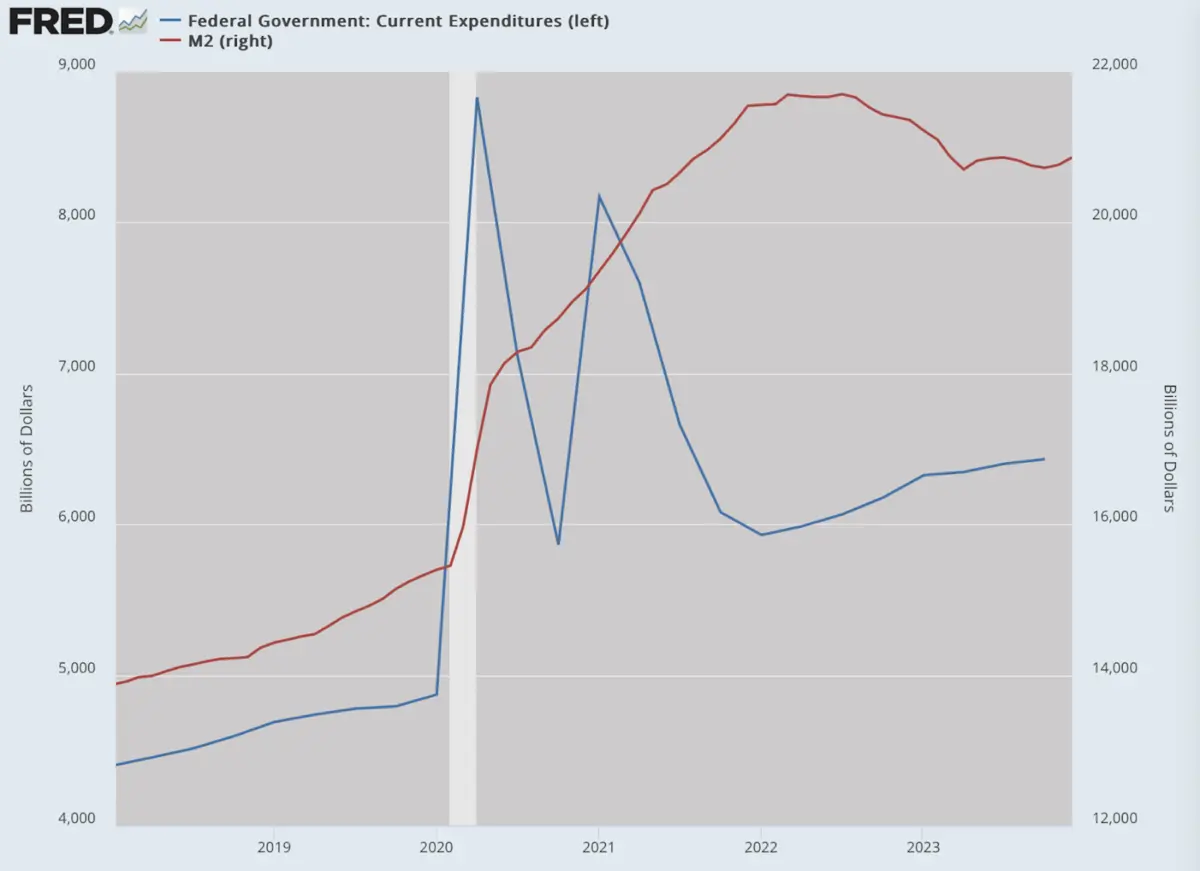

The supposed crisis came in 2020 and Congress was called upon multiple times to authorize many trillions in new spending.

They did it with the stroke of a pen, like stoners buying things at the mall without a thought as to how the bill would be paid.

The U.S. Treasury acts as a bookkeeper. It notices that the money isn’t there to spend, but it responds to what Congress and the president order. So spend it does, while creating new debt called Treasury bills.

The Treasury, of course, turned to its trusted friend the Fed to be the buyer through its preferred intermediaries. The Fed complied and bought many trillions in new debt, sending the cash to the sellers and thus enabling the helicopter spending.

Where did the Fed get the money? That’s where the magic comes in: It comes from computer entries. That’s why we have a central bank. It makes scarcity of resources disappear when it matters enough to the government.

The Fed was now the owner of the debt, which it distributed far and wide through agreements and transactions with the banking system it regulates. This process is what generated inflation: vast sums of new cash awash in the economy and injected straight into general circulation through stimulus payments and other subsidies.

This worked for a while until the Fed started panicking about the resulting inflation. Here, two years into high inflation, is when the Fed raised the interest rates that it charged member banks. These rate increases cascaded throughout the yield curve, causing huge increases in everything from long-dated bonds to mortgage rates to credit-card debt.

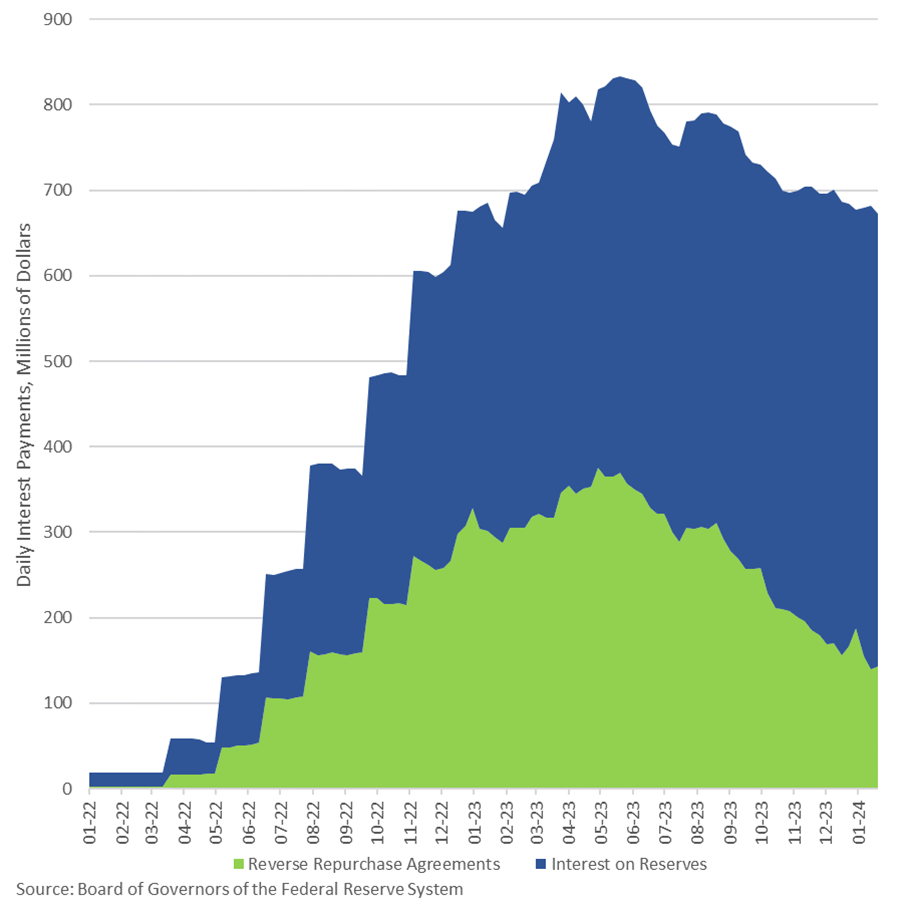

As part of this process to rein in money expansion, the Fed resorted to an old trick it tried in 2008. It started paying higher rates to banks to park their money at the Fed, thus sterilizing the money. It was an attempt to sponge up the liquidity that it had created.

But then, the Fed had a serious problem. It still had to pay high rates on that cash held in the form of debt because all this slush was on the liability side of its balance sheet. After all, these are the Fed’s bonds.

That’s when the outgoing expenses started far outpacing the incoming revenue from its portfolio. The losses are mounting due to the timing of the emergency measures in two directions: first from acting as the purchaser and then owner of vast government debt and then ending up holding the bag as it raised rates to curb money flows.

There is no easy way out of this pickle. One irony here is that when the Fed makes money, it sends it to the Treasury Department. That revenue flow to the government has come to an end, as the Fed’s payments are going to bondholders, which are mostly banks and financial institutions. (The Treasury is trying to make up the difference with more vigorous tax collection.)

For this reason, there is a case for doubt that we are done with the chaos caused by the Fed’s actions since 2020. Yes, we’ve experienced inflation that robbed the dollar of 20 cents or more of purchasing power. But that alone does not deal with the full issue. Plenty of spare cash is still rattling around the banking and financial system and it is landing in financials.

The S&P is setting new records, but you surely did not believe the Biden line that this reflects new productivity and prosperity. More likely, this is exuberance born of loose money. There is also the problem of the Fed’s balance sheet, which still needs to move in the opposite direction with more assets than liabilities.

There is the matter of timing to deal with also. There is an election coming up. The Fed is already under pressure to backtrack on its quantitative tightening and even push some helpful rate cuts between now and then.

That could involve generating more in the way of credit expansion, which in turn threatens to repeat the experience of the 1970s. Back then, just when the Fed thought it was safe to serve the political class again with low rates, it inspired an inflationary bout worse than what came before.

The instant that the Fed stops paying banks to park reserves in its vaults, eventual hell could be unleashed for whomever the new U.S. president is. But if it does not take this course, the losses will mount without end.

Isn’t monetary policy such a blessing! It’s fun to think of an alternative universe in which government functioned like the normal American household or any state government, spending what it can pay for or borrowing in the markets while facing a normal default premium like every other debt issuer. That, sadly, is not the world in which we live, thanks to the existence of this beast.