On July 12, financial markets were roiled by an early release of the Consumer Price Index that turned out to be a fake. It looked real, and markets were flooded with sellers because the number came in at 10.2 percent year over year. That would imply more extreme efforts by the Federal Reserve to crack down.

The Bureau of Economic Statistics said it was a fake and everyone calmed down. Can you believe anyone would make up or believe such a ridiculous report?

The real report, which was released on July 13, wasn’t that much different. The official inflation rate as measured by consumer prices—which are rising much more slowly than producer prices—is now 9.1 percent, the highest rate in 41 years. That caused immediate gasps all around, and nowhere as intensely as at the White House, where inflation is utterly wrecking this presidency which is polling at devastating low numbers.

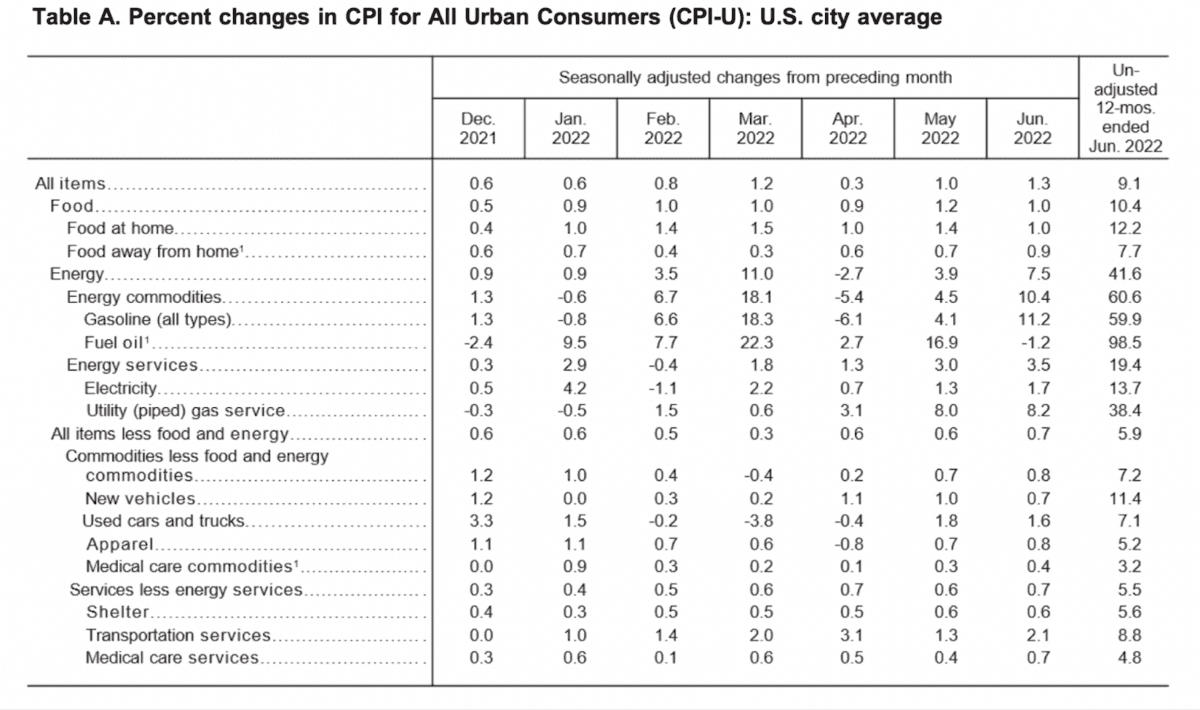

“The all items index increased 9.1 percent for the 12 months ending June, the largest 12-month increase since the period ending November 1981. The all items less food and energy index rose 5.9 percent over the last 12 months. The energy index rose 41.6 percent over the last year, the largest 12-month increase since the period ending April 1980. The food index increased 10.4 percent for the 12 months ending June, the largest 12-month increase since the period ending February 1981.”

Still, media reports attempted to downplay the disaster by assuring readers that things really have changed and that the next report will be much better. That’s because oil and gas are down. Economist Paul Krugman was first out with the “clarification,” saying that this is old news and no longer matters because energy is already correcting in the other direction. Oh, sure.

What people seem not to understand is that inflation of this sort is never even and linear. The forces of monetary devaluation spread out the economy in ways that no one can predict, hitting one sector for a time and then moving on. If we only focus on one set of changes, we are missing the bigger picture.

Here is the breakdown of how this index—which is a statistical fiction created as a mental tool but doesn’t actually exist in the real world—came to be, sector by sector. Here is where you find the evidence of the unfolding calamity that has roiled American life.

You can drill down into the numbers and find eye-popping data such as how fuel oil is up 98.5 percent year over year, and how utility prices are up 38.4 percent. Gasoline is up 59.9 percent year over year. How can these numbers be so grim and yet yield an overall number of 9.1 percent? You have to look at the low performers such as medical care commodities (3.2 percent) and non-energy services (5.5 percent). It all comes down to how the formula weighs the sectors.

Measures of real-time inflation for the better part of the year have estimated rates between 10 and 12 percent. So there should be nothing truly shocking in this official number. And yet the shock is there simply because the Bureau of Economic Statistics has now codified what everyone already knows: The purchasing power of the dollar is draining away fast.

The beauty of a figure that approaches 10 percent is that it makes it easy to figure out how much value your money is losing each year. It means that if you have a dollar in your wallet and keep it there for five years, it will be worth only two quarters in 2027. That puts a fine point on the robbery taking place right now. This devaluation affects all income, too, which has taken a hit even as families are spending down their savings and ramping up credit card debt.

Only a year and a half ago, many people felt a sense of comfort in their financial well-being. Savings were up, and income was secure. It seemed as if there was going to be no great price to pay for the lockdowns and $6 trillion in congressional spending covered entirely by Fed debt monetization. What could go wrong? Seemingly out of nowhere, debt and income trends flipped, putting a massive financial squeeze on the middle class and the poor especially.

![Real disposable income falling dramatically even as household debt service as a percent of disposable income is rising. (Data: Federal Reserve Economic Data [FRED], St. Louis Fed; Chart: Jeffrey A. Tucker)](/_next/image?url=https%3A%2F%2Fimg.theepochtimes.com%2Fassets%2Fuploads%2F2022%2F07%2F13%2F2-JAT-2022.07.13-1200x952.png&w=1200&q=75)

What is fascinating to watch is the effect of this on financial markets. They, too, appear to be getting back to reality, with the dawning realization that life since the summer of 2020 has been mostly an economic illusion. All the financial indexes seem to be headed back to a 2019 plateau, wiping out three years of earnings. That’s a notable correction by any standard of history.

It is easier to talk about what should not be done than it is to identify the fix. The Biden administration needs to stop pretending this is the fault of Russia’s Vladimir Putin. That claim has become an international joke. It’s also not the fault of gas-station owners, meat packers, grocers, real estate agents, landlords, dry cleaners, or electric companies. Inflation is affecting everyone in the same way that a rising tide clears out the sand castles we built. There is no way to stop it with artificial means once it begins.

The Fed can certainly raise rates, patch up its balance sheet by selling securities, and that’s all well and good, except for the recession that this also creates via the credit markets. We are going to see rising unemployment in high-end industries, with six-figure professionals suddenly finding themselves in a weak job market at their reservation wage. They will be forced to downgrade not only their spending but their social status, which is far more painful.

But, in the end, the only real solution to fix the carnage of inflation is economic growth. What causes that? Look back to the works of Adam Smith, who was wise enough to ask the great question of where wealth comes from. His answer: from well-functioning markets. That’s what needs to be unleashed from the government chains that are currently binding it.

The Biden administration doesn’t understand this. It will take no efforts to make this possible, barring some weird miracle or Pauline conversion.

Buckle up, folks! We have two more years of this growing damage to the American way of life. On the other side of all of this carnage, let’s all hope that we gain a new appreciation of the capacity of a free people to manage their own lives and rebuild the progress and hope that we once had.