This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

This morning’s jobs numbers surprised the bond market, printing at 199,000 new jobs, slightly above the consensus market expectations of 180,000. Revisions were revised down by 35,000 jobs. Government added another 49,000 jobs, all of them at the state and local level, that are included in the 199,000 number. The Household Survey, which is which is a poll to estimate the number of people employed, as opposed to the number of jobs created, and which is determined separately, estimated 180,000 new jobs were created.

The unemployment rate ticked down to 3.7 percent, down from last month’s 3.9 percent, but up slightly from the 3.6 percent of November 2022. Among the unemployed, 2,145,000 have remained unemployed for 15 weeks or more.

The labor force-participation rate increased slightly, to 62.8 percent from 62.7 percent.

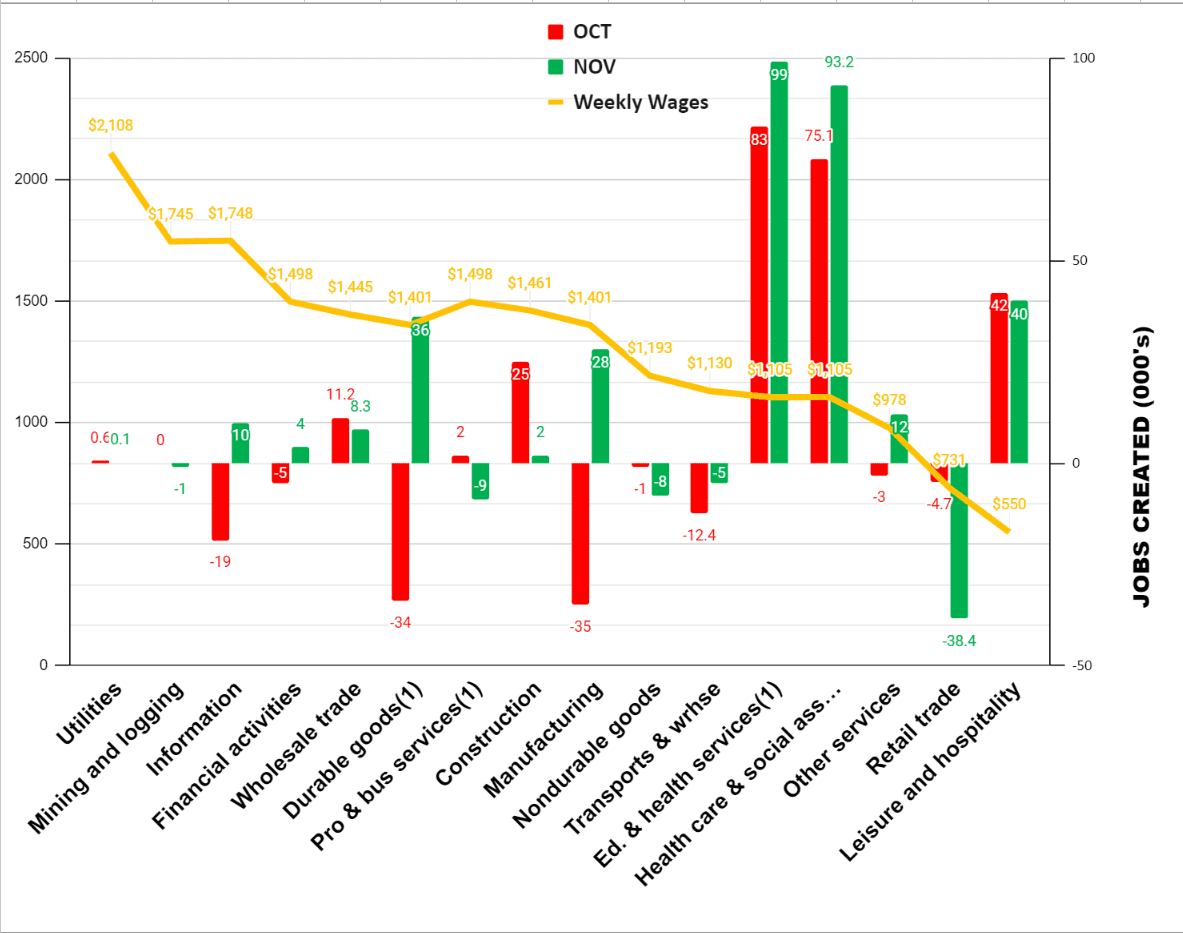

Let’s look at our exclusive schedule of November Jobs by Average Weekly Wages:

Source: Schedule of November Jobs Creation by Average Weekly Wages from BLS data / The Stuyvesant Square Consultancy

Once again, we’re seeing the overwhelming number of jobs created in the educational and health services sector (which includes health care and social assistance, but that is shown here separately). As we have pointed out previously, these are sectors that receive much of their revenue from government in the form of school taxes, college loans, MediCare and MedicAid, so they are not necessarily reflective of the strength of the overall productive goods and services economy. (Government employment is not otherwise shown in the chart for the same reason.)

Surprisingly, going into the busy Christmas and Hanukkah season, November jobs showed more than 38,000 jobs were lost in the retail trade. Manufacturing jobs replaced jobs lost last month in both durable goods and non-durable goods, partly due to the United Auto Workers strike being settled and other factors, presumably including a better outlook for the economy than had been expected earlier in the Autumn.

Opinion and Outlook

The bond market had been anticipating that the Federal Reserve would reduce rates on a slowing economy. This morning’s better-than-expected number left the bond market mostly bereft of a firm direction of further Fed actions. It was a “Goldilocks” number, insofar as they were concerned; however, by 10:00 a.m., bonds were trading up (and thus yields were lower) on the two-, 10-, and 30-year bonds, implying the market thinks the Fed is unlikely to cut rates as soon as it had previously anticipated. The prior view was mostly sanguine anyway, given that Fed officials had warned, repeatedly, that they were unlikely to cut rates as quickly as the market had thought. Gold prices also fell from record highs on this morning’s jobs news as the market anticipated a stronger-than-expected economic future.

The national debt continues to grow, unabated, and may possibly cross the $34 trillion threshold by the end of the year. Congress does not seem to have much concern, given that it will adjourn for the Christmas recess after Dec. 14 and only return the second week of January. That is surprising—one might say irresponsible—given that the current continuing resolution (CR) expires on Jan. 19. We see it more than likely that the GOP House will, again, cede to yet another CR, particularly given that its majority will be down by the expulsion of Rep. George Santos (R-N.Y.) and the resignation of Rep. Kevin McCarthy (R-Calif.). That will likely weigh poorly for the future of House Speaker Mike Johnson (R-La.) and for incumbent House Republicans in the 2024 election, as the deficits, debt, and spending were major talking points of the GOP since it took control. Many incumbent Republicans may find themselves facing a GOP primary failing a rapid turnabout of the party priorities.

If the CR is extended and nothing is done to arrest spending, deficits, and the debt, there is a risk that long-term interest rates—which are largely beyond the Fed’s control, absent the rare and radical step of yield-curve control—could increase significantly to ensure government bond sales clear. Debt is already at 120 percent of U.S. GDP, 15 percentage points higher than the already outrageous prior debt-to-GDP ratio of 105 percent that existed before the pandemic. (And we are now at least a year beyond it!)

Losing control of interest rates to a circumspect market—one that thinks the dollars will be repaid with will be worth substantially less than those the lender has lent—creates the kind of inflation that, once unleashed, becomes unrecoverable. It will cause less money to be received for each bond sale as bonds are discounted in the market, meaning that more bonds have to be issued to make up the difference and meet anticipated needs. But that means more money will need to be paid to pay off all the bonds when they come due. That means either higher taxes—at risk of recession—or higher inflation as the dollar loses its value from more “printing.” Absent some massive increase in productivity unseen since World War II, it is the road to perdition and economic disaster.

Summary

I expect inflation to tick up if there is an extension of the CR and for the economy to slow further as a consequence, mostly toward the end of the second quarter. The Fed will continue to hold rates “as is,” which will be a mistake, as inflation ticks up further, into the range of 3.5–4.0 percent. The current quarter, GDP will print at 2 percent or less, but then slink down to 1.5–2.0 percent in the first quarter of 2024 and to around 1 percent for 2024, if not recession, for the entirety of 2024. Much depends on the Congress, but I have considerable doubt it will act responsibly.

November’s Other Data Points

The Institute for Supply Management’s Manufacturer’s Purchasing Managers Index (PMI) for October showed the industrial economy is contracting at the same rate as last month, at 46.7. (A reading below 50 signals contraction.) It is the thirteenth consecutive month of contraction.

On the other hand, the ISM Services Index showed the service economy expanding, slightly more quickly, in an 11-month trend. The Job Openings and Labor Turnover Survey (JOLTS) for October, released Dec. 5, declined, with 617,000 fewer jobs openings in October than in September. Total separations increased by 51.

Building permits in October, released Nov. 17, were at a seasonally adjusted annual rate of 1,487,000. This is 1.1 percent below the revised September rate of 1,471,000, but is 4.4 percent below the October 2022 rate of 1,555,000.

Privately owned housing starts in October were at a seasonally adjusted annual rate of 1,372,000. This is 1.9 percent (±13.5 percent) above the revised September estimate of 1,346,000, but is 4.2 percent (±10.0 percent) below the October 2022 rate of 1,432,000.

For October, personal income and outlays, released Nov. 30, showed disposable personal income up 0.3 percent in current dollars and the same amount in chained 2017 dollars. (“Chained dollars” is a measure of inflation that takes into account changes in consumer behavior in response to changes in prices.) Personal income in current dollars was up 0.2 percent.

The August Personal Consumption Expenditures (PCE) Index from a year ago, excluding food and energy, released the same day, and reported to be the Federal Reserve’s preferred measure of inflation, printed at 3.5 percent. PCE inflation, also called “headline inflation,” printed at 3.0 percent.

The RCM/TIPP Economic Optimism Index (previously the IBD/TIPP Economic Optimism Index) fell 10.1 percent in December, to 40.0. The index has remained in negative territory for 28 consecutive months now.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times.

J.G. Collins is managing director of the Stuyvesant Square Consultancy, a strategic advisory, market survey, and consulting firm in New York. His writings on economics, trade, politics, and public policy have appeared in Forbes, the New York Post, Crain’s New York Business, The Hill, The American Conservative, and other publications.