As the Beijing regime’s actions clarify the thinking about its role in the world and expected behavior, we must reconsider what type of economic and financial relationship the United States and other countries should maintain with a hardened authoritarian state.

Can and should the United States decouple from China?

China hawks and doves cling to a misperception that the U.S. and Chinese economies maintain deep economic and financial interdependence. For example, many argue that China holds about $1 trillion in U.S. government debt and could cause broad disruptions. In reality, China holds only about 4 percent of outstanding U.S. debt securities, with the Federal Reserve ready to step in should China attempt to weaponize its holdings.

In keeping its financial markets closed for so long to foreign investors, China limited the portfolio investment such as stocks and business entanglements such as banks in mainland China. In reality, the financial entanglements remain minimal and manageable.

Economically, a more complicated picture emerges. Imports to the United States from China equal 2 percent of the U.S. gross domestic product (GDP), and exports from the United States to China represent 0.6 percent of the U.S. GDP—which now fall behind Mexico, as U.S. trade shifts closer to home. While small, the top-level numbers fail to capture the whole story. Most imports from China continue to fall into the basic manufacturing category, such as garments, machines, toys, and furniture, and a second category, basic electronics, such as iPhones and televisions. The type of trade matters for its ability to move around the world and the potential risk to the United States.

China sells itself as the workshop of the world, but, in reality, a lot of its exports can move to other countries for shipment to the United States with minimal disruption. For example, large amounts of garments, textiles, and basic manufacturing can shift with little or no disruption. Even if not shifted to other countries, this type of trade presents no significant risk to the United States.

Trade in electronics presents a more complicated problem. Some types of electronics manufacturing, such as iPhone assembly, can be moved to other countries without major disruptions. However, other types of electronics manufacturing, such as televisions, require more specialized buildings, inputs, and labor that require lead time, a transfer of knowledge, and infrastructure.

One other trade category needs to be mentioned: Chinese monopolies in key products, such as certain metals, minerals, and electrical vehicle batteries. China has spent vast sums to corner global markets in certain raw materials and finished products.

This presents a conundrum for the United States: The Chinese imports most easily shifted to other countries are generally the least critical from a risk perspective, but the riskiest imports are generally more complicated to shift to other countries.

So how can the U.S. government encourage and assist in decoupling high-risk Chinese products?

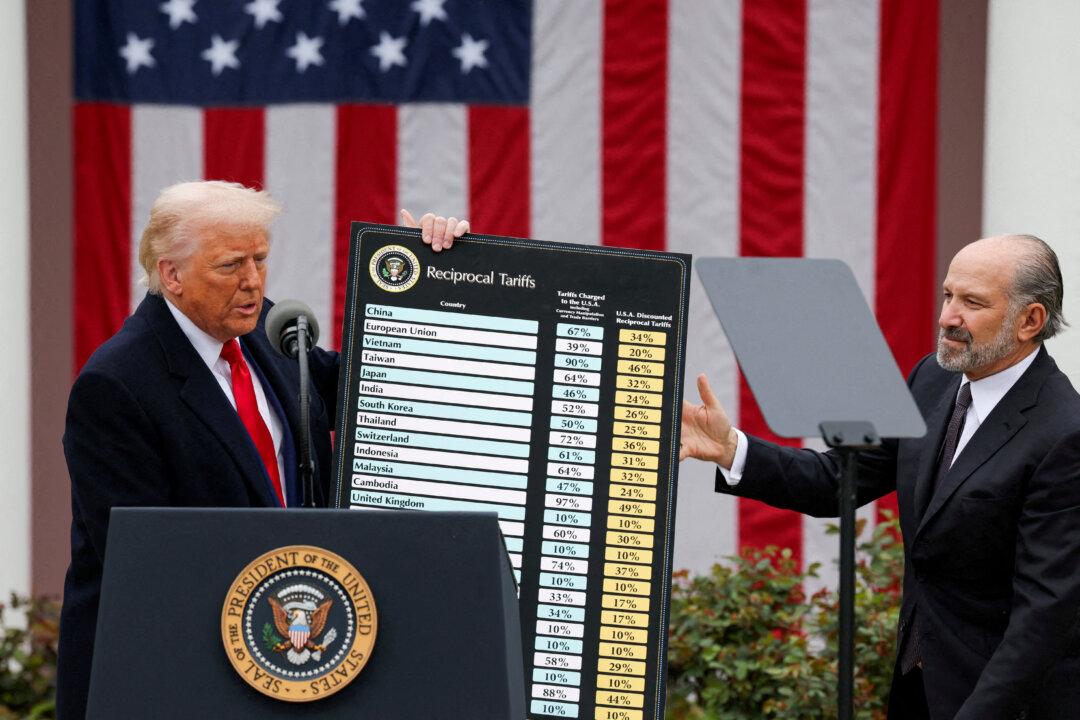

Tariffs are inefficient and encourage uncompetitive behavior, so they should be avoided. But in the case of China, tariffs help global producers to shift production. As a price signal, tariffs raise the price of goods from China, giving companies the time to move production and build new plants for those products. However, raising the price of products from China doesn’t go far enough to help shift supply chains away from high-risk suppliers.

There are a number of steps that the United States should take to encourage responsible decoupling away from China. Washington should actively work with countries and companies that want to leave China and those countries that wish to be the recipients of new investment. The primary fault of the United States—under both the Trump and Biden administrations—stems from the refusal to offer incentives to countries worried about China and companies working with China. The biggest complaint of Southeast Asian countries is the United States’ relative absence in the region or tangible offerings. At the same time that the United States works to help companies leave China, it can bring investment and jobs to other countries.

The United States should prioritize goods and industries that need decoupling and focus on how to achieve that objective. Decoupling shouldn’t imply a total cessation of all trade between the United States and China. Instead, it means or should mean decoupling high-risk products and shifting concentrated high-risk sectors to a greater range of producers. China holds a near-global monopoly in basic drug manufacturing, key metals and minerals, and certain electronics, placing the United States at serious risk for anything, from COVID-19 drug manufacturing to electronics inputs. Raising the price of Chinese-made products from these sectors only imposes losses on U.S. consumers if no other companies worldwide manufacture those products.

The United States has valid national security concerns about being overly reliant on a single adversarial country holding a near monopoly on basic drug production and electronics input. By working with companies and other countries, the United States can work to diversify its key supply chains away from an adversarial state that shows a willingness to use its monopoly power to impose pain on others. The United States has taken the first step to decouple—it must go further.