But there is an opportunity here with Trump’s nominee for Fed chair, Kevin Warsh. His first task will be navigating a hostile Senate. But should he be confirmed, Warsh’s time would be best spent cleaning up the Federal Reserve system: its personnel, spending, and data.

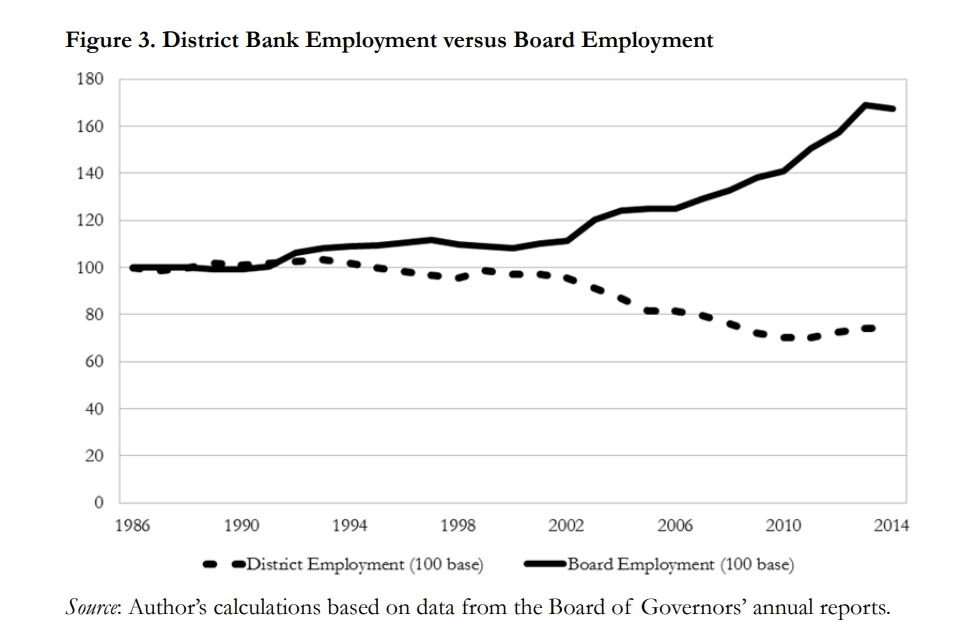

Does the Fed really need that many employees? After all, this isn’t the 1960s or 1970s when many things had to be done by hand. Not only have there been significant technological improvements and greater automation over the past 50 years, the development of artificial intelligence will also accelerate this trend. As such, the new Fed chair should reevaluate whether the Fed needs so many employees.

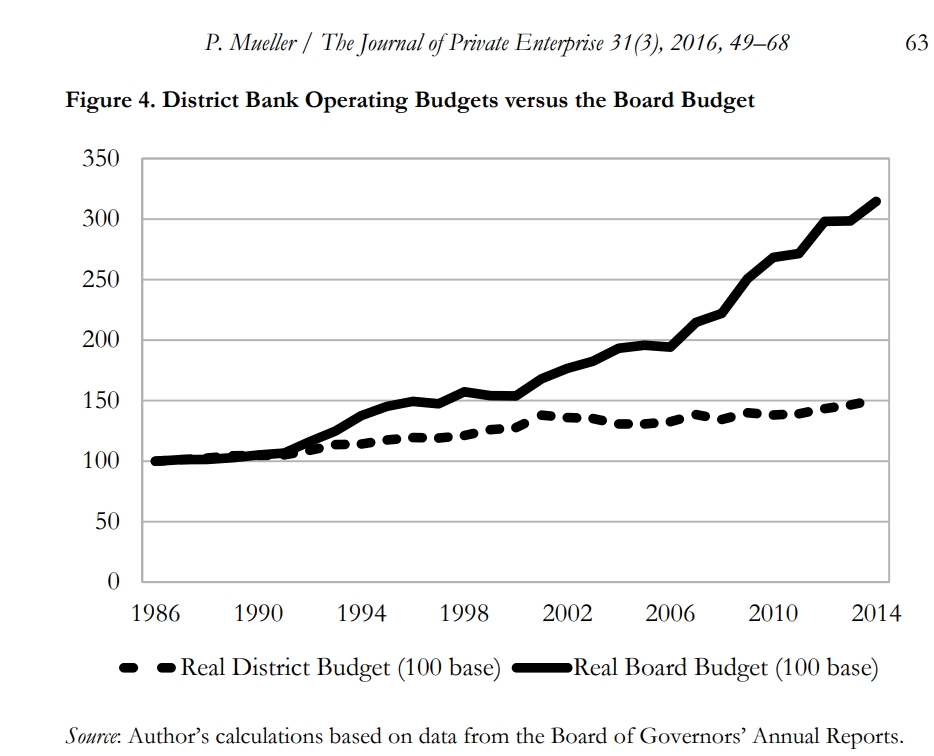

Along with reducing headcount through reorganization and consolidation, the Federal Reserve is ripe for an audit of its spending. Ron Paul popularized the idea of auditing the Fed in 2008. The Federal Reserve is unique in that it can literally create money, and in that it sets its budget independent of Congress. What would you expect the budget trend to be for a fully self-funding organization that can print money? If you said up and to the right, collect your prize.

The budget of the Board of Governors of the Fed has grown more consistently than the Federal budget for decades. In fact, why would any office or department at the Fed ever voluntarily reduce its spending? As such, we don’t see examples of significant retrenchment or budget cuts across the Board of Governors. District banks, on the other hand, operate with private-sector participation through their member-bank stockholders, yet they still suffer from bureaucratic bloat because of limited market competition.

By restructuring staff, streamlining operations, and auditing Fed spending, the new Fed chair can couch all of this change in terms of modernizing the institution. The Fed has largely failed to keep abreast of technological change when it comes to data, metrics, and execution. It still relies heavily on surveys and anecdotal conversations when it has access to millions of data points, nearly in real-time.

Consider the following key indicators that the Fed officials rely on:

Similarly, most of the key indicators that the Fed uses for assessing the strength of the labor market (the unemployment rate, nonfarm payrolls, labor force participation rate, and various measures of underemployment) tend to be released monthly as well.

The important measure of economic growth, the gross domestic product (GDP), comes out only quarterly—although there are frequent estimates. Furthermore, the measures of GDP tend to be revised often, too. The Atlanta Fed produces a “GDPNow” number—but it also relies primarily on estimates rather than real-time data. Indicators such as industrial production, retail sales, and business investment are not much better.

One area in which the Fed does make use of real-time data is in financial market conditions. Interest rates (e.g., federal funds rate, Treasury yields), credit spreads, and asset prices change in real time and can be used to assess financial stability and the effectiveness of monetary policy.

In addition to the delays, most of these core metrics, particularly GDP and the unemployment rate, are lagging indicators. They reflect past economic performance rather than provide real-time insights into current or future trends. In a rapidly evolving global economy, relying heavily on backward-looking data can lead to policy decisions that address emerging challenges too slowly or exacerbate existing ones.

The Federal Open Market Committee’s framework often emphasizes aggregate demand management, assuming that inflation is primarily a demand-side phenomenon. But recent economic shocks (supply chain disruptions, energy price spikes) highlight the critical role of supply-side factors. Over-reliance on demand-side metrics can lead to inappropriate policy responses.

In fact, many economists argue that the Fed should be less reactive in general. Economist Milton Friedman noted that there were “long and variable lags” between the implementation of monetary policy and its effects. Following predictable monetary rules will likely generate more stability and more growth in the long run.

Monetary policy (in terms of target interest rates) matters, but so does operational efficiency, utilization of technology, and access to good information. Institutional reform may also help the Fed rebuild public trust by reassuring people that its decisions reflect reality today rather than reality months ago—or not at all. Cleaning up the Federal Reserve will be a monumental task, but it will also be a legacy. Let’s hope that Warsh is up for the challenge.