Nearly everyone has a sense that something terrible threatens the nation, as if we haven’t seen or experienced the worst of it. I cannot dispute it. For several years, if not for a decade and a half or longer, we’ve been kicking the can down the road, patching up problems with debt and money printing, government spending and subsidies, or just generally eating the seed corn, as the old expression goes.

At some point, there will be a price to be paid.

Urban Office Space

Those who took office leases out in 2019 and before didn’t foresee the trends of our time. Inspired by the lockdown economy, vast numbers of workers are doing everything possible to avoid coming back to the office on a regular basis. They will show up sporadically only to make their faces shown, but otherwise, they are content with their at-home lifestyles.The labor shortage is giving them leverage over the bosses who are panicked about their long-leased office space now only half-full at best. When renewals come up next year and the next, these companies are going to be renegotiating for dramatic downsizing. That might be fine if it happens to a few companies in a large office structure, but when it happens all at once, for a space that is already highly leveraged, the result can be a full financial meltdown.

In 2008, we were introduced to the concept of a house being financially underwater: Its resale value is lower than the loan value of the property, which means that the mortgage holder is losing money with every payment. They would be better off selling the property and buying it again at the now much lower valuation. That led to the abandonment of millions of homes across the country.

What if that was just a warmup? What if we are witness to underwater skyscrapers and once-prestigious office spaces? What happens when the owners decide to permit bank repossession rather than continue to juggle mounting liabilities? What will that do to the banking system? We’ve never seen this, so the results have to be left to the imagination.

As for street-facing retail shops, their No. 1 problem is shrinkage due to rampant theft—a problem that no civilized city should face.

Inflation

Inflation data can be confusing. For years now, we’ve heard that it’s cooling, calming, relaxing, diminishing, and generally looking better because, after all, it is just transitory. And yet, the experience in our own lives is utterly grim. Part of this is the result of a fundamental mathematical confusion. This is a huge difference between rising less slowly and falling. And yet all reporting conflates those two.This would never make sense in a weight-loss program. If you put on 50 pounds in a month, and then gained only 30 and then 20 more in the subsequent months, is that good news or bad news? The terrible truth is that you are still headed toward disaster, albeit at a slower rate. That’s the summary of inflation in our time. There is no real good news. There is only less worse news.

There was a sense in 2021 that this whole problem would go away and we would soon relax back to 2019 prices, where we had been, more or less, for many years. Consumers have been slow to recognize that this truly is the new normal. We aren’t going back to the old days; we are only headed to the new days at variable rates.

Household finance is only now figuring out that every dollar has lost some 18 cents of value in a mere three years, which is a more substantial amount than people have typically saved even in the best of times. This means that inflation has robbed twice the average savings of the past, plus eaten into real income. The latest data on real household income have clocked the third year in a row of declines.

Low Savings

Here is an axiomated truth of economics: all prosperity grows from investment, which in turn comes from savings, which is made possible only by deferring consumption. No amount of Keynesian-style voodoo can refute that basic proposition. Investment requires savings, and savings require deferred consumption. Without it, we are getting poorer.All else equal, with historically fast increases in interest rates, you would expect two things: dramatic movement of funds into savings that are now paying a higher rate of return than financials, and also a diminution of debt that is too expensive to carry. Neither is happening. Why? Bluntly, there is no financial flexibility remaining in the system. Funds are already committed.

If you are carrying a car lease, a student loan, a mortgage, plus a personal loan, there is no automatic switch that allows you to go from paying debt service to saving money. It just isn’t possible. So it doesn’t matter what the incentives are if the funds are otherwise committed.

Just have a look at the huge increase in credit card debt. That makes no financial sense, but it’s the reality.

It’s the same with corporate debt. It took 30 years from 1980 to 2010 to go from $1 trillion to $6 trillion but only 10 more years to double to $12 trillion and another three to get to $14 trillion today. These companies took advantage of zero interest rates to change their business models, living off leverage as opposed to socking away gains for a rainy day.

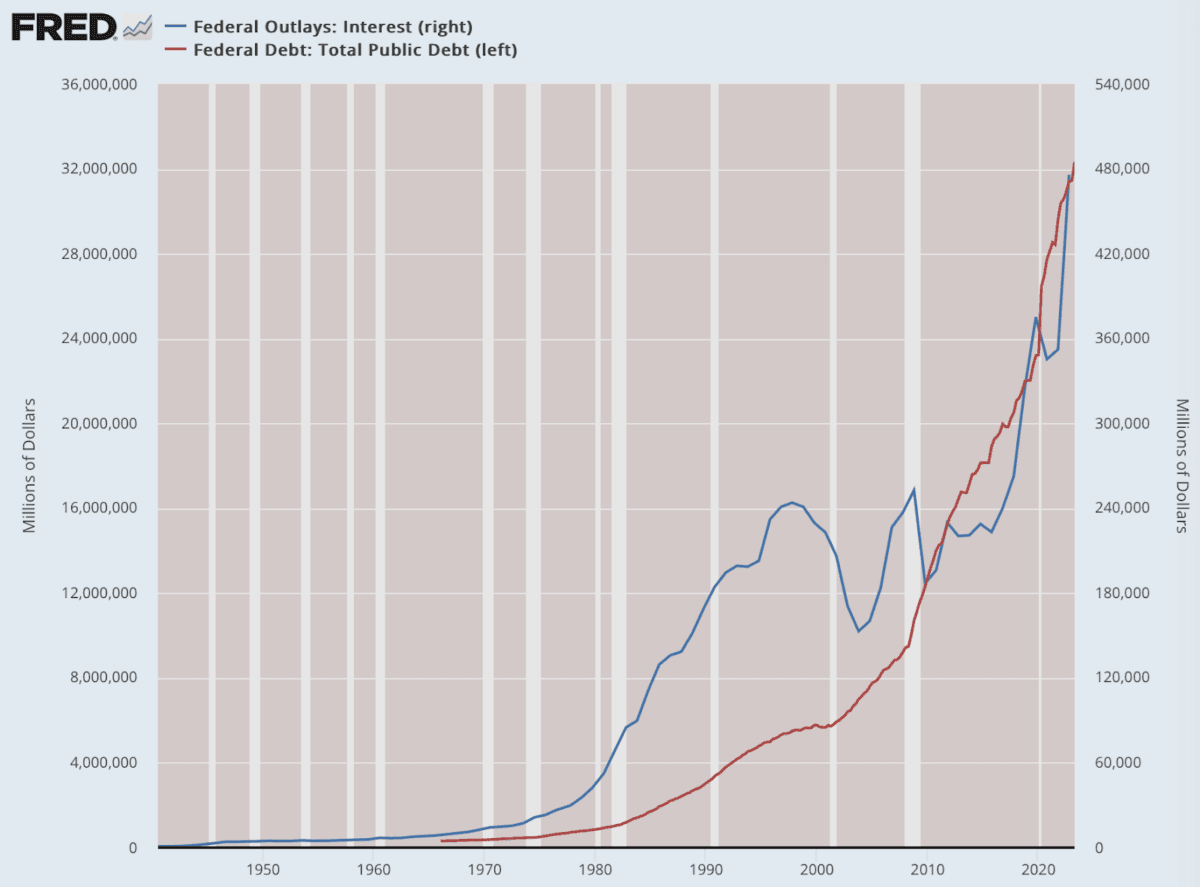

Fiscal Time Bomb

When the Federal Reserve embarked on a program of higher interest rates to crush inflation, everyone knew what this would mean to federal finance. It would blow up the expense of the U.S. Treasury on payments toward the debt. Did anyone really care? Not really.Sure enough, we are at a half-trillion dollars going to service the federal debt, and the rise is alarming. There is no magic money machine out there. All of these payments come from taxes or dollar depreciation in the form of inflation. On the back of this is the federal debt itself, the rise of which is beyond belief, as a half-trillion was recently added in a fortnight. Such numbers are truly beyond human comprehension.

Every bit of federal debt crowds out private investment. We’ve got vast amounts of capital going toward funding big government rather than new innovations and small businesses. And yet it is still not enough. Tax revenues are on the decline but the government has a plan for that too.

Prepare yourself, my friends: tax collection is going to get much more ferocious. There’s a reason why the IRS has hired tens of thousands of new agents. This size of government doesn’t come cheaply. Many people I know are experiencing all kinds of tangles today with the collection agents, many of which are actually private companies. This isn’t a kinder or gentler government. This is big government with teeth.

Financial Markets

The stock market has been taking many hits recently, and this is mostly because of the period of wake-up: Capital is moving to more secure bonds and out of stocks, the future of which is uncertain. Yields on the 10-year Treasury just spiked way more than anyone at the Fed planned, above levels in 2007, thus putting enormous pressure on capital markets.For a very long time, we’ve been able to rely on rising financials over the long term. It’s not clear whether that is going to be the reality for the next few years, as capital chases safety over speculation. What this means for a banking system holding vast amounts of debt priced under old terms is anyone’s guess.

With so much of U.S. wealth socked away in retirement accounts, this new reality is going to hit extremely hard. Indeed, a whole generation could panic about their financial future. Already, it’s nearly impossible for even a middle-class family with two incomes to make ends meet. They are already living paycheck to paycheck. Their only solace has been to look at rising digits in their brokerage accounts. What happens when that stops?

And what are people doing about it? They are spending like it is the end times: vacations, dinners out, clothes, and generally piling up debt.

Put all this together and you have only one conclusion: The United States as a nation is headed toward declining wealth and rising poverty. Such conditions bring out the worst in people, which has profound cultural consequences. Essentially, it means a much coarser and less generous people. Declining wealth calls forth the worst of human nature. It turns good people into savages.

Buckle up. It’s going to be a bumpy ride.