If the Chinese yuan devalues against the U.S. dollar, “officially” or otherwise, it could dramatically alter the economic status quo of the past two-plus decades and it will be for the worse.

Each of these currencies has been decimated – for a variety of reasons including political strife (Brazil, South Africa); economic sanctions (Russia); and India’s President Modi creating a “cashless society” two years ago.

In China’s case, the Yuan’s decline to levels not seen since before the 2008 crisis is principally due to the People’s Bank of China (PBOC) engaging the U.S. in a currency war - in direct response to Donald Trump’s escalation of the inevitable; and now, burgeoning; Sino-American trade war.

Trade War

Irrespective, the cumulative impact of the Yuan’s devaluation – fixed or loosely floating – was to create a massive trade surplus with the U.S. that was used to finance U.S. spending of Chinese goods via the purchase of more than $1 trillion of U.S. Treasury bonds. This artificially inflated both the U.S. and Chinese economies – but due to the massive amount of debt created by such manipulation, created economic imbalances that would need to be reversed.That day appears to have arrived, with the non-political politician Donald Trump providing the catalyst. He insists that the huge amount of jobs the weak Yuan has “stolen” be returned to America, via tariffs and other trade war tactics, designed to make it less profitable for Chinese companies to manufacture goods, compared to America. Which in turn, is causing the PBOC to officially – albeit, quietly – allowing the Yuan to decline anew.

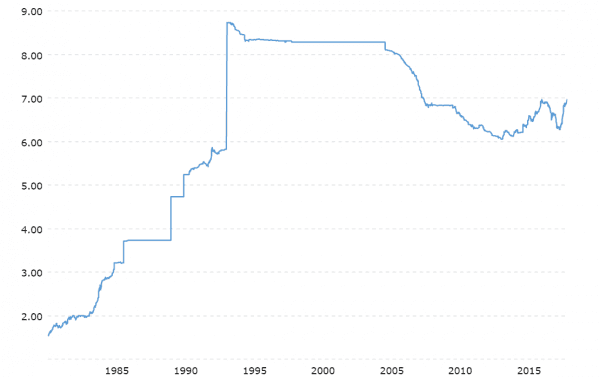

Now the Yuan is on the cusp of breaching the key psychological barrier of 7.0 to the dollar, a level not seen since April 2008, just before the worst financial crisis of our lifetimes. It’s not a coincidence the U.S. stock market has so dramatically declined in lockstep; not to mention, the Chinese stock market, and nearly all others.

Break Below 7

If it trades above 7.0, the ramifications will be massive; global; and for the most part, devastating – as it will be viewed as a political statement that the Chinese government intends to devalue the Yuan to counteract U.S. import tariffs; The same type of trade war tactics like the Smoot-Hawley Act of 1930, many blame the Great Depression on.This, in turn, will give the green light to all Central banks to (hyper)inflate their currencies. Fiat currency is a Ponzi scheme that must continue to grow, in order to survive. That is, until “bond vigilantes” call them out via much higher interest rates, as they have throughout history.

Yes, financial markets have shown a level of worry not seen in years; and yes, it has something to do with the rapid decline of “Emerging Market” currencies. However, given how little attention is being paid to this correlation – particularly, the Yuan/dollar’s inexorable decline toward 7.0; my guess is, that if (when) it occurs, it’s impact will be powerful, unpredictable, and dangerous. Few financial markets will benefit from such an event – with sound money alternatives like gold and Bitcoin to experience a huge capital inflow.