This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

Federal Reserve Chair Jerome Powell (L) speaks as President Joe Biden (R) listens during an announcement at the White House in Washington, on Nov. 22, 2021. Jim Watson/AFP via Getty Images

The October jobs report showed that the economy added 261,000 new jobs, considerably better than the consensus estimate of 200,000 jobs. This morning’s print is 54,000 fewer jobs than were created in September 2022 and 461,000 fewer jobs than were created in the COVID recovery period of 2021. Net revisions for August and September added another 29,000 net new jobs. (It is generally believed that 200,000–250,000 jobs are required to accommodate population growth.)

The jobs print, 25 percent-plus more than were expected, very likely sets up continued rate hikes from the Federal Open Market Committee, the policy-making arm of the Federal Reserve, until there is a tipping point that indicates inflation is on a clear glide path toward the Fed’s preferred target of 2 percent.

The unemployment rate was 3.7 percent, up 0.2 of a percentage points from September and down 0.9 of a percentage point from 4.6 percent in October of last year. The labor force participation rate was 62.2 percent, down from 62.3 percent that printed in September and up 50 basis points (bps) from October of last year, when it printed at 61.7. (A basis point is defined as 1/100th of a percentage point.)

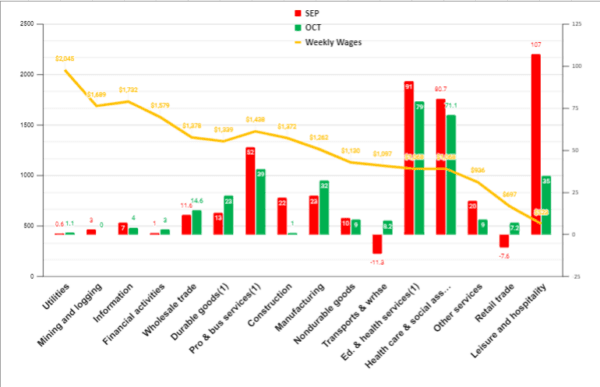

Bureau of Labor Statistics October Jobs by Weekly Wages by Major Sectors / Copyright 2022 The Stuyvesant Square Consultancy. All rights reserved

We are largely at the same level of jobs that we had prior to the pandemic, 153 million, but the jobs creation trajectory that would have occurred in that period is lost, likely permanently. The question now is whether, with a slowing economy and a Federal Reserve (Fed) tightening interest rates and reducing its balance sheet, the current trajectory can be maintained or whether the job creation will flatten or decline so as to arrest inflation. We anticipate it will be the latter.

The majority of jobs were, again, in lower-wage sectors, such as leisure and hospitality, and sectors that are largely government-supported, such as education and health services. That said, the higher-wage sector of professional and business services also showed strong jobs performance, at 46,000 jobs (albeit fewer than last month), with an average weekly wage of more than $1,400.

Real wages—which we define as annualized average weekly wages minus the 12-month average trimmed mean inflation rate for personal consumption expenditures, for September (the latest available data)—currently 4.74 percent, were mixed, with most sectors suffering real wage losses, as detailed in our quarterly chart of real annual year-over-year wages. (We report this data with the jobs reports that coincide with the end of each quarter.)

Other Data

Federal Reserve Policy

Quantitative tightening is always disruptive to markets, and doing so is always risky. Milton Friedman won the Nobel Prize in economics for proving that the Fed’s monetary tightening between the spring of 1928 through October 1929 was the proximate cause of the Crash of 1929 and the subsequent Great Depression. Former Fed Chair Ben Bernanke even admitted such in 2002. The Fed tightening of its balance sheet while simultaneously escalating its discount rate is not without risk.

Wall Street has mostly revised its view to match what we have been saying for some time: that the Fed would need to move the discount rate to a range of 3.5–5.0 percent to achieve its terminal rate, where inflation is contained to its 2 percent target.

In its statement Wednesday, the Fed also introduced a notion “cumulative tightening,” whereby the Fed acknowledged that its monetary policy takes some time to work its way through the economy:

“The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time. In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

While many read the comment as a dovish assertion by the Fed, and markets moved accordingly, their hopes were dashed within the hour when Fed Chair Jerome Powell said the risks of going too soft on inflation outweighed the risks of going too hard on inflation. In effect, Powell said the Fed can always loosen policy if it tightens too much, but if it doesn’t tighten enough, inflationary expectations can grow well out of control.

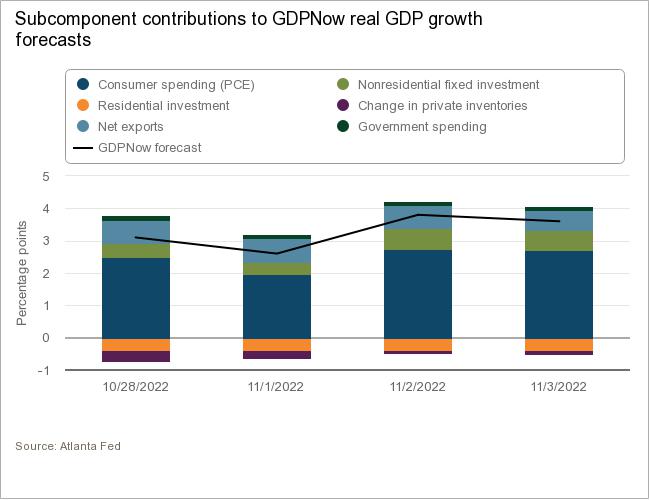

The Federal Reserve Bank of Atlanta is projecting fourth quarter 2022 to print at about 3.6 percent growth, well above the consensus range of -1.2 and +1.8 percent GDP growth. The more sanguine view of the Atlanta Fed continues to assume good consumer spending growth. We and others disagree.

We think the terminal rate will likely go to 5.5 percent, or even higher, if inflation from China’s anticipated reopening (see “Markets,” below), unless there is significant slowing in the Consumer Price Index within the next three quarters after this (i.e., fourth quarter 2022 to second quarter 2023). We are paying the price now of Powell dismissing inflation as “transitory” while others were issuing “hair on fire” warnings of inflation. The situation was exacerbated as the Biden administration and Congress forced more “recovery spending” when the recovery was already underway on its own.

Markets

We’re also seeing market risk in the mega-cap and tech space, as they move toward austerity in a slowing economy. Rideshare app Lyft (LYFT), for example, plans to lay off 13 percent of its workforce. Stripe and QualCom are doing the same. Amazon is pausing hiring. And, of course, Elon Musk is set to drop something like half of Twitter’s staff, though its more likely related to his takeover than macroeconomic effects.

As rumors of a China reopening abound (i.e., a relaxing of its zero-COVID rules), we’re also seeing increased prices in hard metals commodity prices and also oil futures. An increase in commodity prices will certainly raise producer prices, which, in turn, will wend their way through the broader economy around the first quarter of 2023. That would force an even higher terminal rate, as discussed above.

The jobs market is still exceedingly tight, and worse than we have seen in more than 20 years. The Beveridge Curve—which charts the job openings rate along the horizontal axis versus the unemployment rate along the horizontal axis, and in which the unemployment rate traditionally exceeds job openings—is printing at an extremely high rate because the job opening rate is virtually double the unemployment rate. That is unlikely to change anytime soon, absent the Fed creating a significant slowdown.

There are also market concerns with the rhetoric and posturing over the war in Ukraine. If, as Samuel Johnson wrote, nothing concentrates a man’s mind more if he knows he is about to be hanged, similarly nothing will focus the markets like the prospect of nuclear war. A sell-off could be triggered instantaneously if there is a “war or rumors of wars” involving nuclear weapons. As we discussed earlier this week, there is a less dramatic risk—but still challenging and possibly even more costly, both in lives and U.S. interests—if Russia weaponizes its food exports.

At this writing, the inversion of the two-year and 10-year Treasury yields is 56 basis points (bps), up from 40 bps in our September jobs report. We would have liked to see the Fed reduce its balance sheet sooner and more aggressively, as we have desired since last year. We now would be in a better place with less or no inversion. The Fed’s actions have been too little and too late, and, consequently, the U.S. economy will have to suffer longer-term inflation.

The Institute for Supply Management’s print of the Manufacturers Purchasing Managers’ Index, the Manufacturing PMI, registered growth, just barely, at 50.2 percent in October, down from 50.9 percent in September. The Institute’s Services PMIfor September showed growth at 54.4 percent, down slightly from September’s 56.7 percent, A reading above 50 signals growth.

The Job Openings and Labor Turnover Survey (JOLTS), released Tuesday, showed that the number and rate of job openings grew to 10,717,000 from last September’s 10,673,000 and grew by 4.3 percent from August’s 10,280,000. The growth in jobs opening is counter to the Fed’s wishes, and part of our reasoning that the Fed’s terminal rate could go as high at 6 percent.

Nonfarm business sector labor productivity increased just 0.3 percent. But from the same quarter a year ago, nonfarm business sector labor productivity decreased 1.4 percent. It is the first instance of three consecutive declines in this measure since 1982. As we noted in the June jobs report, first-quarter 2022 labor productivity dropped to its lowest level since 1947. As we have said previously, increasing productivity should be a public policy priority now because it will help trim inflation as well as curtail a recession.

Total business inventories remain ridiculously high, and the highest on record, a factor mentioned by many of the respondents in the ISM report.

Housing starts in September, released Oct. 19, were at a seasonally adjusted annual rate of 1,439,000. This is 8.1 percent below the August estimate of 1,566,000, and is 7.7 percent below the September 2021 rate of 1,559,000.

The IBD/TIPP Index of Economic Optimism for October printed at 41.6, down 6.9 points from September. (The index signals optimism at 50 or above.)

Commentary

The two quarters of decline in the first and second quarters of 2022 printed at a technical recession, which will need to be confirmed by the National Bureau of Economic Research Business Cycle Dating Committee. As we explained in our 2022 third-quarter GDP report, much of the “growth” was illusory from an anomaly with the data on imports and inventory.

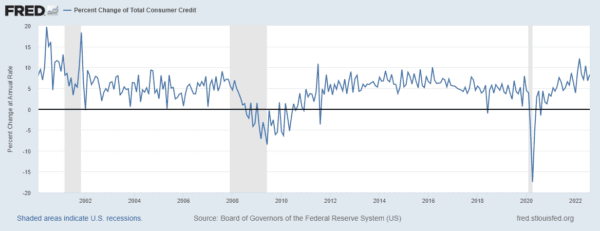

Household debt service as a percentage of disposable personal income was rising as of second quarter 2022, particularly consumer debt. As reported by the Federal Reserve Bank of New York: “Credit card balances saw their largest year-over-year percentage increase in more than 20 years, while aggregate limits on cards marked their largest increase in over 10 years.” This is to be expected in an inflationary economy, when wages fail to keep pace with higher prices and workers turn to their credit cards and consumer loans to maintain their lifestyles. We’re anxiously awaiting the third-quarter print.

As a consequence, we expect consumer spending to slow, as consumers—particularly those “living paycheck-to-paycheck”—are “tapped out” of available credit. With winter coming on, many people in northern climates will face a choice to “eat or heat” as energy prices—expected to be double what they were last year, in some areas—will hobble many family budgets. While the growth in consumer credit demand has reduced somewhat, the rate of growth of credit in March was the highest in 20 years. Even at the current rate of growth, it is still the highest since March, 2016. We suspect the reason the rate of growth has decreased is that banks and credit card issuers are tightening lending standards.

Percent change of total consumer credit, 2000 to August 2022 / Federal Reserve chart

Inflation continues to print at an unacceptable level, which will likely be exacerbated if rumors of China reopening prove true. Further, if the anticipated rail strike cannot be avoided, inflation will continue at a high level, notwithstanding tighter monetary policy.

We had said as recently as our September jobs report that we believed that real overnight rates will need to go to 3.5–5.0 percent, and stay there for at least three quarters, to thoroughly extinguish inflation and, more important, inflationary expectations. We now revise that discount rate to 5.5–6.5 percent. Despite the rapid increase in rates, today’s positive jobs print foretells continuing inflation above mid-single figures. We believe Wall Street is sanguine about the direction of rate increases. With full employment, we believe the Fed is cocked and loaded to knock down inflation (notwithstanding that policymakers will do so more slowly than we had hoped).

That said, we reiterate our long-standing call for the Fed to increase the limit of the Treasurys and mortgage-backed securities that it allows to “burn off,” up to at least $125 billion to reduce the Fed’s balance sheet more rapidly. This will signal Wall Street to de-leverage its own balance sheets accumulated during the zero and near-zero interest rate policies. This can be done in the next 12–18 months, but only if the Fed is compelled to act more rapidly by decreasing its own balance sheet.

While it will absolutely slow the economy more quickly, and even will likely cause a recession, it’s far better to incur sharp pain for a short period than anything similar to the lingering malaise the nation suffered after the financial crisis of 2008–09. (Think of pulling off a Band-aid in one quick motion as opposed to gradually pulling it off. Right now, the Fed is doing the latter.) The Fed’s failure to recognize that the inflation we saw at the end of last year was genuine, not “transitory,” has left it with only bad choices.

That said, and despite the Fed’s purported “independence,” we think it is far more likely that the board of governors would prefer to suffer lengthy malaise coming into the presidential election cycle over a sharp, short, recession that cuts into employment and retirement accounts and bankrupts marginal and over-leveraged businesses. Given a choice between recession and inflation—like a choice between castor oil or a sugary soft drink—the Fed governors will be tempted to the latter in a presidential election year or the run up to one. That’s another reason for instigating a quick, deep recession.

We believe fourth-quarter 2022 GDP will print in the neighborhood of 1 percent, plus or minus 50 bps. We are monitoring “gray swans” (i.e., events known and possible to happen, but assumed unlikely) in the Taiwan Straits, Ukraine, Europe, and U.S. elections, and will post information on those in our Twitter feed, @Stuysquare.

DISCLOSURE: The views expressed, including the outcome of future events, are the opinions of The Stuyvesant Square Consultancy and its management only as of November 4, 2022, and will not be revised for events after this document is submitted to The Epoch Times editors for publication. Statements herein do not represent, and should not be considered to be, investment advice. You should not use this article for that purpose. This article includes forward looking statements as to future events that may or may not develop as the writer opines. Before making any investment decision you should consult your own investment, business, legal, tax, and financial advisers. We associate with principals of TechnoMetrica on survey work in some elements of our business.

Note: Our economic and business commentaries most often tend to be event-driven. They are mostly written from a public policy, economic, or political/geopolitical perspective. Some are written from a management consulting perspective for companies that we believe to be under-performing and include strategies that we would recommend were the companies our clients.

J.G. Collins is managing director of the Stuyvesant Square Consultancy, a strategic advisory, market survey, and consulting firm in New York. His writings on economics, trade, politics, and public policy have appeared in Forbes, the New York Post, Crain’s New York Business, The Hill, The American Conservative, and other publications.