The Southern California housing market seems finally—maybe—to be returning to some semblance of normalcy.

Of course, some places are still super red-hot. Scott Barr, for instance, relates that the clients of Pacific Sotheby’s Global International looking for a home within five blocks of the ocean in Laguna Beach are still paying “all cash” for the $2 million and $3 million homes they want to buy.

At the same time though, Valerie Voss, a real estate agent in the Inland Empire area of southern California, reports that the buyers she’s seeing are no longer showing up with $50,000 and $75,000 for a down payment.

Indeed, she says, “If you’re an FHA buyer with 3.5 percent down, now is the first time in a long time you have a good change to be able to move into a home of your own.”

The FHA, or Federal Housing Administration, guarantees the debt of first time homebuyers and only requires they have 3.5 percent of the purchase price available as an initial down payment.

And those wealthy clients in Laguna Beach may still be borrowing up to 80 percent of the value of their home after they purchase the home, but for them, that’s a rational economic decision to borrow from a specialty lender at these super-low interest rates of still less than 3 percent and use the money for other investments with higher expected rates of return.

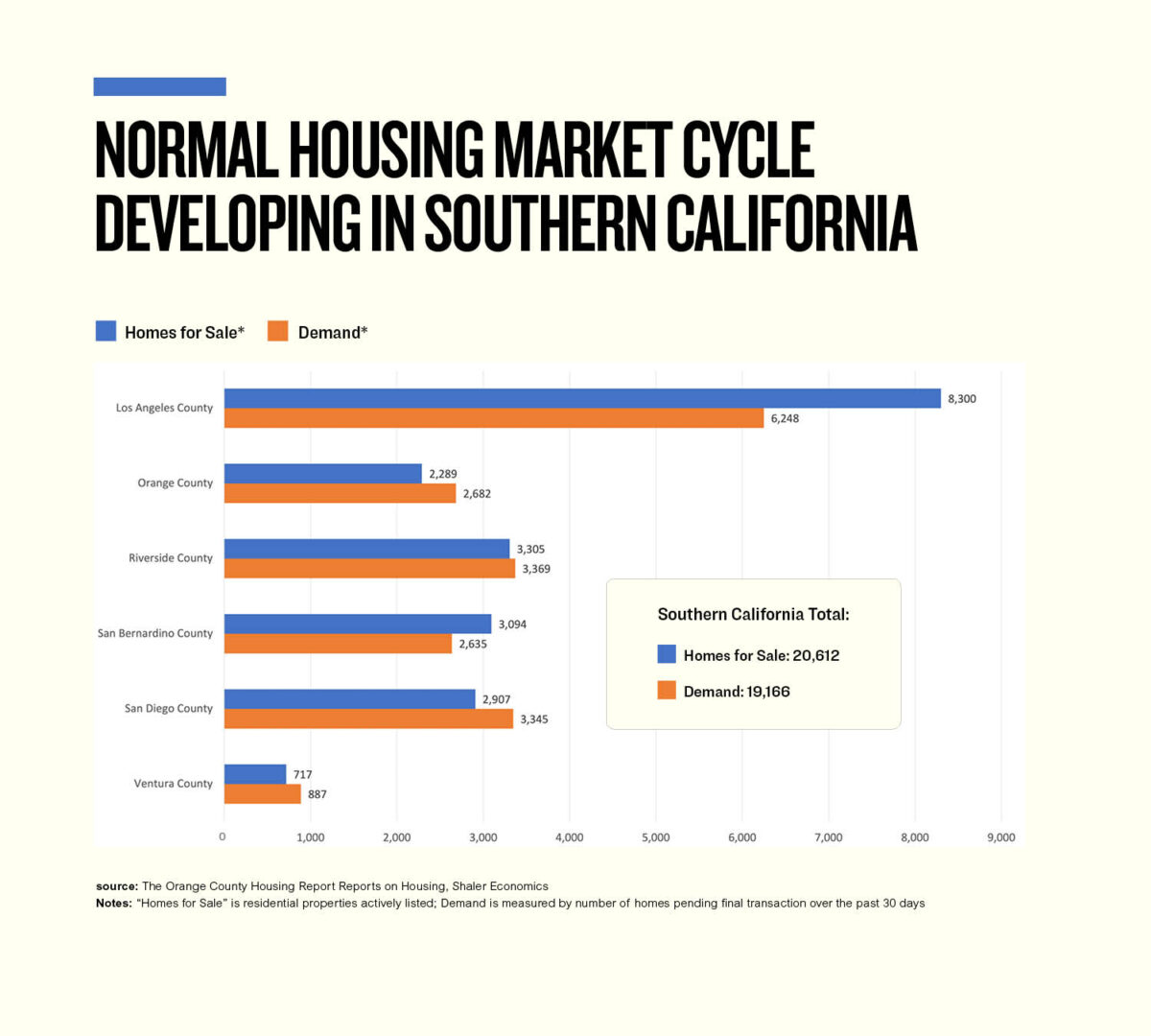

This all comes against the backdrop of “days to sell” times in southern California roughly in line with where they were at this time a year ago (comparing early September to early September).

According to the OC Housing Report, published every two weeks, the time a home-seller should expect to take to sell his or her home is back to where it was a year ago after reaching very fast levels during the spring and summer.

Now, however, students are generally going back to in-person classroom instruction, and parents will be reluctant to change homes while kids are in school and as Thanksgiving and the traditional December holidays approach.

Two other key phenomena taking place right now are that the State of California stopped paying Federally-subsidized additional unemployment benefits last week (Labor Day was the last day) and many mortgage forbearance programs are also coming to an end.

Valerie Voss, in the Inland Empire, thinks these mortgage forbearances might have a particularly strong impact where she lives. An increased supply of homes, possibly from home-sellers avoiding a foreclosure, will do much to lead to a “normal” “seasonality” in home prices. Home prices are typically lowest around the December religious holidays and are typically highest between Spring Break (typically tied to the timing of Easter) and when students go back to school.