But the cuts will put British finances further into debt because there is no corresponding cuts in government services, particularly the tremendously expensive National Health Service. The markets saw growing debt, as well as inflation, and responded to the measures by demanding higher interest rates, which was affected by the market lowering the value of the gilts.

Early on Wednesday, Eastern Standard Time, the prices of UK gilts took a battering from the markets. British pension funds that had put up their portfolio of gilts as collateral to borrow capital in order to enhance their returns suffered margin calls as the bonds fell in value, along with the value of the British pound.

The BOE intervention stopped the hemorrhaging of the UK gilts, at least for now. But it raises serious concerns about the stability of markets, mostly in the United Kingdom, and around the globe as well.

“The MPC’s annual target of an £80 billion stock reduction is unaffected and unchanged. In light of current market conditions, the Bank’s Executive has postponed the beginning of gilt sale operations that were due to commence next week. The first gilt sale operations will take place on 31 October and proceed thereafter.”In other words, the BOE was backing off from its planned reduction of its balance sheet, a reduction not unlike the planned reduction of the U.S. Federal Reserve’s balance sheet.

We Need to Be Wary

It’s important to note that while the pound is still a valued currency, it lost its status as the world’s reserve currency decades ago, when it was replaced by the U.S. dollar. The fact the pound is less significant than the dollar these days makes the pound much more vulnerable to the vagaries of the world’s sovereign debt markets, because lenders are concerned about the country’s ability to repay its debts, and—for foreign lenders—the value of pound when payment is made. (See, e.g., Japanese yen, once at veritable par with the dollar (1:100) 30 years ago, is now US$1:¥145 because its debt-to-GDP ratio has soared to more than 2.5:1.) The pound has similarly declined relative to what is now “King Dollar.”The U.S. dollar’s status as the world’s reserve currency—what was once called “an exorbitant privilege”—on the other hand, means that lending countries allow the United States to maintain a much larger balance of payments deficit than it would otherwise could.

Country X sells its goods or services to County Y in exchange for Country Y’s currency. Having no use for Country Y’s currency in Country X, Country X then uses the Country Y currency it has earned to do one of three things: 1) buy Country Y’s exports; 2), buy Country Y’s assets (factories, land, stocks, etc.), or 3) buy Country Y’s sovereign debt. So if Country X has a current account balance of payments deficit—meaning, Country X bought more from Country Y than it sold to Country Y—then Country X can either buy Country Y assets, like factories or stocks, or Country Y government bonds.Country X here is the functional equivalent of China and Country Y is the functional equivalent of the United States. Because of the U.S. balance of payments deficit, China (and several other of our trading partners) have excess dollars that they all need to return to the United States. The excess of those funds, after China purchases U.S. goods and services, are invested in U.S. assets such as properties, stocks, and U.S. Treasuries. This allows the United States to finance its $31 trillion national debt.

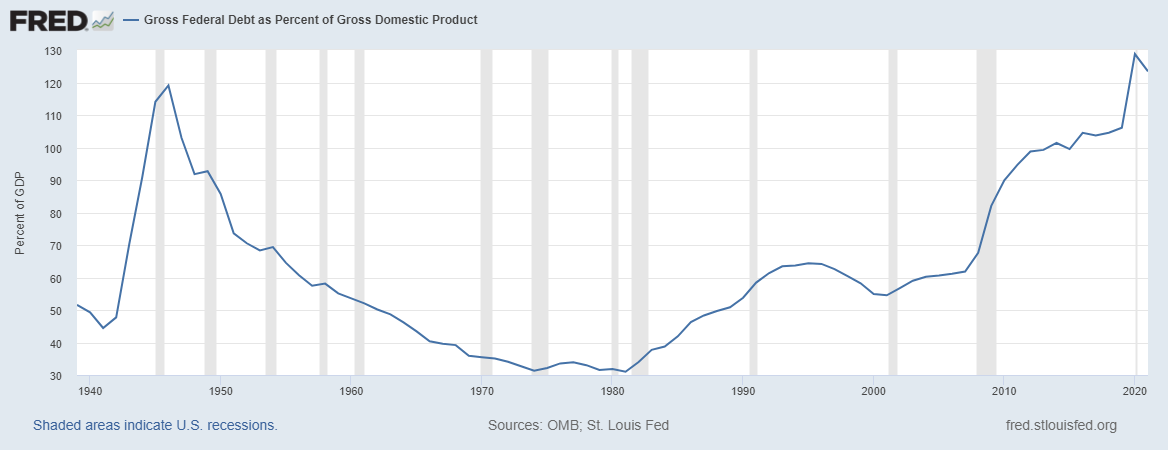

Ratio of U.S. Debt to GDP, 1940–2022

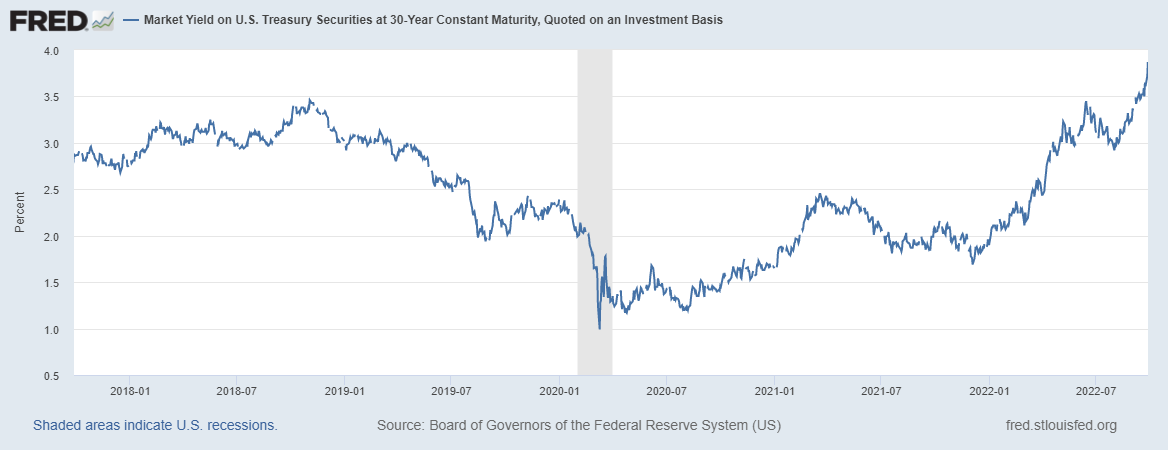

Market Yield on U.S. Treasury Securities at 30-Year Constant Maturity (quoted on an investment basis, 9/17–9/22)

Thus, the United States potentially faces the same kind of liquidity crisis the United Kingdom faced this morning.

The Fed, like the BOE, is tightening credit with higher rates at the very same time it is allowing its balance sheet of Treasuries and mortgage-backed securities to burn off to the tune of $95 billion per month. Thus bond values are falling and, consequently, bond rates are increasing. As illustrated above, the interest rate on the 30 year Treasury has spiked, and rapidly, to its highest rate since November 2018. On Wednesday, the yield on the 30-year bond briefly reached 4 percent, but then the rate fell, and as it did, the market rebounded from the doldrums and closed up 1.8 percent.

It seems the markets believe the Federal Reserve will ease up on the tightening of the markets, as the BOE did on Wednesday when it delayed its planned sale of gilts until the end of next month. But if the Fed loosens monetary tightening to avoid a liquidity crisis, as the BOE did, or to avoid a recession, that should trouble—not encourage—the markets. It means the Fed has effectively lost control of monetary policy.

In summary, the global markets are decidedly unstable. There is a risk of a liquidity crisis in the United States, not unlike the one Britain experienced briefly on Wednesday, when margin calls on bond collateral forced sales and drove up rates. Such developments risk a downward—and rapid—spiral of bond values, further driving up rates. It has the potential to be a very dangerous and unstable time.

Investors should act with extreme caution. Begin by rebalancing portfolio toward cash and set stop-loss orders on brokerage accounts.

___________________________________________________