Student loan debt relief is a regressive policy that mostly benefits high-income households, says former U.S. Treasury Secretary Larry Summers.

In a series of tweets, the former director of the National Economic Council (NEC) in the Obama administration stated that “all serious economists” agree that debt reduction is “regressive.”

Summers also thinks a good start to altering post-secondary student lending is to substitute loans with grants.

Recently, President Joe Biden extended the moratorium on student loan payments, which Summers believes is “highly problematic” when judged on its economic effects.

Is Student Loan Debt Relief Regressive?

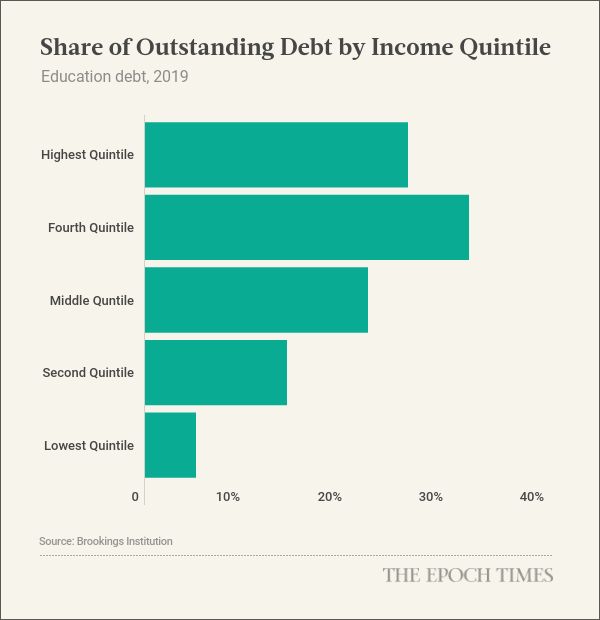

The Brookings Institution, an economic research think tank, published a report in October 2020 that assessed who owed most of the student loan debt.

The highest-income 40 percent of households owed close to 60 percent of the outstanding education debt and made nearly 75 percent of the payments, Brookings noted. But the lowest-income 40 percent of households possessed about a fifth of the outstanding debt and made just 10 percent of the payments.

“It should be no surprise that higher-income households owe more student debt than others,” the think tank wrote. “Students from higher-income households are more likely to go to college in the first place. And workers with a college or graduate degree earn substantially more in the labor market than those who never went to college.”

Some public policymakers also assert that it would be a waste of federal resources since it would fail to help the tens of millions of Americans who didn’t attend university or college and don’t have national student debt.

Others disagree, including the Roosevelt Institute, a New York City-based, left-leaning think tank.

“Contrary to common misperceptions, careful analysis of household wealth data shows that student debt cancellation ... would provide more benefits to those with fewer economic resources and could play a critical role in addressing the racial wealth gap and building the Black middle class,” the report stated.

Inflation and a Recession

Summers also chimed in on the most pressing issue facing many Americans today: inflation.

The administration has promised that inflation would subside over the next 12 months because of its actions, from tapping strategic oil reserves to investigating anti-consumer practices. The latest recommendation involves employing anti-monopoly laws.

But the Harvard economist thinks exploiting antitrust regulations to reduce 39-year high inflation is a reflection of “science denial” on the part of the White House.

He also recently warned about a looming recession threat stemming from inflation dangers.

Many Americans are worried about the same economic downturn amid rampant price inflation.