New jobs created printed at 236,000 on April 7, according to the Establishment Survey, on par with market expectations of 230,000 jobs. The Household Survey printed lower, at 160,000. Net revisions were down 17,000 from January and February.

Both the unemployment rate, at 3.5 percent, and the number of unemployed persons, at 5.8 million, changed little in March. The U6 number was 6.7 percent. The U6 is total unemployed plus all persons marginally attached to the labor force plus total employed part time for economic reasons, as a percent of the civilian labor force, plus all persons marginally attached to the labor force. The Labor Participation Rate increased to 62.6, up from last month and last year, we believe largely as a consequence of pandemic benefits fInally being withdrawn.

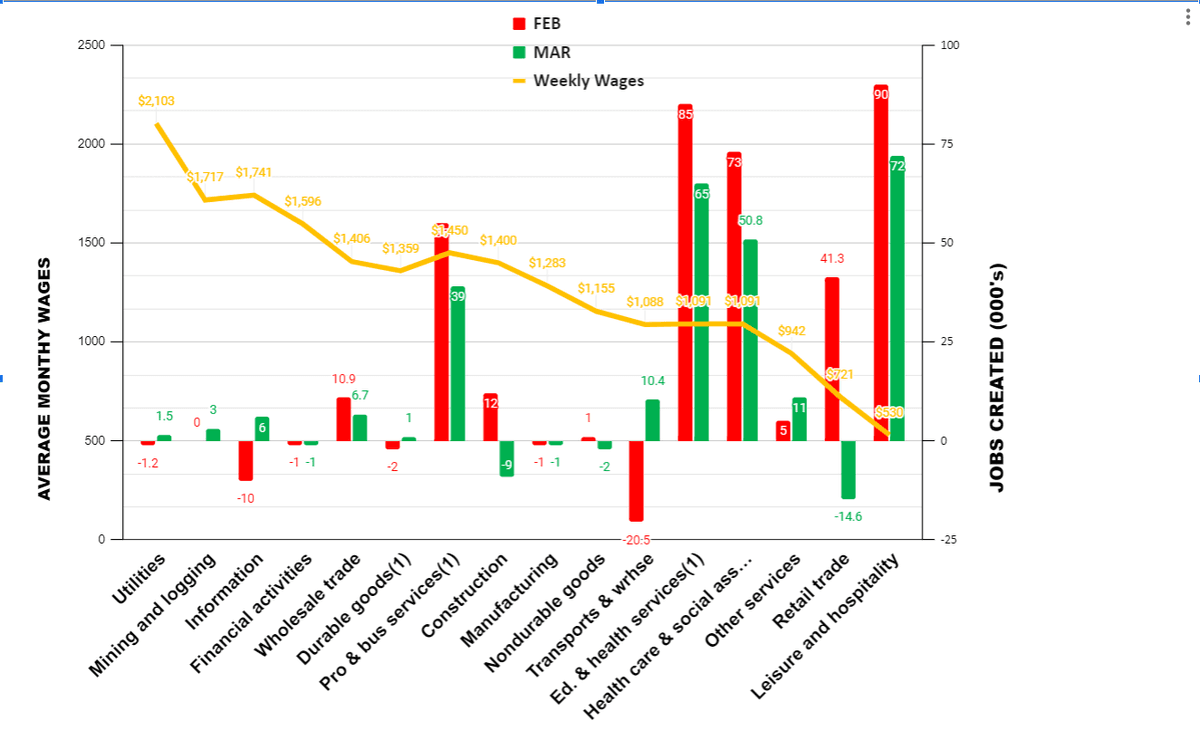

Looking at our exclusive chart of jobs created by average weekly wages, you can see that most of the jobs are in the leisure and hospitality sectors and in the heavily government-supported education, health, and social services sector. Jobs were lost in retail, construction, and nondurable goods manufacturing, which are often the earliest signs of a slowing economy.

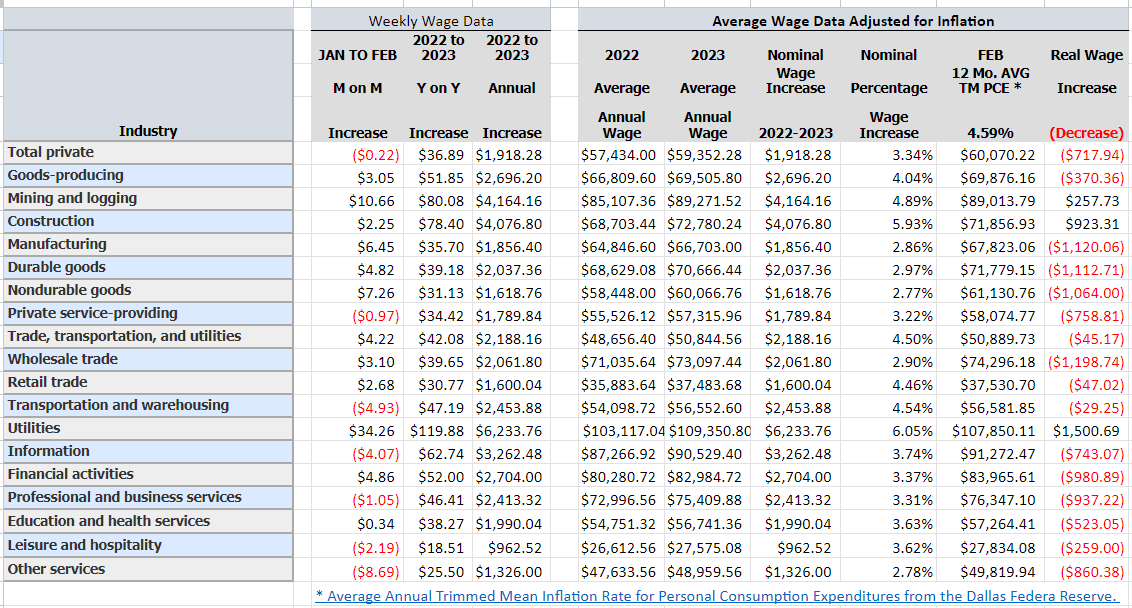

Our quarterly assessment of average real wages by sector shows that almost all jobs lost ground, in terms of real wages, after adjusting for annualized inflation. Only those high-skilled, often dangerous, positions in mining and logging, construction, and utilities gained real wage ground.

Other Data

The March ISM Manufacturing Index printed at an abysmal 46.3 on Monday, below market expectations. That is the lowest print since the start of the pandemic, which print was, itself, the lowest print since the financial crisis of 2008–09 and indicates the economy is contracting faster. Wednesday’s release of the ISM Services Index showed growth, but at a slower rate, led by a decline in export services orders.Building permits in February, released March 16, were at a seasonally adjusted annual rate of 1,524,000. This is 13.8 percent above the revised January rate of 1,339,000, but is 17.9 percent below the February 2022 rate of 1,857,000. Privately owned housing starts in February were at a seasonally adjusted annual rate of 1,450,000. This is 9.8 percent above the revised January estimate of 1,321,000, but is 18.4 percent below the February 2022 rate of 1,777,000.

Opinion

We continue to abide by our view that that there will be a recession commencing in the third quarter (to be acknowledged sometime in 2024); however, our former belief that the Fed would continue with robust interest-rate increases has changed. We think that the Fed has been chastened by the banking crisis, which was exacerbated by Fed tightening. We believe, moreover, that banks will fortify their balance sheets and be more restrained in their lending, effectively doing the Fed’s tighening for them. (Banks begin to report earnings next week; we'll be watching closely.)Today’s jobs numbers, which reflect hiring only through the first half of March, will likely be far more restrained next month. There will be no “soft landing.” There will be a mild recession in the second half that could worsen in 2024, depending on the policy response.

We predict first-quarter 2023 GDP will print at 1 percent. We anticipate second quarter 2023 will print at 0.5 percent. Jobs numbers, which have not printed below expectations in nearly a year, will most likely print below 200,000 new jobs.

_______________________________________________________