Commentary

The January jobs report printed at a moderate 467,000 new jobs, well above the consensus estimate of 150,000.

The seasonally adjusted unemployment rate was 4 percent, unchanged.

The seasonally adjusted U-6 Unemployment, at 7.1 percent, was down 2/10th of a percentage point from December, and down 4 percentage points since last year.

Analysis: Details and Outlook from Stuyvesant Square

The January jobs report surprised most and signaled, first, that the Federal Reserve is likely to drive rates higher.That said, the effect of the annual benchmarking should not be ignored. As related by the Bureau of Labor Statistics at the end of the report, today’s numbers are “benchmarked to reflect comprehensive counts of payroll jobs for March 2021. These counts are derived principally from the Quarterly Census of Employment and Wages (QCEW), which counts jobs covered by the Unemployment Insurance (UI) tax system. The benchmark process results in revisions to not seasonally adjusted data from April 2020 forward.” (Details of these adjustments can be found here.)

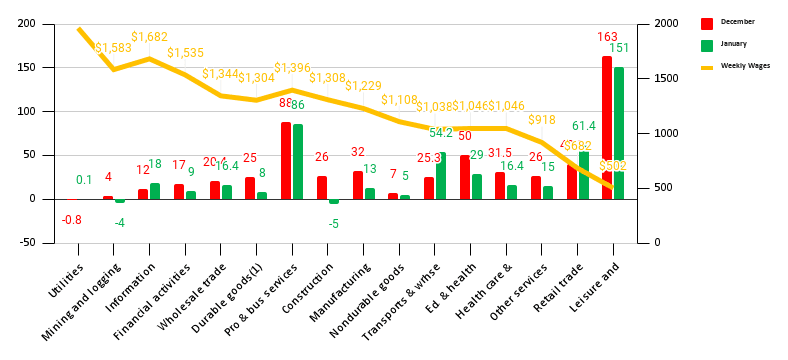

Note, too, that a significant number–151,000–of the new jobs were created in the “Leisure and Hospitality” sector, where average weekly wages are just $502/week. The other big performer was in Professional & Business Services, but we have seen this over several years as accounting firms and companies hire staff for the calendar year closings, audits, and tax compliance.

January Jobs by Average Weekly Wages

Source: ©The Stuyvesant Square Consultancy from BLS January Jobs Data.

Fed Normalizing

On Thursday, the Bank of England increased rates by 25 basis points, or a quarter of one percent to 0.5 percent. The European Central Bank kept rates flat, but will discontinue net purchases of bonds under its pandemic emergency purchase program at the end of March 2022. The Bank of Japan, meeting last month, let rates stand pat, but reportage today indicates markets are expecting a tightening.Trimmed mean inflation for personal consumption expenditures, less food and energy, or “Real PCE“ for the Dallas Fed was at 3.0 percent, year on year for December. The real PCE Price Deflator, reportedly the Fed’s preferred measure of inflation, printed at 4.9 percent for December. That compares to 1.5 percent for December of 2020.

All this points to the Fed almost assuredly raising rates when it meets in March. Depending on the February jobs report, which will print on March 4, we expect the March 15–16 Federal Open Market Committee to raise rates between a quarter and a half point.

We also expect that the Fed will announce a full stop—or at least a further significant decrease—to its asset purchase program. This should drive longer-term rates higher, as we discussed in our column in December.

We reiterate our view that the first half of 2022 is “risk off” and that equity and bond values will be adversely affected as the Fed moves to normalize rates to at least r*, the natural rate of interest. Larry Summers and others have stated the Fed’s rate is below the natural rate. They urged rate hikes for that reason.

Additional Risks

We have grave concerns about Russian, U.S., and NATO policy in Eastern Europe. All sides have engaged in provocative behavior, and the likelihood it will be resolved peaceably with all sides in a better condition is virtually nil. We see a danger to the USA, even with a course of sanctions.Supply chains continue to be stressed, particularly electronic chips so that sales of consumer durables that utilize them will be slowed. China’s shutdown will exacerbate all types of supply shortages in the USA and among our trading partners.